The Great Gridlock of 2025: How Power Scarcity Stalls Data Center Growth

Industry Risk Analysis 2025: Why Power Availability Now Dictates Data Center Viability

Industry Risk Analysis 2025: Why Power Availability Now Dictates Data Center Viability

The primary constraint on data center expansion has decisively shifted from capital and land availability to power procurement and grid interconnection, creating multi-year delays and forcing a strategic re-evaluation of deployment models. Power availability is no longer an operational expense to be managed; it is the fundamental gating factor for growth in the AI era.

- Between 2021 and 2024, industry focus was on rapid construction to meet predictable cloud demand, with power treated as a readily available utility. While demand grew, it was largely accommodated by existing utility planning.

- From 2025 onward, the explosive, AI-driven demand for power has overwhelmed grid capacity, transforming energy from a simple line item into an existential risk. Hyperscalers are now designing campuses requiring 200 MW to 500 MW, with some connection requests exceeding 1, 000 MW, a scale that local grids cannot support without years of upgrades.

- The consequences are now tangible project delays. Interconnection wait times in key U.S. markets have ballooned to 7-10 years, according to Blackstone. Virginia’s “data centre alley” faces waitlists of up to seven years, and Google has publicly stated that grid connection is now its single biggest challenge.

- This shift is confirmed by utility forecasts. Over the past year, U.S. grid planners nearly doubled their five-year load growth projections from 2.6% to 4.7%, a direct result of unanticipated data center demand that their infrastructure was not built to handle.

Investment Surge: Trillions Mobilized to Bridge the Data Center Power Gap

A wave of multi-billion-dollar investments launched in late 2024 and 2025 confirms the convergence of the energy and technology sectors, as hyperscalers and financiers directly fund power infrastructure to de-risk data center expansion. This represents a strategic shift from being a passive energy consumer to an active infrastructure investor.

- The scale of required capital is immense, with Blackstone estimating that over $2 trillion in investment is needed for data centers and supporting power infrastructure in the next five years. This acknowledges that the public grid cannot and will not deliver the required power on the industry’s timeline.

- Major financial and tech players are creating dedicated funds to co-develop power and data infrastructure. In October 2024, KKR and Energy Capital Partners announced a $50 billion strategic partnership explicitly to support AI growth through integrated investments.

- This trend accelerated with Microsoft and Black Rock launching a $30 billion investment fund in September 2024 to build new data centers and the energy assets to power them, bypassing traditional utility development cycles.

- In December 2024, Google, Intersect Power, and TPG committed $20 billion by 2030 to build clean energy infrastructure specifically to enable new U.S. data center capacity, directly linking power generation investment to compute expansion.

