CCUS in 2026: Why Strategic Cancellations Signal a New Era for Carbon Capture Projects

Project High-Grading Defines the New CCUS Commercialization Strategy

Major energy firms are pivoting from broad, ambitious carbon capture portfolios to a selective “high-grading” strategy, prioritizing projects with clear economic returns and integration with legacy assets over speculative ventures. This marks a significant shift from the expansive project announcements seen in prior years to a more focused, financially disciplined approach to deploying Carbon Capture, Utilization, and Storage (CCUS).

- The 2021-2024 period was marked by geographically diverse project announcements, including collaborations like BP‘s plan with Linde for a US Gulf Coast CCS hub and explorations in China with CNPC. This demonstrated a wide-ranging approach to establishing a global CCUS footprint.

- In contrast, the period from January 2025 to today shows a dramatic narrowing of focus toward executing large-scale, de-risked hubs. This is exemplified by the final investment decision (FID) on the $7 billion Tangguh UCC project in Indonesia, a project directly linked to enhancing natural gas production.

- This strategic pivot is defined by high-profile cancellations of projects previously seen as cornerstones of decarbonization plans. Notable examples include BP’s termination of its 1.2 GW H 2 Teesside blue hydrogen project in December 2025 and the suspension of its Indiana CCS project in June 2025.

- The clear implication is that CCUS is being deployed not as a universal climate tool, but as a pragmatic instrument to prolong the economic life of profitable fossil fuel operations, such as using captured CO₂ for Enhanced Gas Recovery (EGR) at the Tangguh facility.

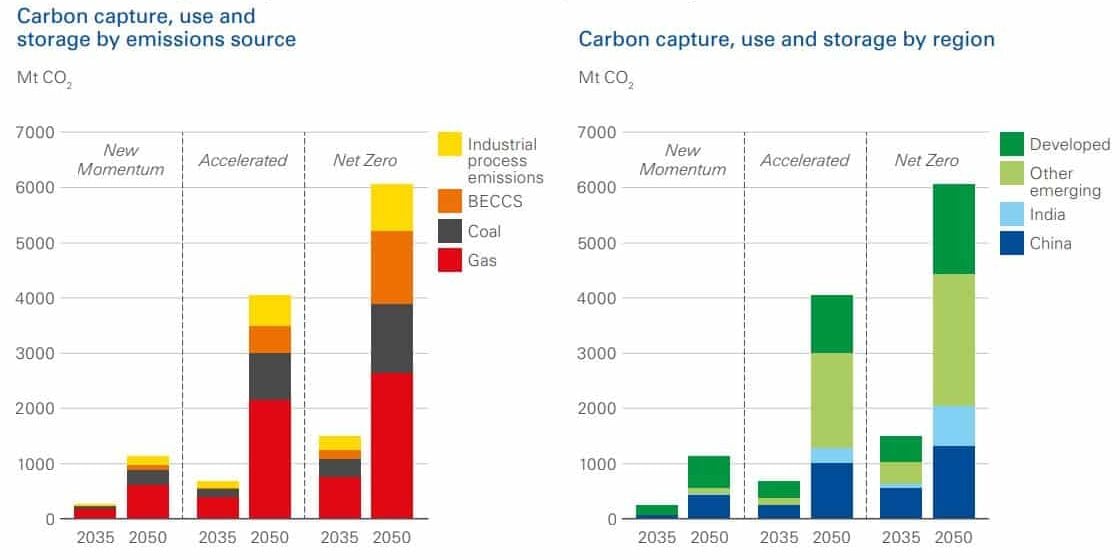

Chart Outlines CCUS Growth Scenarios to 2050

This chart illustrates the different strategic pathways available for CCUS growth, providing high-level context for the article’s discussion of a new, selective commercialization strategy.

(Source: CarbonCredits.com)

Cancellations and Budget Cuts Reveal a Pivot Back to Core Assets

Major project cancellations and significant capital reallocations in 2025 reveal a clear corporate strategy to de-prioritize speculative low-carbon ventures in favor of maximizing returns from core oil and gas operations. This financial discipline is forcing a market-wide reassessment of which CCUS projects are commercially viable versus merely technically feasible.

