Bloom Energy SOFC Industrial Rollout, $7.65 B Data Center Deals vs. High CAPEX and 2 Critical Material Risks (2021 to 2026)

Industrial SOFC Projects, Bloom Energy Confronts High CAPEX and Material Risk

Solid Oxide Fuel Cells (SOFCs) are failing to achieve widespread adoption in the steel, cement, and chemical sectors primarily due to prohibitive capital expenditures and supply chain vulnerabilities, a stark contrast to their rapid success in the power-hungry data center market. While the technology’s high efficiency presents a clear path to decarbonize industrial heat, economic and material headwinds are confining most projects to the pilot stage, preventing the scale needed to make a significant impact on industrial emissions in 2026.

- The commercial divergence is clear: while the fuel cell market captured $7.65 billion in data center deals in a recent 90-day period, adoption in heavy industry remains limited to smaller, validation-focused trials such as the DEMOSOFC project. This highlights a fundamental challenge where industrial customers, unlike hyperscalers facing grid-lock, are more sensitive to high initial costs versus mature incumbent technologies.

- Between 2021 and 2024, the focus was on announcing and launching pilots to prove technical feasibility. Now, from 2025 to 2026, the conversation has shifted to economic viability. The inability of SOFCs to provide the primary high-temperature heat (above 1, 000°C) for steel and cement kilns relegates them to auxiliary power and heating roles, complicating the investment case for a full-scale replacement of existing assets.

- The chemical industry remains the most promising near-term market for industrial SOFC-CHP systems. The technology’s high-grade exhaust heat aligns well with the sector’s constant demand for process steam. However, even in this ideal use case, high capital cost remains the primary barrier to adoption over conventional gas boilers and turbines.

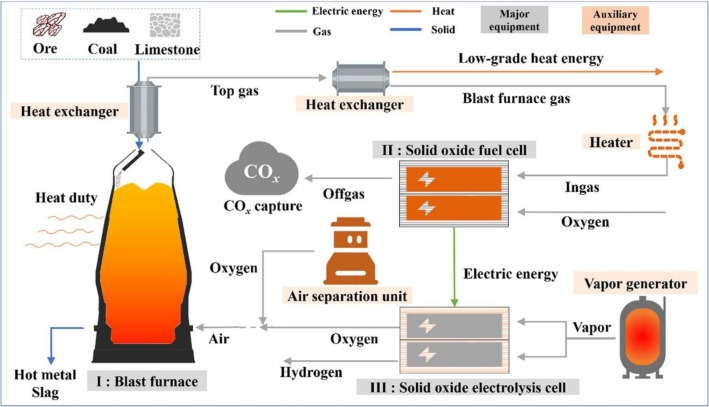

SOFCs to Decarbonize Industrial Steelmaking

This diagram shows how SOFCs can integrate with the steelmaking process, directly illustrating the technology’s potential for industrial decarbonization mentioned in the section.

(Source: ScienceDirect.com)

Ceres Power Forges 3 OEM Partnerships to Tackle SOFC Manufacturing Scale

Strategic partnerships between technology developers and large-scale industrial manufacturers are the primary mechanism being used to address the dual challenges of high manufacturing costs and market access for SOFCs. By combining specialized fuel cell expertise with the manufacturing prowess and supply chain control of established original equipment manufacturers (OEMs), the industry aims to scale production and drive down the unit costs that currently hinder industrial adoption.

- The asset-light licensing model, exemplified by [Ceres Power], is central to this strategy. By partnering with industrial giants like Bosch in Europe and Weichai in China, the company aims to leverage their existing manufacturing infrastructure to produce SOFC stacks at a scale and cost unachievable for a standalone technology firm.

- Pilot-focused partnerships are critical for validating the technology in harsh, real-world operating conditions. The trial involving Delta, [MODEC], and Eld Energy to test a 120 k W SOFC system is a key example, with the goal of moving to commercial production by the end of 2026. Success in these trials is essential to building bankability for larger projects.

- Collaborations are also extending to future fuel sources, preparing the technology for a post-natural gas world. The alliance between NYK Line and Samsung Heavy Industries to deploy ammonia-fueled [SOFC systems in maritime shipping] by 2028 demonstrates the platform’s adaptability and secures its relevance in long-term decarbonization roadmaps.

