Ceres SOFC Fuel Flexibility Projects, Multi-GW Centrica Deal, $7.65 B in Agreements, and 4 Key Partnerships (2021 to 2026)

SOFC Commercial Scale Projects, Ceres Fuel Flexibility for Data Centers

Solid Oxide Fuel Cell (SOFC) adoption is accelerating as its inherent fuel flexibility allows for immediate, large-scale deployment on existing natural gas infrastructure, directly addressing the urgent power needs of grid-constrained sectors like data centers while providing a clear, de-risked pathway to future fuels like hydrogen and ammonia. The period from 2025 to today marks a definitive shift from smaller pilots to commercially significant, multi-megawatt agreements, validating the technology as a strategic asset for the energy transition.

- From 2021 to 2024, SOFC deployments were characterized by pilot projects and smaller-scale installations focused on validating efficiency and reliability. The period from 2025 to today has seen the emergence of gigawatt-scale strategic commitments, exemplified by the March 2026 partnership between Centrica and Ceres to deploy SOFC power across the UK and Europe, starting with natural gas and transitioning to hydrogen.

- Data centers, facing critical power shortages and grid connection delays, have become a primary adoption driver. In January 2026, Bloom Energy signed a Memorandum of Understanding with Korean partners to deploy its fuel-flexible SOFCs in the country’s rapidly growing data center market, following announcements of its systems powering data centers in the US.

- The maritime sector is actively pursuing SOFCs for decarbonization. A US-Korean partnership announced in January 2026 is developing ammonia-to-hydrogen SOFC systems to replace diesel generators on large vessels, while the EU-funded HELENUS project is developing next-generation SOFC solutions for sustainable shipping.

- Biogas provides a carbon-neutral fuel pathway for circular economy applications. Companies like Viking Line are using biogas to power ships, creating a renewable fuel supply chain that SOFCs can directly utilize for highly efficient combined heat and power (CHP) generation at industrial or municipal sites.

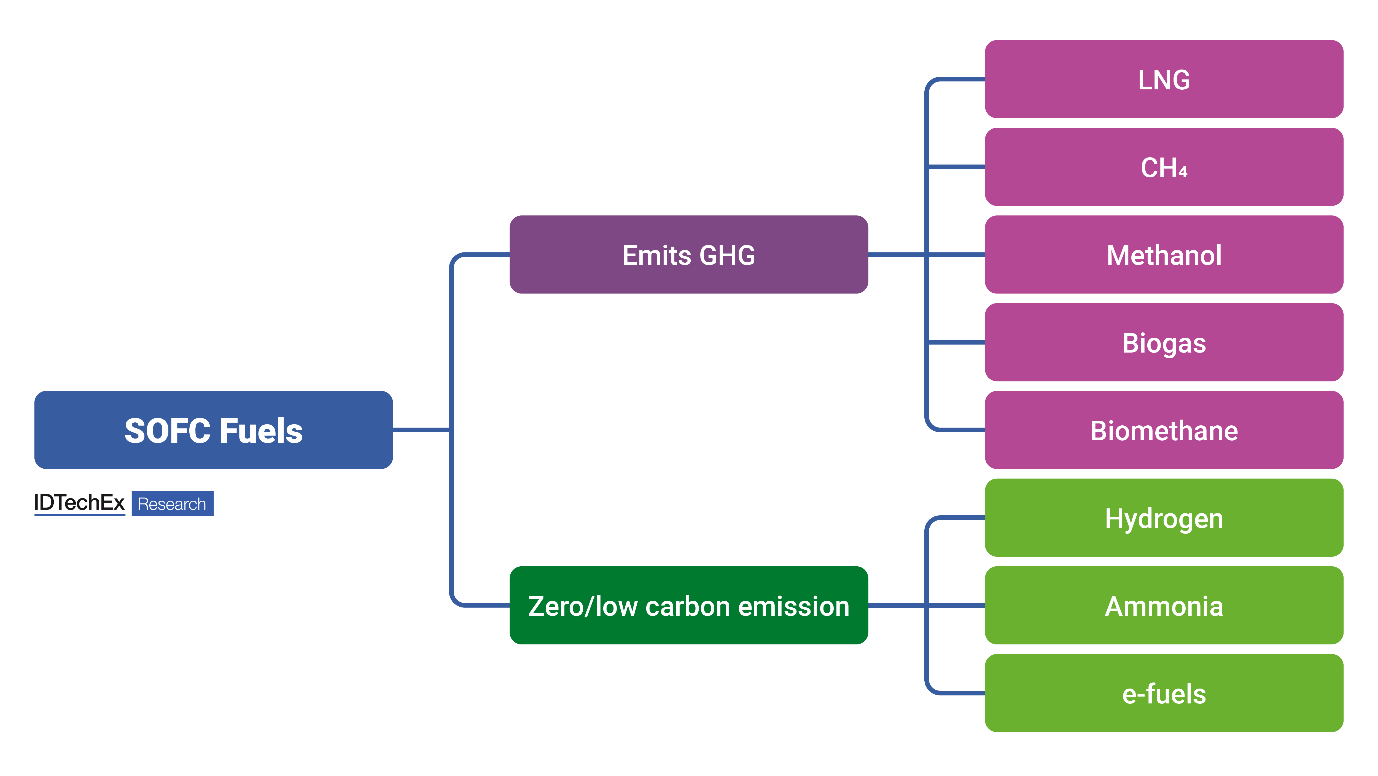

SOFCs Offer Flexible Decarbonization Path

This chart illustrates the core concept of fuel flexibility discussed in the section, showing how SOFCs can use current natural gas infrastructure while providing a clear path to future zero-carbon fuels like hydrogen.

