Bloom Energy SOFC Deployments, 2.8 GW Oracle Deal, $2.65 B AEP Contract, and $7.65 B Data Center Deals (2026)

SOFC Commercial Projects, Bloom Energy Shift From Pilots to Gigawatt-Scale Data Center Deals

Solid Oxide Fuel Cell (SOFC) technology transitioned from niche pilots to gigawatt-scale commercial deployments in 2026, driven by the acute power and reliability demands of the AI data center industry. This shift marks the technology’s validation as a bankable, scalable solution for mission-critical power, moving far beyond the smaller demonstration projects that characterized the market in prior years.

- Between 2021 and 2024, SOFC adoption was characterized by smaller-scale industrial and utility pilots focused on demonstrating fuel flexibility and emissions reductions.

- In 2026, the market shifted dramatically with multi-gigawatt agreements, exemplified by the 2.8 GW supply deal between [Bloom Energy] and Oracle for data center power, a scale previously unseen in the fuel cell industry.

- The first 90 days of 2026 saw $7.65 billion in fuel cell deals specifically for data centers, confirming that the sector’s power crisis has become the primary catalyst for SOFC commercialization.

- While data centers became the anchor market, applications expanded into other hard-to-abate sectors, with 2026 pilot projects targeting maritime shipping (Genevos‘s HELENUS project) and offshore energy (MODEC‘s FPSO deployment), demonstrating the technology’s versatility.

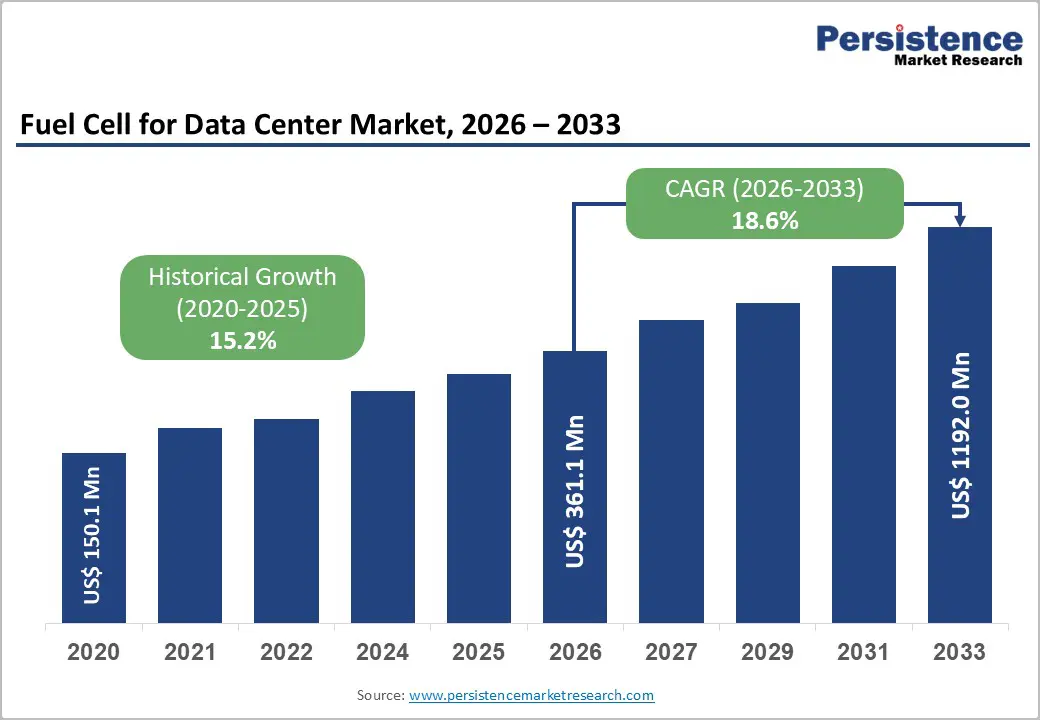

Data Center Fuel Cell Market Nears $1.2B

This chart directly quantifies the market opportunity in data centers, which is the core subject of the section discussing the shift to gigawatt-scale data center deals.

(Source: Persistence Market Research)

$5 B in Funding, Bloom Energy Secures Brookfield and AEP Capital for SOFC Production

Major capital injections from financial institutions and utilities in 2026 have de-risked SOFC manufacturing scale-up and provided the financial backing for multi-billion-dollar, long-term deployment agreements. This influx of capital from sophisticated investors validates the technology’s economic model and provides the runway for significant capacity expansion.

- Brookfield committed to invest up to $5 billion to finance the deployment of Bloom Energy‘s SOFC technology, signaling strong confidence from institutional investors in the technology’s commercial viability and long-term revenue potential.

- Utility giant American Electric Power (AEP) signed a landmark $2.65 billion deal to deploy up to 1 GW of Bloom Energy‘s SOFC systems, marking a significant commitment from a regulated utility to fuel-flexible, dispatchable power assets.

