Rheinmetall SOFC Military Adoption, 51% of UAV Programs, 1 Ineratec E-Fuel Partnership, and 26 x Endurance Gains (2021 to 2026)

The adoption of fuel cells in military unmanned aerial vehicles (UAVs) has shifted from niche experimentation between 2021-2024 to the new standard for endurance and stealth platforms by 2026, with over half of new development programs now incorporating the technology. This transition is not an incremental upgrade but a strategic response to an operational environment that demands persistent surveillance, low acoustic signatures, and simplified logistical footprints. The clear limitations of battery power in endurance and internal combustion engines in stealth created a decisive opening for the operational advantages offered by fuel cells, particularly Solid Oxide Fuel Cells (SOFCs).

Military UAV Adoption, Rheinmetall SOFCs Power 51% of New Programs

The operational application of fuel cells in military UAVs has accelerated from isolated proofs-of-concept to widespread integration in frontline platforms, driven by a doctrinal need for persistence that battery power cannot supply. By 2026, fuel cells are no longer an alternative but a core enabler for next-generation ISR capabilities, with their adoption rate in new programs reaching a critical mass of 51%.

- During the 2021–2024 period, adoption was concentrated in specialized platforms like the Lockheed Martin Stalker. This UAV used a propane-fueled SOFC system developed with the U.S. Army Research Laboratory to demonstrate extended flight capabilities, establishing the initial validation for using common fuels in forward-deployed logistics.

- By 2026, the application expanded dramatically, with fuel cells becoming integral to new platforms designed for contested airspace. This is demonstrated by the combat deployment of the Hydrogen-Powered Raybird UAV in January 2026 for long-range, low-signature reconnaissance missions.

- This acceleration is driven by operational necessity, as the typical 30-minute flight time of battery-powered drones became a critical liability against advanced counter-UAS systems. In contrast, SOFC and PEM fuel cells deliver mission times exceeding 13 hours, representing a more than 26-fold increase in operational persistence.

- The technology is now applied across multiple mission sets beyond UAVs, with companies like Guardiaris and Cera Synth developing SOFC solutions to power entire off-grid military installations, which indicates a systemic shift toward fuel cell-based energy resilience.