(Source: IDTechEx)

$1.6 B Ammonia Project, Topsoe Green Fuel Investment Analysis

Major capital investments in 2026 are flowing not just into SOFC manufacturing but into the parallel green fuel infrastructure required for long-term decarbonization, with multi-billion-dollar green ammonia and hydrogen projects signaling market confidence that a viable supply chain for these future fuels is under construction. These investments are critical enablers for SOFCs to transition from a natural gas bridge to a fully zero-carbon power source.

- The scale of green ammonia investment is demonstrated by Topsoe’s March 2026 award of a Front-End Engineering Design (FEED) contract for a $1.6 billion green ammonia plant in Jordan, designed to produce 100, 000 tonnes per year.

- This follows Topsoe’s selection in January 2026 to provide its ammonia synthesis technology for the massive 4.4 GW NEOM green hydrogen project in Saudi Arabia, which will use ammonia as a hydrogen carrier for storage and transport.

- Government policy is reinforcing this trend, with the European Commission awarding €650 million in February 2026 to 14 cross-border projects aimed at modernizing Europe’s electricity and hydrogen grids, directly supporting the infrastructure needed for hydrogen-fueled SOFCs.

- Venture capital is also funding innovation in the fuel supply chain, with ammonia production startup Ammobia raising $7.5 million in January 2026 from industrial majors including Shell Ventures, Air Liquide, and MOL Switch to scale its alternative production process.

Table: Key Investments in SOFC and Alternative Fuel Infrastructure (2026)

| Company / Entity | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Topsoe (Jordan Project) | Mar 2026 | Awarded FEED contract for a $1.6 billion, 100, 000 tonne/year green ammonia plant, establishing a large-scale supply of a key SOFC future fuel. | Gasworld |

| European Commission | Feb 2026 | Awarded €650 million to 14 cross-border projects to modernize electricity and hydrogen grids, building the infrastructure for hydrogen-powered SOFCs. | Hydrogen News from Europe |

| Topsoe (Saudi Arabia Project) | Jan 2026 | Selected to supply ammonia synthesis technology for a 4.4 GW green hydrogen project, creating a massive hydrogen-as-ammonia production hub. | Gasworld |

| Ammobia | Jan 2026 | Raised $7.5 million from strategic investors to scale an alternative, sustainable ammonia production process, supporting fuel supply chain innovation. | H 2 View |

Ceres Multi-GW Centrica Deal, 4 Key SOFC Partnerships (2026)

Strategic partnerships in 2026 have pivoted from technology validation to securing large-scale market access and deployment channels, pairing SOFC developers with major energy distributors and industrial end-users. These collaborations are designed to accelerate the rollout of gigawatts of power, signaling that the technology is commercially ready for mainstream energy applications.

- The landmark partnership between Centrica and Ceres in March 2026 aims to deploy multi-gigawatts of SOFC power for data centers and industrial clients in the UK and Europe, starting with natural gas and establishing a clear path to hydrogen.

- In the marine sector, a January 2026 statement of intent between Eld Energy, MODEC, and Delta formalized collaboration to develop a Marine SOFC System, with mass production of Delta’s stacks scheduled to begin by the end of 2026.

- Amogy’s March 2026 partnership with an energy firm in Asia will deploy its ammonia-to-hydrogen cracking technology for fuel cells in the digital sector, providing a stable, zero-emission power source for applications like data centers.

- To address the power demands of the South Korean data center market, Bloom Energy signed an Mo U with local partners in January 2026 to expand the deployment of its fuel-flexible SOFC systems.

Table: Key SOFC Strategic Partnerships and Deployments (2026)

| Partners | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Centrica and Ceres | Mar 2026 | Strategic partnership to deploy multi-GW of on-site SOFC power in the UK and Europe, leveraging existing gas networks with a transition plan to hydrogen. | Ceres |

| Amogy and Asian energy firm | Mar 2026 | Partnership to deploy ammonia-to-hydrogen systems for fuel cells in Asia’s digital industries, targeting the data center market with zero-emission power. | Gasworld |

| Eld Energy, MODEC, and Delta | Jan 2026 | Statement of Strategic Intent to develop a Marine SOFC System for offshore power, with mass production of stacks planned by the end of 2026. | Eld Energy |

| Bloom Energy and Korean Partners | Jan 2026 | Non-binding Mo U to expand SOFC deployment across the Korean data center market, addressing rising power demands with a fuel-flexible solution. | Data Center Dynamics |

Europe vs. Asia, SOFC Fuel Flexibility Deployment Focus

Europe and Asia have solidified their positions as the primary centers for SOFC deployment and related fuel infrastructure development in 2026, though with distinct strategic drivers. Europe is advancing through strong, policy-driven hydrogen integration mandates, while Asia’s activity is centered on pressing industrial and commercial needs, particularly for reliable data center power and marine decarbonization.