Table: Key SOFC Strategic Partnerships (2025-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Ceres Power & Weichai/Bosch | Ongoing (2025-2026) | Licensing partnerships to scale manufacturing in China and Europe, aiming to reduce system costs and accelerate market penetration in industrial and transport sectors. | Gasworld |

| Delta, MODEC, & Eld Energy | 2026 | Trial of a 120 k W SOFC power system with a target for initiating commercial production in late 2026, validating the technology for off-grid and industrial power applications. | Port News |

| NYK Line & Samsung Heavy Industries | 2028 (Target) | Joint development to deploy ammonia-fueled SOFCs on vessels, demonstrating the technology’s fuel flexibility and addressing decarbonization in the hard-to-abate shipping sector. | Mordor Intelligence |

Asia-Pacific vs. Europe, Weichai Drives SOFC Adoption in China’s Industrial Base

While North America and Europe lead in policy-driven initial deployments and high-margin data center applications, the Asia-Pacific region, particularly China, is positioned as the critical long-term growth engine for industrial SOFCs. This geographic shift is driven by the region’s massive manufacturing base, urgent need for cleaner industrial processes, and direct state support for fuel cell technology as a pillar of national industrial policy.

Asia-Pacific to Dominate SOFC Market

This forecast validates the section’s thesis by showing the Asia-Pacific region as the largest and fastest-growing market, underpinning its role as the long-term growth engine.

(Source: MarketsandMarkets)

- Between 2021 and 2024, SOFC activity was concentrated in North America, led by [Bloom Energy]’s commercial success in stationary power, and in Europe, where EU-funded pilots like DEMOSOFC demonstrated technical viability.

- Starting in 2025, a strategic pivot toward the Asia-Pacific market has become evident. China’s industrial strategy, executed through manufacturing giants like Weichai, is a major catalyst, targeting SOFCs for both industrial CHP and transportation, creating a demand-pull that outstrips other regions.

- Europe remains a crucial hub for innovation and policy development. The EU’s Clean Hydrogen Partnership and national strategies in Germany and Belgium create specific demand for high-temperature heat solutions in the chemical and steel industries, serving as a key proving ground for industrial applications.

- Nascent interest is emerging in markets like India and Malaysia, where companies like Elcogen are expanding. This interest is driven less by carbon mandates and more by a strategic need for energy security and a desire to reduce dependence on volatile imported fossil fuels.

SWOT Analysis, Bloom Energy’s SOFC Efficiency vs. Material and Cost Risks

In 2026, the strategic position of natural gas SOFCs is defined by a clear and proven strength in energy efficiency, which creates a compelling economic case for industrial users. However, this is directly offset by critical weaknesses in high capital costs and vulnerable material supply chains. These factors create immediate opportunities in transitional decarbonization but expose the technology to significant threats from competing solutions and future regulatory shifts.

- Strengths: Unparalleled combined heat and power (CHP) efficiency, exceeding 90% in many applications, provides a direct and immediate reduction in fuel consumption and operating costs for industrial users.

- Weaknesses: Prohibitively high capital expenditure (CAPEX) remains the single largest barrier to widespread adoption, coupled with a dependence on rare earth elements (REEs) whose supply chains are concentrated and subject to geopolitical risk.

- Opportunities: The technology is perfectly suited to serve the $35+ billion industrial CHP market and has found a new, high-margin anchor market in powering data centers, which provides revenue to fund further R&D and scale manufacturing.

- Threats: Volatility in the price of natural gas, the primary feedstock, directly undermines the technology’s operating cost advantage. Furthermore, the rapid advancement of green hydrogen and direct electrification technologies poses a long-term competitive threat.