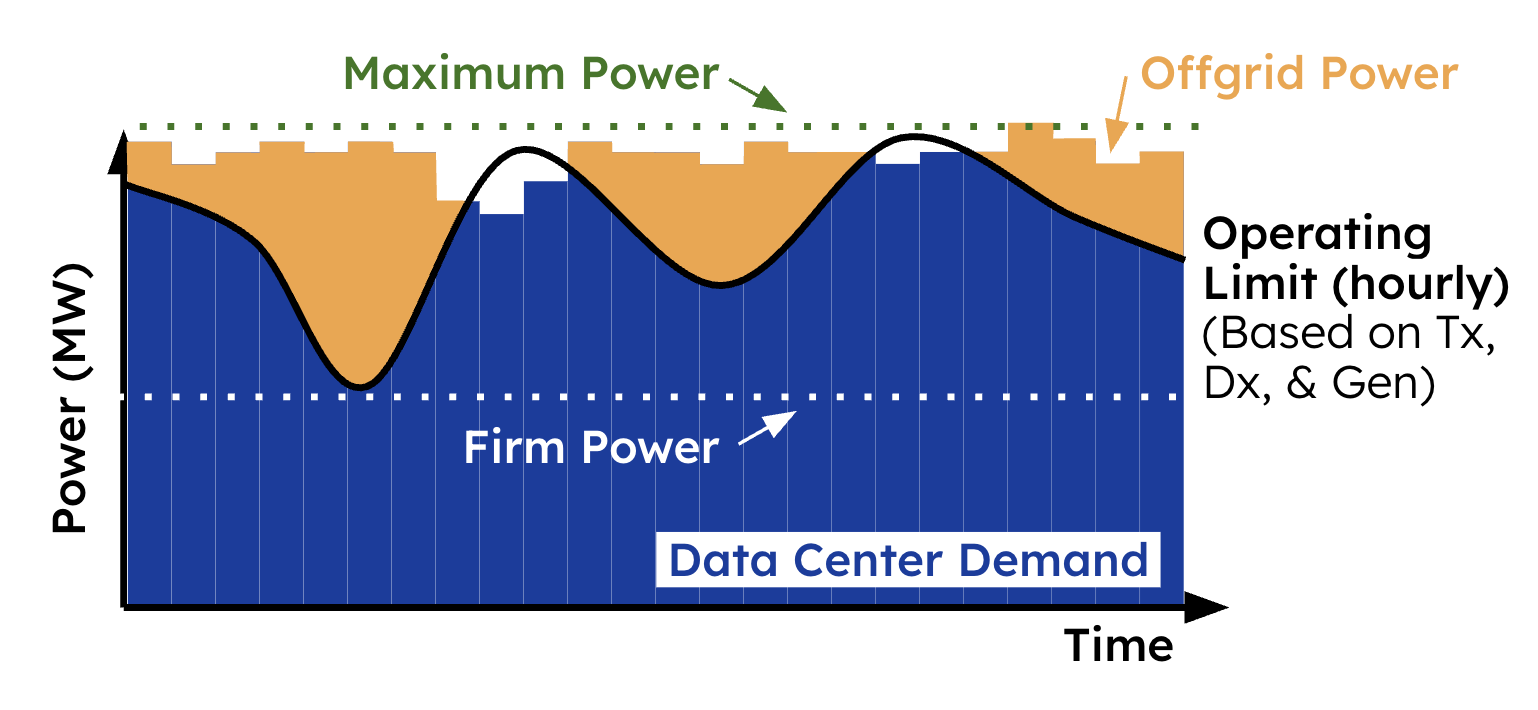

Data Center Demand Creates A Widening Power Gap

This chart visualizes the ‘power gap’ that the investments mentioned in the section are trying to bridge, showing how data center demand regularly exceeds the grid’s operating limits.

(Source: Camus Energy)

Table: Recent Major Investments in Data Center Power Infrastructure

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Google, Intersect Power, TPG | 2024 – 2030 | A $20 billion investment to build out renewable power infrastructure, enabling the development of new U.S. data center capacity powered by dedicated clean energy. This directly ties new generation to new compute. | Google, Intersect Power, TPG Launch $20 Billion Data … |

| Blackstone | 2024 – 2029 | An estimated $2 trillion in required investment to meet global demand for data centers and the supporting power infrastructure. This figure highlights the market-wide recognition of the infrastructure deficit. | The Convergence of Data Centers and Power |

| KKR & Energy Capital Partners (ECP) | October 2024 | A $50 billion strategic partnership to invest in data centers and the power generation assets needed to support AI-driven growth, creating a vertically integrated development model. | ECP Enters into $50 Billion Strategic Partnership with KKR |

| Microsoft & Black Rock | September 2024 | A $30 billion investment fund to finance the construction of new data centers and the energy infrastructure required to power them, aimed at accelerating deployment by directly funding power solutions. | Microsoft, Black Rock Launch $30 B AI Data Center … |

Strategic Alliances in 2025: Tech and Energy Forge Joint Ventures to Secure Power

To bypass gridlock, data center operators are now forming direct joint ventures and long-term power agreements with energy producers, securing dedicated generation capacity as a core component of their expansion strategy. These partnerships go beyond standard renewable energy credits to include co-development and physical power delivery.

Data Center Demand Growth Dwarfs National Grid Expansion

This chart powerfully illustrates the ‘gridlock’ forcing strategic alliances by showing projected data center power demand growth far outpacing the growth of entire national grids.

(Source: 451 Alliance – Blog)

- In a model of deep integration, Echelon Data Centres and renewable energy producer Iberdrola formed a €2 billion joint venture in 2025. The objective is to develop data center sites across Spain where Iberdrola will provide 100% of the required power from its own renewable assets.