- Europe’s growth is underpinned by robust policy and public funding. The EU’s €650 million investment in cross-border hydrogen infrastructure and initiatives like the Clean Hydrogen Partnership’s HORIZON-JU-CLEANH 2-2026 call create a favorable environment for hydrogen-ready technologies like SOFCs. The Centrica-Ceres deal is a direct commercial result of this environment.

- Asia, particularly South Korea and Japan, is a mature market for fuel cells and is now a key growth area for large-scale SOFCs. Partnerships like the Bloom Energy-Korea Mo U and Amogy’s entry into the region’s digital sector are driven by acute needs for grid-independent power for data centers and advanced manufacturing.

- The Middle East is emerging as a globally significant production hub for the green fuels SOFCs will require. Multi-billion dollar green hydrogen and ammonia projects in Saudi Arabia and Jordan, backed by companies like Topsoe, are being developed primarily for export, establishing the future supply chain for Europe and Asia.

- In North America, SOFC deployment continues to be strong for stationary power, where extensive natural gas infrastructure makes it an economically viable solution for providing behind-the-meter power to industrial customers and data centers facing grid constraints.

SOFC Technology Maturity for Fuel Flexibility in 2026

In 2026, SOFC technology has achieved full commercial maturity for stationary power generation using natural gas and biogas, with its readiness for pure hydrogen and ammonia now being proven through large-scale strategic commitments rather than small-scale pilots. The core technology is validated; the focus has shifted to manufacturing scale-up, cost reduction, and integration with emerging clean fuel supply chains.

SOFC Lifecycle Shows Fuel Versatility

This diagram directly visualizes the technology’s mature fuel flexibility discussed in the section, showing how the operational stage can accept various inputs from natural gas to hydrogen and ammonia.

(Source: ScienceDirect.com)

- While the 2021-2024 period focused on demonstrating reliability and efficiency in pilots, the market in 2025-2026 is defined by the commercial validation of SOFCs as a bankable, gigawatt-scale solution. High electrical efficiencies of over 60% are now a standard commercial offering, not a laboratory target.

- The technology’s fuel flexibility is its primary mature attribute. Systems from leading manufacturers like Bloom Energy, Ceres, and Doosan are explicitly marketed as “hydrogen-ready, ” capable of running on natural gas today and transitioning to hydrogen blends or pure hydrogen with minimal modification.

- The viability of ammonia as a fuel is moving from R&D to commercial application. Partnerships aimed at deploying ammonia-to-power systems in the marine and digital sectors in 2026 confirm that SOFCs are the preferred conversion technology for this critical hydrogen carrier.

- The principal remaining challenge is not technological but industrial: scaling manufacturing capacity to meet the explosive demand forecasted by market analysts, who predict the SOFC market could grow at a CAGR of over 30% to reach as high as $143.66 billion by 2040.

SOFC 2027 Outlook, Watch for Manufacturing Scale and Fuel Contracts

The critical factor for sustained SOFC growth into 2027 will be the industry’s ability to execute on manufacturing scale-up to meet the wave of demand solidified by major 2026 partnerships. The primary signal to watch is the announcement of new gigafactories and, equally important, the signing of the first large-scale, long-term offtake agreements for green hydrogen and ammonia tied directly to SOFC projects.

SOFC Market Set for Major Growth

This forecast quantifies the future market potential discussed in the 2027 outlook, visualizing the multi-billion dollar demand that new manufacturing scale-up and fuel contracts are aiming to capture.

(Source: Verified Market Research)

- If leading manufacturers announce new production facilities or significant expansions in late 2026 or early 2027, it will confirm that the supply side is responding to the demand signaled by multi-gigawatt deals like the Centrica-Ceres partnership.

- Watch for the first commercial-scale SOFC projects originally deployed on natural gas to begin operating on significant hydrogen blends or pure hydrogen, moving the “hydrogen-ready” promise into operational reality.

- A key risk is the timeline for green fuel availability. If large-scale green hydrogen and ammonia projects like those under development by Topsoe face significant delays, it could slow the pace of SOFC’s transition away from natural gas and temper the technology’s near-term decarbonization impact.

The questions your competitors are already asking

This report covers one angle of SOFC’s shift to commercial-scale deployment. The questions that matter most depend on your work.

- What is actually happening with the Centrica-Ceres partnership since the March 2026 announcement?

- What is the outlook for SOFC deployment in grid-constrained data centers by 2030?

- Which data center operators are adopting SOFCs for on-site primary power?

- SOFC performance on natural gas vs. hydrogen. What are the technical risks of fuel switching at commercial scale?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.