- Fuel Cell Energy announced a collaboration with Sustainable Development Capital LLP (SDCL) to deploy up to 450 MW of fuel cell power, demonstrating a growing market for third-party financing and deployment models that lower upfront capital costs for end-users.

Table: Bloom Energy Strategic Investments

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Brookfield | Jan 2026 | Up to $5 billion investment to finance the deployment and offtake of Bloom Energy‘s SOFC technology. The agreement de-risks customer adoption by providing a clear financing pathway. | Lee Enterprises |

| American Electric Power (AEP) | Jan 2026 | A $2.65 billion agreement to deploy up to 1 GW of Bloom Energy‘s SOFCs. This validates the technology for utility-scale, dispatchable power and provides a pathway to integrate green hydrogen into the grid. | Fuel Cells Works |

| Data Center Sector | Q 1 2026 | Fuel cell companies secured $7.65 billion in data center deals in the first 90 days of 2026. This capital influx is a direct response to the AI-driven power shortage and need for reliable, on-site generation. | Introl Blog |

Ceres Power Multi-Gigawatt Centrica Partnership, Expanding SOFC Technology Licensing (2026)

Strategic partnerships between SOFC technology developers and large industrial energy consumers solidified in 2026, moving beyond R&D collaborations to create multi-gigawatt deployment pipelines aimed at future-proofing industrial power supplies. These alliances pair technology innovators with established market leaders, accelerating market penetration and scaling.

- The strategic partnership between [Ceres Power] and Centrica aims to develop a multi-gigawatt pipeline of on-site SOFC power for industrial customers in the UK and Europe, establishing a clear commercial pathway from natural gas to hydrogen.

- In the offshore sector, a tripartite collaboration formed between MODEC, Eld Energy, and Delta Electronics to pilot a 120 k W SOFC system on a Floating Production Storage and Offloading (FPSO) vessel, creating an integrated partnership to decarbonize a complex industrial environment.

- Technology licensor Elcogen expanded its ecosystem through Mo Us with JNK India Limited in India and a partnership with Bonicorn and Eltronic Pt X in Thailand, enabling regional manufacturing and deployment through local industrial experts.

Table: Ceres Power and Bloom Energy Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Oracle / Bloom Energy | Apr 2026 | Expansion of a supply agreement to 2.8 GW for powering Oracle data centers. This massive deal establishes SOFCs as a core infrastructure component for hyperscale computing. | Data Center Dynamics |

| Centrica / Ceres Power | Mar 2026 | A strategic partnership to develop a multi-gigawatt pipeline of on-site fuel cell power for industrial customers. The systems will initially use natural gas and transition to hydrogen, future-proofing the investment. | Centrica |

| MODEC / Eld Energy / Delta Electronics | Jan 2026 | Collaboration to deploy a 120 k W SOFC system on an FPSO vessel by 2027. The project aims to prove the technology’s viability for decarbonizing the demanding offshore energy sector. | Offshore Energy |

US vs. Europe Market Growth, Ceres Power and Bloom Energy Target Regional SOFC Demand

While the United States led in 2026 with large-scale, centralized SOFC deployments for data centers, Europe and Asia focused on building distributed industrial energy ecosystems through strategic technology licensing and regional partnerships. This geographic divergence reflects different market needs and regulatory environments, with the U.S. prioritizing immediate, large-scale power solutions and Europe and Asia building broader industrial capabilities.

European SOFC Market Forecasted for Strong Growth

The section specifically compares the US and European markets. This chart provides a concrete forecast for the European SOFC market, directly supporting the section’s regional analysis.

(Source: Market Data Forecast)

- The U.S. market is dominated by large, direct sales from manufacturers like Bloom Energy for on-site power, driven by grid constraints and the urgent power requirements of hyperscale data centers.

- In Europe, the model is characterized by partnerships like the one between Centrica and [Ceres Power] in the UK, focusing on creating decentralized power generation for a broad industrial base with a government-supported path to green hydrogen.

- Asia is emerging as a key growth market for technology adoption and manufacturing, with companies like Elcogen establishing partnerships in India and Thailand to support industrial decarbonization and green hydrogen production goals.

SOFC Commercial Scale, Ceres Power and Bloom Energy Validate Bankable Technology

Solid Oxide Fuel Cell technology achieved commercial-scale validation in 2026 for stationary power generation, while parallel developments in reversible operation and new fuel compatibility demonstrate its increasing maturity as a flexible platform for the energy transition. The technology has moved beyond questions of technical viability to matters of economic competitiveness and manufacturing scale.

Planar SOFC Market to Exceed $1.7B by 2031

This section discusses the commercial-scale validation and economic competitiveness of SOFCs. The chart provides a strong monetary forecast for the specific technology, validating its market growth.

(Source: Mordor Intelligence)

- Between 2021 and 2024, the primary focus was on proving SOFC reliability and efficiency in sub-megawatt deployments, often in subsidized demonstration projects.