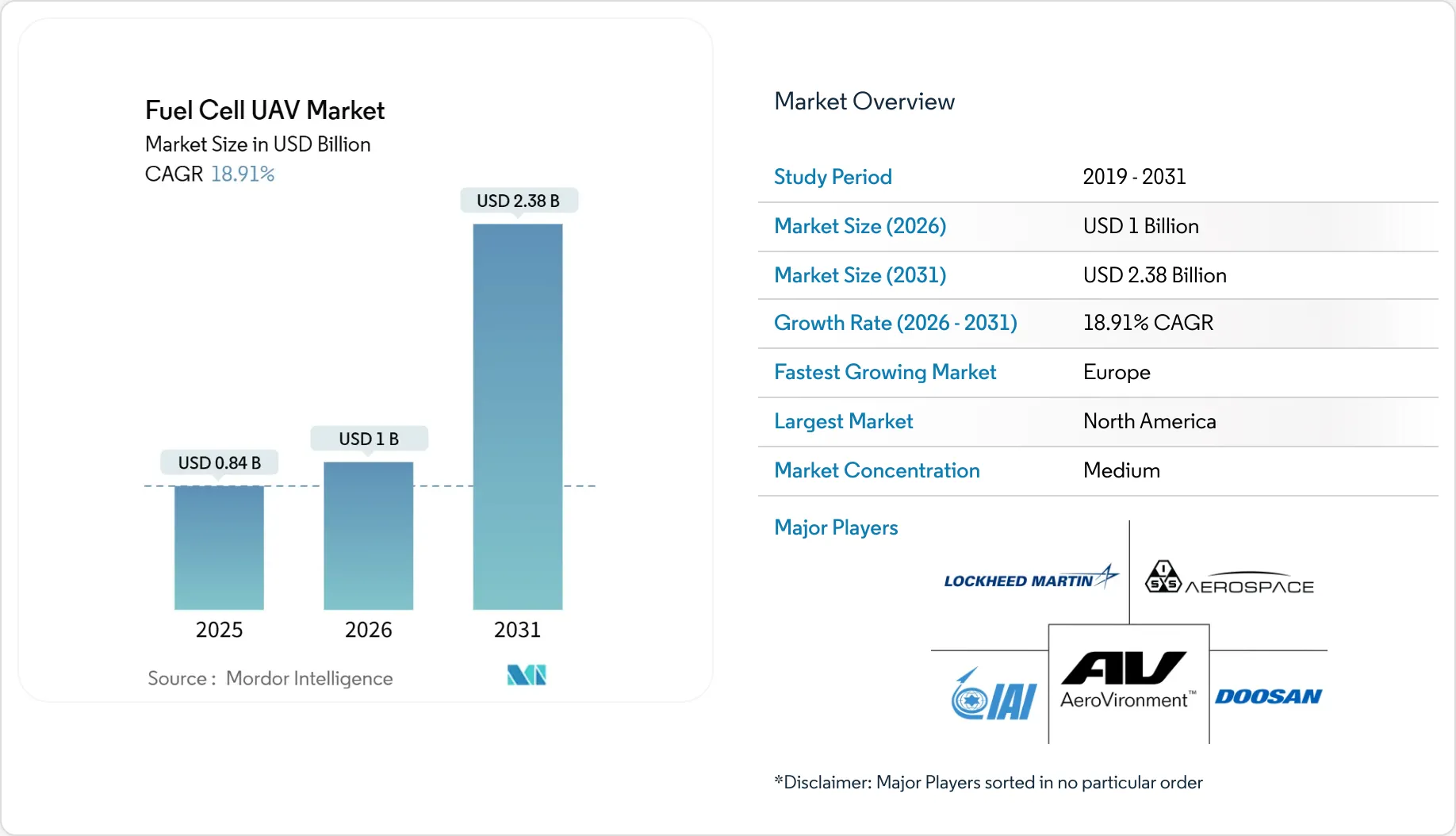

Fuel Cell UAV Market to Surpass $2B

This chart quantifies the significant market growth for fuel cells in UAVs, reinforcing the section’s point about adoption reaching a ‘critical mass’ of 51%.

(Source: Mordor Intelligence)

Rheinmetall 1 Ineratec E-Fuel Alliance Signals Logistics Overhaul (2025 to 2026)

Strategic partnerships formed in 2026 are focused on solving the final logistical and technological barriers to widespread SOFC deployment, particularly regarding in-field fuel production and system efficiency. These collaborations are moving SOFCs from being a platform-specific component to an integrated part of a resilient, field-based energy ecosystem.

- The joint development agreement between German defense firm Rheinmetall and e-fuels producer Ineratec is a critical enabler. It aims to create mobile systems that can produce synthetic hydrocarbon fuels from CO₂ and hydrogen in the field, which would eliminate vulnerable liquid fuel supply chains.

- Technology-sharing agreements are accelerating performance improvements, such as the licensing deal announced in April 2026 between Advent Technologies and EH Group. This partnership advances High-Temperature PEM (HTPEM) fuel cells by combining innovative stack designs with advanced materials for greater efficiency.

- Major industrial players are leveraging their commercial scale for defense applications. General Motors is expanding its HYDROTEC fuel cell platform to create mobile power generators for military support, which lowers the cost curve through automotive-scale production.

- The broader commercial SOFC market, where companies like Bloom Energy and Doosan Fuel Cell are expanding, creates a competitive ecosystem that directly benefits defense procurement by driving down costs and enhancing reliability for all applications.

Key Military Fuel Cell Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Rheinmetall / Ineratec | Mar. 2026 | Joint development of a mobile e-fuel production system to produce synthetic fuels from green hydrogen. The goal is to enhance defense resilience and simplify fuel logistics in the field. | H 2 View |

| Advent Technologies / EH Group | Apr. 2026 | License and joint development agreement for Advent to use EH Group’s technology to advance High-Temperature PEM (HTPEM) fuel cells for applications including defense. | Stock Titan |

| General Motors (GM) | Jan. 2026 | Expansion of HYDROTEC fuel cell applications beyond vehicles to develop mobile and fixed power systems that can support military operations and EV charging. | Renewable Innovations |

US and Germany Lead SOFC Military Development and Deployment

The United States and Germany have emerged as the epicenters for military fuel cell development and deployment, driven by established defense industrial bases and direct government support. Meanwhile, real-world combat in Ukraine provides critical, high-stakes validation of the technology’s operational benefits.

North America and Europe Dominate Market

This chart’s regional breakdown supports the section’s claim that the US and Germany (representing North America and Europe) are leading military fuel cell development.

(Source: MarketsandMarkets)

- The United States leads in foundational R&D and system integration. This includes the U.S. Army Research Laboratory’s work on the Lockheed Martin Stalker, corporate initiatives from General Motors in Michigan, and federal funding such as the $350, 000 grant in Connecticut to build out a domestic defense supply chain.

- Germany is focused on industrial and logistical solutions, highlighted by Rheinmetall‘s e-fuel partnership with Ineratec and SFC Energy‘s specialization in ruggedized, long-lasting fuel cells designed specifically for defense customers.

- In January 2026, Japan contributed a key technological breakthrough with a palm-sized SOFC microreactor capable of a five-minute startup. This innovation directly addresses a historical barrier for using SOFCs in time-sensitive tactical situations.

- The use of low-noise, hydrogen-powered combat drones in Ukraine, as reported in April 2026, offers battlefield validation of the technology’s stealth and endurance benefits, providing invaluable performance data for NATO and allied military planners.

SOFCs Reach Tactical Viability, Rheinmetall Addresses Startup and Fuel Hurdles

By 2026, Solid Oxide Fuel Cells have matured from a promising but impractical technology into a tactically viable power source for military applications, having overcome the critical barriers of slow start-up times and complex fuel-supply logistics. This maturation has been central to their adoption in demanding UAV programs.