- To secure its European expansion pipeline, Equinix announced a pre-order power agreement in August 2025 for 500 MWe with Stellaria, an alternative energy provider incubated by Schneider-Electric. This move secures power capacity years in advance of facility construction.

- Signaling a more symbiotic grid relationship, Google is actively re-engineering its data centers to function as flexible loads. By shifting workloads and using on-site storage, it can reduce demand during peak grid hours, providing stability services to utilities in exchange for more favorable operating conditions.

Table: Key Strategic Partnerships for Data Center Power

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Equinix & Stellaria (Schneider-Electric) | August 2025 | A pre-order power agreement for 500 MWe to support Equinix‘s European data center expansion. This secures large-scale power capacity ahead of time, de-risking future builds. | Equinix Collaborates with Leading Alternative Energy … |

| Echelon Data Centres & Iberdrola | August 2025 | A €2 billion joint venture to co-develop data centers in Spain. Iberdrola will supply 100% of the power from its renewable portfolio, creating a fully integrated energy and data campus. | Power progress in your global data center expansion |

| Google & Grid Operators | August 2025 | An initiative to make its data centers more flexible, shifting computational tasks to times of lower grid stress. This strategy turns a data center from a static load into a dynamic grid asset. | How we’re making data centers more flexible to benefit … |

Geographic Diversification: How Power Constraints Are Redrawing the Global Data Center Map

Severe power constraints in established hubs like Northern Virginia and Silicon Valley are forcing data center development to disperse into secondary markets and regions with available energy capacity, fundamentally decentralizing digital infrastructure. The primary site selection criterion has shifted from network latency to power availability.

Power Constraints Are Redrawing the US Data Center Map

These maps directly support the section’s theme, visualizing the intense power load in hubs like Northern Virginia and projecting how data centers will strain state grids, forcing geographic diversification.

(Source: POWER Magazine)

- Between 2021 and 2024, development was heavily concentrated in primary markets with dense fiber connectivity. Northern Virginia was the epicenter, absorbing massive capacity additions annually.

- By 2025, these hubs are saturated. Northern Virginia now faces grid connection waitlists of up to seven years, and the European Union reports delays of two to ten years. This has effectively placed a moratorium on new large-scale development in the world’s most desirable digital locations.

- This gridlock is forcing a strategic geographic shift. Developers are now actively building in secondary markets where power is more accessible, even if connectivity is less optimal. The Echelon/Iberdrola partnership in Spain is a prime example of this “power-first” site selection strategy.

- New growth frontiers are emerging as a direct result. Canadian regulators are reviewing data center applications totaling 15 GW, indicating a potential surge in a region with significant hydroelectric resources. This pattern of moving to energy-rich areas will redefine the global data center map over the next five years.

Technology Response: How On-Site Generation and Grid-Enhancing Tech Are Mitigating Constraints

In response to grid failures, the data center industry is rapidly deploying commercially available on-site power generation and grid-enhancing technologies (GETs) to create resilient, independent energy systems. The strategy is moving from grid-reliance to grid-independence and grid-optimization.

Tech Efficiencies Could Halve Data Center Power Demand

This chart perfectly matches the ‘Technology Response’ theme by forecasting how innovations like liquid cooling and processor efficiency can significantly mitigate future power requirements.

(Source: Energeia-USA.com)

- In the 2021-2024 period, on-site power typically meant diesel generators for backup purposes only. The primary operational model was complete reliance on the public utility grid for continuous power.

- The market in 2025 shows a clear pivot to “behind-the-meter” prime power. A recent survey indicates that 27% of data center facilities are expected to be fully powered by on-site generation by 2030, a direct response to grid unreliability.

- Commercially mature solutions are now being deployed at scale for primary power, including natural gas turbines from firms like GE Vernova and solid-oxide fuel cells from providers like Bloom Energy, which offer a grid-independent power source.

- As a parallel strategy, operators are deploying GETs to maximize existing grid infrastructure. For example, Switched Source is deploying its Phase-EQ technology, which can unlock up to 25% more capacity on existing power lines, providing a near-term solution while new generation is built.