- BP‘s strategic reset announced in February 2025 provides a stark example of this trend. The company cut its annual energy transition spending by over $5 billion while simultaneously increasing its planned oil and gas investment by approximately 20% to $10 billion per year.

- This financial pivot directly led to the indefinite suspension of the planned blue hydrogen and CCS project at the Whiting Refinery in Indiana in June 2025, halting a key decarbonization initiative in the US Midwest.

- The most significant retreat was the cancellation of the 1.2 GW H 2 Teesside project in the UK in December 2025. The move stalled a flagship blue hydrogen project, citing land use conflicts with a planned AI data center, which highlights how low-carbon projects are weighed against other, more immediately profitable land uses.

- These actions demonstrate that even large-scale projects within major industrial hubs are vulnerable to cancellation if they fail to meet stringent near-term financial criteria or lack guaranteed offtake agreements for their low-carbon products.

Table: Key CCUS and Blue Hydrogen Project Cancellations (2025)

| Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| H 2 Teesside | December 2025 | BP cancelled its 1.2 GW blue hydrogen project in the UK. The project was intended to capture its CO₂ emissions for storage via the Northern Endurance Partnership infrastructure. | Enerdata |

| Indiana CCS Project | June 2025 | BP indefinitely suspended its blue hydrogen and CCS project at its Whiting Refinery. It aimed to capture and store CO₂ to enable blue hydrogen production. | Fuel Cell Works |

Partnership Strategy Shifts From R&D to Project Execution

The nature of CCUS partnerships is evolving from broad, early-stage research collaborations to focused, project-specific execution consortiums. This change is designed to de-risk massive capital expenditures and secure complex supply chains for a handful of sanctioned mega-projects, rather than exploring a wide array of future possibilities.

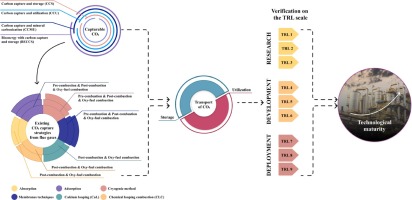

Diagram Maps CCUS Path to Technological Maturity

This diagram visually represents the shift from early-stage research (low TRL) to full-scale deployment (high TRL), perfectly matching the section’s theme of partnerships evolving from R&D to project execution.

(Source: ScienceDirect.com)

- A primary signal of this shift was the conclusion of BP‘s 25-year, $56 million Carbon Mitigation Initiative with Princeton University in September 2025. The end of this long-term R&D alliance indicates a move away from foundational research.

- In contrast, partnership activity in 2025 and 2026 is centered on project delivery. The Northern Endurance Partnership (a venture of BP, Equinor, and Total Energies) awarded a series of major contracts to firms including SLB, Halliburton, and Noble Corporation to build its UK offshore CO₂ storage network.

- Similarly, to advance its $7 billion Tangguh UCC project, BP awarded critical construction and supply contracts to Saipem, Leighton Asia, and Tenaris in late 2024 and 2025, solidifying the execution supply chain.

- Even new technology partnerships are now geared toward immediate commercial application. This is seen in the February 2026 selection of FT CANS™ technology, co-developed by Johnson Matthey and BP, for a commercial Sustainable Aviation Fuel (SAF) plant in the UK.