- Between 2021-2024, SOFCs were primarily considered for stationary or long-duration, non-tactical roles because their start-up times often exceeded 30 minutes, which limited their utility for rapid deployment scenarios.

- A key validation point arrived in January 2026 when a Japanese research team demonstrated an SOFC microreactor that reached its 600°C operating temperature in just five minutes. This milestone effectively eliminated the start-up delay as a major operational obstacle.

- The issue of fuel logistics, once a significant challenge, is now a strategic advantage. Unlike PEM cells that often require pure hydrogen, the fuel flexibility of SOFCs allows them to run on common hydrocarbon fuels. This capability is being operationalized by the Rheinmetall and Ineratec mobile e-fuel production system.

- This maturation is further supported by the broader commercial market, where companies like Ceres Power are scaling production. This commercial growth enhances the robustness and lowers the cost of components used in military-grade systems.

SWOT Analysis, Rheinmetall SOFC Military UAV Applications

The strategic value of SOFCs in military applications is defined by a clear set of operational strengths that directly counter modern threats. Market growth and technological maturation have effectively mitigated historical weaknesses, shifting the focus from viability to scalability.

- The primary strengths of extended endurance, low acoustic signature, and fuel flexibility are validated by operational platforms and market data.

- Weaknesses such as long start-up times have been technically resolved through innovations like miniaturized microreactors, shifting the focus to manufacturing scale and cost reduction.

- Opportunities are expanding as sophisticated counter-UAS threats grow and the commercial fuel cell market drives down technology costs, making wider deployment feasible.

- Threats remain centered on the logistical complexity of integrating new fuel types during a transitionary phase and competition from incremental improvements in battery technology for shorter-range missions.

SWOT Analysis for SOFC in Military Applications

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | High energy density demonstrated in prototypes (e.g., Lockheed Martin Stalker). Fuel flexibility (propane) proven as a concept. | Endurance of >13 hours operationally deployed (Raybird UAV). Low acoustic signature validated in combat (Ukraine). Fuel flexibility extended to e-fuels (Rheinmetall). | Theoretical advantages were validated in real-world combat and logistics-focused partnerships, moving from prototypes to standard operational capability. |

| Weaknesses | Long start-up times (>30 minutes) limited tactical use. High system costs. Perceived logistical complexity of new fuels. | Start-up times reduced to 5 minutes in new microreactors. Costs decreasing due to commercial market scale-up (e.g., Bloom Energy). | Key technical barriers were resolved through targeted R&D, and cost concerns are being mitigated by crossover from the rapidly growing commercial sector. |

| Opportunities | Growing military need for persistent ISR. Early government R&D funding and interest from defense contractors. | Rise of sophisticated C-UAS systems makes stealth and endurance a top priority. Strong market growth (30%+ CAGR forecasts) attracts investment. Mobile e-fuel production creates energy independence. | The threat environment evolved to perfectly match the core strengths of fuel cells, turning a niche capability into a strategic necessity. |

| Threats | Competition from improving Li-ion battery technology. Limited supply chain for military-grade components. | Battery tech still cannot match fuel cell endurance for long-range missions. Supply chain is being regionalized (e.g., CONNSTEP grant). | The performance gap between fuel cells and batteries for long-endurance missions widened, solidifying the fuel cell’s role. Supply chain risks are being actively addressed. |

SOFCs to Standardize in Ground Power, Rheinmetall Paves Way

If mobile e-fuel production systems like the Rheinmetall-Ineratec platform prove effective in field trials through 2027, watch for SOFC adoption to rapidly expand from UAVs to become the standard for all tactical ground power generation, displacing diesel generators.

SOFC Market Poised for Explosive Growth

This strong market growth forecast to $9.3B supports the section’s prediction that SOFC adoption will rapidly expand from UAVs to larger markets like ground power.

(Source: Research and Markets)

Validated SOFCs Drive New Technology Revenue

This chart shows the market-level outcome of the technical validations detailed in the SWOT, illustrating how overcoming weaknesses has driven a major revenue shift.

(Source: MarketsandMarkets)

- The successful deployment of fuel-flexible SOFCs in UAVs serves as the critical validation for their use in other power-hungry applications, such as command posts, communication hubs, and forward operating bases where silent, efficient power is critical.

- The ability to produce fuel on-site would resolve one of the largest points of failure for deployed military forces: the reliance on vulnerable fuel convoys. This directly supports the strategic military objective of achieving energy independence at the tactical edge.

- Signals to watch include procurement announcements for mobile SOFC generators from the U.S. Army or allied nations and new partnerships between defense primes and SOFC manufacturers focused on ground-based systems, building on the model established by GM‘s HYDROTEC platform.

The questions your competitors are already asking

This report covers one angle of the strategic shift to fuel cell-powered military UAVs. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the military UAV fuel cell market?

- Rheinmetall’s activities in e-fuels. Is the Ineratec partnership progressing from pilot to deployment?

- How does SOFC power compare to battery-electric for endurance and stealth in military UAVs?

- Which military UAV programs are adopting SOFC solutions?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.