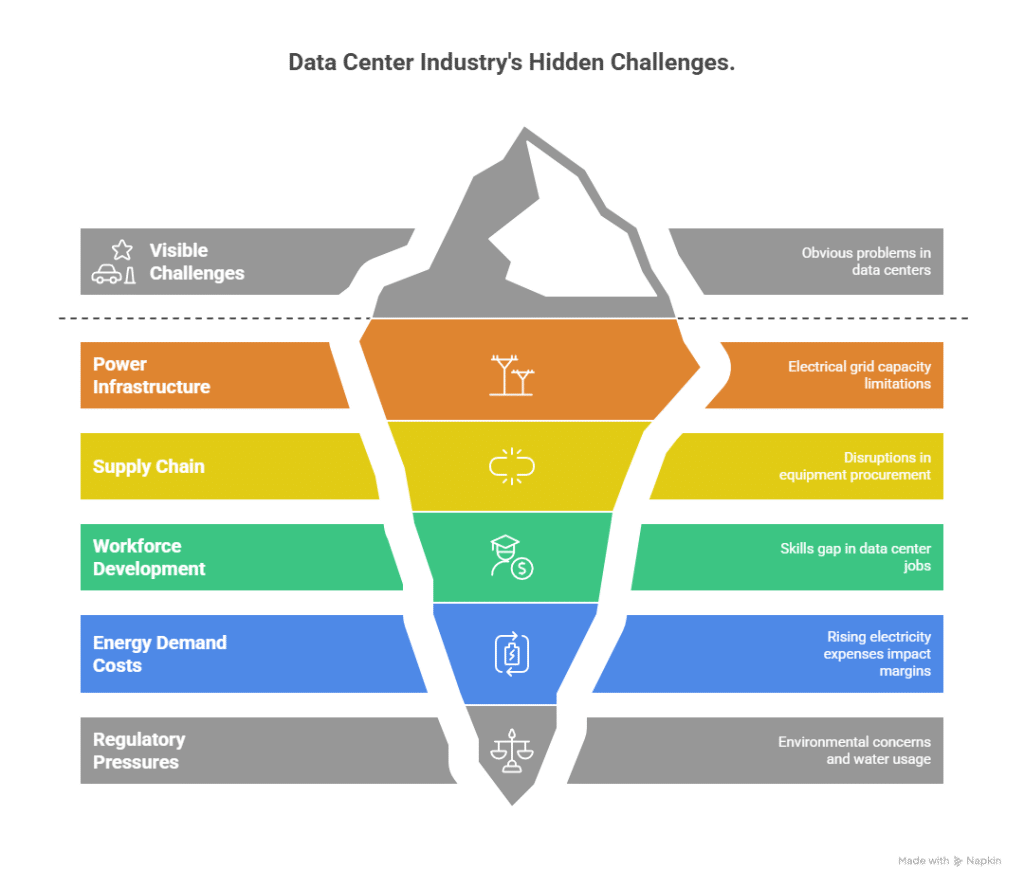

SWOT Analysis: Navigating Data Center Power Constraints in 2025

The data center industry’s primary strength, its explosive growth, has created a critical weakness in its dependency on inelastic grid infrastructure. This threat is also creating opportunities for innovation in energy strategy, market consolidation, and the development of new, integrated asset classes.

Power Infrastructure Is the Core Data Center Challenge

This infographic serves as a perfect introduction to a SWOT analysis, identifying ‘grid capacity limitations’ as the critical underlying weakness and threat facing the industry.

(Source: The Network Installers)

- Strengths: The sector continues to attract massive capital and is driven by non-negotiable demand from AI and cloud computing.

- Weaknesses: An extreme dependency on aging public grid infrastructure with multi-year development timelines has become the primary bottleneck.

- Opportunities: The crisis is forcing the creation of new business models, including grid-interactive data centers and co-located power generation, driving innovation and creating a competitive moat for energy-savvy operators.

- Threats: The inability to secure power in key markets is no longer a future risk but a present reality, leading to project cancellations, operational curtailments, and rising costs.