- In 2026, the technology proved its bankability at scale with multi-gigawatt deals from companies like Oracle and AEP, confirming its readiness for mission-critical, 24/7 power applications without direct reliance on pilot-program subsidies.

- Technology developers are now advancing dual-use platforms; [Ceres Power] launched a single stack platform capable of both power generation (SOFC) and hydrogen production (SOEC), enabling assets to serve multiple functions and improve utilization.

- Fuel flexibility expanded beyond natural gas and hydrogen, with a 2026 debut by Chery of a 25 k W SOFC system fueled by ammonia, opening pathways to use hydrogen carriers for decarbonization in applications where direct hydrogen is not feasible.

SOFC SWOT Analysis, Bloom Energy Market Opportunities and Hydrogen Cost Risks

The SOFC market in 2026 is defined by the strength of its fuel flexibility and the massive opportunity presented by data center power demand, while its primary weakness remains the near-term reliance on natural gas and the external threat of high green hydrogen costs. The recent surge in commercial activity has validated the technology’s strengths and magnified the opportunities, but has not yet resolved underlying dependencies.

Hydrogen Economy Faces $500B+ Investment Gap by 2030

The section identifies ‘high green hydrogen costs’ as a key risk in its SWOT analysis. This chart quantifies the massive investment gap in the hydrogen economy, which is a primary driver of that cost risk.

(Source: ScienceDirect.com)

Table: SWOT Analysis for Hydrogen-Ready SOFC Systems (2026)

| SWOT Category | 2021 – 2023 | 2024 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | High electrical efficiency and fuel flexibility demonstrated in pilots. Lower emissions compared to grid power. | Proven 24/7 reliability for mission-critical loads. Fuel flexibility (natural gas to hydrogen) is a key selling point. High power density for on-site generation. | Large-scale deals (Oracle 2.8 GW) validated SOFCs as a bankable, reliable solution for hyperscale data centers, moving past the pilot stage. |

| Weaknesses | High capital cost relative to conventional generation. Limited manufacturing scale. | Green hydrogen costs ($4.00-$7.00/kg) remain above the economic target of $3.00/kg. Initial deployments still rely primarily on natural gas. | The “hydrogen-ready” feature is being sold, but its economic use is still in the future, creating a dependency on natural gas prices in the near term. |

| Opportunities | Grid instability and decarbonization goals created a niche for reliable on-site power. | Explosive power demand from AI data centers. Major government investments ($150 B by 2030) in hydrogen infrastructure. Hard-to-abate sectors (maritime, offshore) seeking solutions. | The AI boom created a massive, urgent, and well-funded customer base (data centers) that did not exist at this scale before 2024, accelerating adoption by years. |

| Threats | Competition from other clean energy sources like solar and batteries. Fluctuating natural gas prices. | Pace of green hydrogen infrastructure build-out. Potential for competing technologies (e.g., SMRs) to offer similar clean, firm power. Regulatory uncertainty. | The market’s heavy concentration on the data center sector creates a single point of failure risk if that industry’s growth slows or it finds alternative power solutions. |

2027 SOFC Outlook, Bloom Energy Data Center Pipeline vs. Ceres Power Licensing Model

For the year ahead, the key strategic question is whether the vertically integrated, direct-sales model of Bloom Energy will continue to dominate through large data center contracts, or if the asset-light, technology-licensing model of Ceres Power will accelerate broader market adoption through its industrial partners.

Stationary Fuel Cell Market Growth Accelerates After 2025

This section provides a ‘2027 SOFC Outlook.’ The chart offers a relevant, forward-looking forecast for the stationary fuel cell market, showing accelerated growth in the exact period being discussed.

(Source: Global Market Insights)

Gap Widens Between Announced and Committed Hydrogen Projects

The SWOT table identifies the high cost of green hydrogen as a threat. This chart visualizes the risk by showing the vast difference between announced hydrogen projects and those that are actually committed, underscoring the uncertainty.

(Source: Intelligent Living)

- If green hydrogen costs remain above $4.00/kg, expect SOFC deployments to remain concentrated in high-value applications like data centers where reliability and power density are paramount, favoring established players like Bloom Energy.

- Watch for additional strategic partnerships between SOFC licensors and major industrial conglomerates, particularly in Asia. A new partnership with a major manufacturer like [Doosan] or a similar industrial giant would signal the licensing model is gaining significant traction against direct sales.

- The development of reversible SOFC/SOEC systems is a critical signal to monitor. A pilot project that successfully demonstrates economic viability in a “Hydrogen Valley” context could validate the technology’s future role as a flexible grid and energy production asset.

The questions your competitors are already asking

This report covers one angle of the manufacturers leading the market for hydrogen-ready SOFC systems. The questions that matter most depend on your work.

- Which SOFC manufacturers are gaining ground in the data center market, and which are positioned to run on 100% green hydrogen?

- What is the outlook for SOFC deployment in AI data centers by 2030, following the multi-gigawatt deals of 2026?

- Which data center operators, beyond Oracle, are adopting on-site SOFC power at gigawatt scale?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.