Table: Evolution of BP’s CCUS Partnerships (2024-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Carbon Neutral Fuels / Johnson Matthey | February 2026 | Technology licensing partnership to use BP‘s co-developed FT CANS™ technology in a commercial SAF plant, focusing on the “Utilization” aspect of CCUS. | Hydrocarbon Processing |

| Princeton University | September 2025 | Concluded a 25-year, $56 million research partnership (Carbon Mitigation Initiative), signaling a strategic shift away from long-term, exploratory R&D. | Princeton Alumni Weekly |

| Northern Endurance Partnership Contractors (SLB, Halliburton, etc.) | 2025 | A series of execution-focused contracts awarded to build out the CO₂ transport and storage infrastructure for the UK’s East Coast Cluster. | SLB |

| Saipem | November 2024 | Awarded a $1.2 billion EPCI contract for the offshore facilities at the Tangguh UCC project, securing a key execution partner for the mega-project. | Carbon Herald |

CCUS Investment Focus Narrows to the UK and Indonesia

The geographic landscape for new CCUS development is consolidating, with major investments flowing into a few key regions that offer strong government support and clear integration with existing energy infrastructure. Meanwhile, ambitions in markets with greater commercial or regulatory uncertainty are being curtailed.

- Between 2021 and 2024, CCUS ambitions were geographically widespread, with major players like BP actively pursuing projects and partnerships in the United States (Texas and Indiana), the UK (Teesside), Indonesia (Tangguh), and even exploring hubs in China.

- The period from 2025 to today reveals a sharp geographic contraction. Firm financial commitments are now concentrated in Indonesia, where the Tangguh UCC project is integrated with LNG export operations, and the UK, where the Northern Endurance Partnership is backed by an approximately £8 billion financing package and strong government support.

- The United States has seen a notable retreat from certain players. BP‘s decision to suspend its Indiana CCS project, despite the project previously being selected for US Department of Energy Carbon SAFE funding, signals a cooling of interest in the US Midwest hub.

- While exploratory discussions continue in other promising markets like India, the lack of firm investment decisions suggests that near-term CCUS growth will be driven by a small number of core hubs that provide clear economic and regulatory advantages, rather than a globally dispersed build-out.

Commercial Viability, Not Technology, Now Dictates CCUS Project Survival

The primary filter for new CCUS projects has shifted from technological readiness to commercial viability. Companies are now prioritizing mature, proven applications that decarbonize existing revenue streams, while shelving more complex projects like blue hydrogen that depend on the creation of new, uncertain markets.

- The 2021-2024 period saw significant industry focus on developing large-scale blue hydrogen facilities, such as H 2 Teesside in the UK and a similar project in Indiana. These projects relied on proven capture technologies but required the simultaneous development of a robust hydrogen offtake market.

- The cancellation of these exact projects in 2025 indicates that the market and infrastructure risks associated with building a new hydrogen value chain are currently too high for private investment alone, even when the underlying carbon capture technology is mature.

- In contrast, the projects that received final investment decisions, such as Tangguh UCC and the Net Zero Teesside power plant, are based on well-understood commercial models. Tangguh uses CO₂ for enhanced gas recovery, and Teesside applies post-combustion capture to a gas-fired power plant with a government-backed revenue model.

- This pattern confirms a clear market preference for CCUS applications that protect and optimize existing, profitable assets rather than those that require building entirely new, and speculative, low-carbon commodity markets from scratch.

SWOT Analysis: Strategic Pivot Sharpens Focus but Increases Transition Risk

The strategic shift in 2024-2025 toward a more focused, financially-driven CCUS portfolio has improved capital discipline for companies like BP. However, it has also exposed them to the risk of falling behind in emerging low-carbon markets and increased criticism for slowing their overall energy transition.

Chart Links Decarbonization Goals to Revenue

This chart connects decarbonization goals to future revenue, illustrating the opportunities and threats at the heart of the SWOT analysis discussed in the section.

(Source: MarketsandMarkets)

- This SWOT analysis captures the trade-offs inherent in this strategic pivot, contrasting the opportunities and threats of the earlier, broader approach with the realities of the current, more consolidated strategy.