Table: SWOT Analysis for Data Center Grid Constraints

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Massive capital availability and rapid construction cycles (18 months) met predictable demand growth. | Continued high demand for AI/cloud attracts trillions in investment (Blackstone, Mc Kinsey forecasts). Ability to fund large-scale energy projects directly. | The strength in construction speed is now neutralized by the weakness in power connection speed. Financial strength is being redirected from building servers to building power plants. |

| Weaknesses | Rising energy consumption was viewed as a manageable operational cost (OPEX). | Extreme dependency on public grid infrastructure that takes a decade to build. Grid connection is now the primary project bottleneck and strategic risk. | The weakness has been validated and elevated from an operational line item to the single greatest threat to growth, as confirmed by Google and market-wide delays. |

| Opportunities | Pursuing renewable Power Purchase Agreements (PPAs) primarily for environmental, social, and governance (ESG) goals and cost management. | Develop new business models (grid-interactive data centers), pioneer on-site prime power (fuel cells, SMRs), and enter new geographic markets based on energy availability. | The opportunity has shifted from ESG optimization to securing fundamental business viability. Energy strategy is now a source of competitive advantage and market consolidation. |

| Threats | Volatile energy prices and the reputational risk of high carbon footprints. | Inability to expand in key markets due to grid unavailability. Gartner predicts 40% of AI data centers will be constrained by 2027. Projects are being delayed or canceled. | The threat has evolved from price risk to existential risk. The inability to get a grid connection means a project cannot be built, regardless of capital or demand. |

2025 Outlook: Expect a Bifurcated Market Defined by Energy Strategy

If hyperscalers and their financial partners succeed in deploying dedicated power infrastructure at scale, watch for an acceleration of market consolidation and a divergence between energy-independent operators and grid-dependent players who will face significant growth limitations.

Generative AI Drives Explosive Data Center Power Demand

This forecast provides the context for the ‘2025 Outlook,’ showing the massive surge in GenAI power demand that will force the market to bifurcate between energy-independent and grid-dependent players.

(Source: Boston Consulting Group)

- If this happens: The multi-billion-dollar investment funds from entities like Black Rock/Microsoft and KKR/ECP successfully finance and build co-located power generation and data centers within the next 3-5 years, creating a private, reliable power ecosystem for their operations.

- Watch this: Monitor the announcements of new large-scale data center campuses being built in conjunction with dedicated power plants (gas, renewables, or future SMRs). Track whether interconnection queue times in key markets begin to stabilize for projects that bring their own power source to the grid.

- These could be happening: Smaller data center operators without the capital for energy joint ventures will be acquired or forced into niche markets. A new class of “energy-first” infrastructure funds and real estate investment trusts (REITs) will emerge. Utilities, faced with losing their largest customers, will adopt new partnership models to co-invest with tech companies, effectively accelerating grid expansion.

Frequently Asked Questions

What is the single biggest challenge for data center growth in 2025?

The single biggest challenge has shifted from capital or land to power availability. The explosive demand for power driven by AI has overwhelmed grid capacity, leading to multi-year delays (7-10 years in some U.S. markets) for connecting new data centers to the electrical grid. This has become the fundamental factor limiting expansion.

How are tech and finance companies responding to these power shortages?

They are moving from being passive energy consumers to active infrastructure investors. Major players like Microsoft, Google, Blackstone, and KKR are launching multi-billion-dollar funds and partnerships (ranging from $20B to $50B) to directly finance and co-develop new power generation assets specifically to support their data centers, bypassing traditional utility timelines.

Why can’t utility companies simply provide the power that’s needed?

The demand has grown unexpectedly fast, overwhelming previous plans. U.S. grid planners recently doubled their five-year load growth projections directly because of unanticipated data center needs. The public grid infrastructure was not built to handle the scale of modern AI campuses (which can require over 1,000 MW), and upgrading or building new transmission and generation capacity is a slow process that takes many years.

How are power constraints changing the location of new data centers?

Established hubs like Northern Virginia are saturated, with long waitlists for power connections. This gridlock is forcing a geographic shift to secondary markets where energy is more accessible. Developers are now using a “power-first” site selection strategy, leading to new growth in energy-rich regions like Spain and Canada, which is redrawing the global data center map.

What technologies are being used to overcome grid limitations?

Data center operators are deploying two main strategies. First, they are installing on-site or “behind-the-meter” prime power generation, such as natural gas turbines and fuel cells, to operate independently from the grid. Second, they are using Grid-Enhancing Technologies (GETs) to unlock more capacity from existing power lines as a near-term solution while new generation is constructed.