Table: SWOT Analysis for Natural Gas SOFC for Industrial Heat 2026: Steel, Cement, and Chemical Applications

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | High electrical efficiency (~60%) and CHP potential were demonstrated in pilot projects and early commercial deployments. Fuel flexibility was a theoretical advantage. | World-class efficiency is now commercially validated, with new stacks from Ceres reaching 69% electrical efficiency. Total CHP efficiency is consistently reported above 90%. | The technology’s core efficiency advantage has been validated at scale, moving from a feature of pilots to a bankable characteristic of commercial products. |

| Weaknesses | High CAPEX and reliance on rare earth elements (REEs) like cerium and gadolinium were identified as key research challenges to be solved through material science. | CAPEX remains the primary barrier to industrial adoption. The data center boom proves some customers will pay a premium, but industrial sectors remain price-sensitive. REE supply chain risk has intensified. | The problem has shifted from a technical R&D challenge to a critical commercial and geopolitical hurdle. The market has bifurcated between high-margin niche applications and cost-sensitive industrial ones. |

| Opportunities | The primary opportunity was seen in replacing traditional CHP systems and providing grid stability. Early interest was noted from data centers. | The data center market has exploded into a $7.65 billion opportunity captured in just 90 days. Integrating SOFCs with carbon capture for e-fuel production has emerged as a new strategic opportunity. | The data center boom provided a vital, high-margin anchor market that did not exist at scale before 2025, offering a path to profitability that can fund industrial cost-down efforts. |

| Threats | Competition from other fuel cell types (PEMFC) and improving renewables with storage. Natural gas price volatility was a known risk. | The threat from green hydrogen-based direct reduced iron (DRI) in steel and direct electrification in other sectors has become more defined, positioning NG-SOFCs as a ‘bridge’ technology. The risk of future carbon taxes on natural gas has increased. | The long-term competitive landscape has clarified, confirming that while NG-SOFCs are a vital transitional tool, they are not the final net-zero solution for many industrial processes. |

SOFC 2026 Outlook, Bloom Energy Viability Hinges on CAPEX and Pilot Success

For natural gas SOFCs to transition from a niche data center solution to a mainstream industrial decarbonization tool in 2026, the market must see a definitive downward trend in capital costs and the successful commissioning of at least one flagship project in a steel, cement, or chemical facility. Without these validation points, the technology risks remaining too expensive for the industrial sectors that need it most, despite its clear efficiency advantages.

SOFC Market Forecast Shows Massive Growth

This strong market forecast quantifies the high-stakes potential discussed in the 2026 outlook, which hinges on overcoming cost barriers to achieve mainstream adoption.

(Source: Straits Research)

Diagram Explains SOFC Conversion Efficiency

This schematic illustrates the energy conversion process, providing a visual explanation for the high efficiency that the section’s SWOT analysis highlights as a key validated strength.

(Source: ScienceDirect.com)

- If large-scale industrial pilots, such as the planned trials in steel production environments, report successful long-term operation with minimal degradation through 2026, then watch for major industrial firms like BASF or Holcim to issue the first significant, multi-unit offtake agreements for their facilities.

- If manufacturing-focused partnerships, like the one between Ceres Power and Weichai, result in a publicly confirmed system cost approaching the critical $1, 000/k W milestone, then these could be happening: a rapid increase in project financing for industrial CHP projects and a decisive shift in market sentiment from cautious to bullish.

- A key signal that is losing steam is the narrative of SOFCs as a permanent, standalone solution for heavy industry. The market is consolidating around the consensus that they are a crucial, highly efficient *transitional* technology that bridges today’s natural gas infrastructure to tomorrow’s hydrogen economy.

- A signal gaining significant traction is the development of Reversible Solid Oxide Cells (Re SOCs). This technology, which combines fuel cell and electrolyzer functions in one unit, adds valuable energy storage and green hydrogen production capabilities, strengthening the long-term value proposition and ensuring the core technology’s relevance in a fully renewable energy system.

The questions your competitors are already asking

This report covers one angle of the commercial barriers facing SOFCs in industrial heat applications. The questions that matter most depend on your work.

- Are industrial SOFC pilot projects like DEMOSOFC progressing to commercial deployment in the steel and cement sectors?

- What is the outlook for SOFC deployment in the steel, cement, and chemical sectors by 2026, given the prohibitive CAPEX and critical material risks?

- How does the cost of an industrial SOFC-CHP system compare to mature incumbent technologies for high-temperature heat?

- What are the near-term opportunities for SOFCs in the chemical industry, where high-grade exhaust heat aligns with process steam demand?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.