Table: SWOT Analysis for a High-Grading CCUS Strategy

| SWOT Category | 2021 – 2023 Approach | 2024 – 2025 Approach | What Changed / Resolved / Validated |

|---|---|---|---|

| Strength | Broad portfolio of low-carbon options across hydrogen, renewables, and CCS, signaling strategic intent. | Improved capital discipline and focus on projects with clear, near-term returns integrated with core business. | The strategy shifted from diversification to financial consolidation, prioritizing profitability over a wide transition footprint. |

| Weakness | High capital expenditure on multiple speculative projects with uncertain timelines and commercial viability. | Reduced presence in the emerging clean hydrogen economy; reputational risk from scaling back green targets. | The company traded project execution risk across many ventures for the strategic risk of missing future growth in markets like hydrogen. |

| Opportunity | Potential to lead the energy transition across multiple technology fronts and geographies. | Opportunity to dominate a few, highly profitable CCUS hubs (e.g., Tangguh, NEP) and prove a replicable, asset-integrated model. | The scope of ambition narrowed from broad market leadership to demonstrating niche dominance in select, de-risked value chains. |

| Threat | Regulatory and technology risk spread across a wide, complex, and capital-intensive project portfolio. | Risk of being outpaced by competitors with more aggressive transition strategies; increased investor scrutiny over fossil fuel dependency. | The primary threat shifted from the failure of individual projects to the risk of the entire corporate strategy becoming obsolete in a rapidly accelerating transition. |

Scenario Modeling: Watch for Execution on Sanctioned Mega-Hubs

The critical path for large-scale CCUS deployment now depends entirely on the successful execution of the few sanctioned mega-hubs. If these core projects falter, it would invalidate the industry’s “high-grading” strategy and could stall institutional investment in CCUS for years.

- If flagship projects like Tangguh UCC and the Northern Endurance Partnership successfully begin operations on their planned 2026–2028 timelines and meet financial targets, it will validate the model of using CCUS to decarbonize profitable fossil fuel assets and encourage replication.

- Conversely, monitor for any further project “high-grading” or cancellations. BP‘s revised corporate target of just five to seven hydrogen and CCS projects by 2030 suggests that its remaining un-sanctioned portfolio is still under intense financial scrutiny.

- The most important signals to watch are physical progress on the ground. The start of drilling activities for the NEP in Q 3 2026 and the achievement of major construction milestones at Tangguh will be the definitive indicators of momentum.

- The trajectory gaining steam is a bifurcated market. A few large, integrated, and economically-driven CCUS hubs will advance, while a wider array of ambitious decarbonization projects will likely stall without direct government mandates and offtake guarantees.

Frequently Asked Questions

Why are major energy companies cancelling so many carbon capture projects?

Companies are cancelling projects as part of a strategic pivot called “high-grading.” They are shifting from a broad portfolio of speculative ventures to focusing only on projects with clear, near-term economic returns that are integrated with their core, profitable assets like oil and gas operations. Projects without guaranteed revenue or that rely on developing new markets, like blue hydrogen, are being cut in favor of more financially disciplined investments.

If projects are being cancelled, does this mean CCUS is failing?

Not necessarily. The strategy is consolidating, not collapsing. While speculative projects are being shelved, large-scale, de-risked hubs are moving forward with significant investment. Projects like the $7 billion Tangguh UCC in Indonesia, which uses CO₂ for enhanced gas recovery, and the Northern Endurance Partnership in the UK, which has strong government backing, are proceeding. This signals a shift toward fewer, but more commercially viable, mega-projects.

What does this trend mean for the future of blue hydrogen?

The outlook for large-scale blue hydrogen has become more challenging. Major blue hydrogen projects, like H2 Teesside in the UK and the Indiana CCS project, were cancelled in 2025. The article suggests this is because they depend on the creation of new, uncertain markets and offtake agreements for the hydrogen. The market and infrastructure risks are currently seen as too high for private investment without stronger government mandates or guarantees.

Where in the world are the new CCUS investments being concentrated?

New CCUS investments are now heavily concentrated in a few key regions that offer strong government support and clear integration with existing energy infrastructure. The article specifically identifies the UK, with the Northern Endurance Partnership, and Indonesia, with the Tangguh UCC project, as the primary hubs receiving firm financial commitments. In contrast, ambitions in other areas, such as the US Midwest, have been scaled back.

What is the most important factor for a CCUS project’s survival in 2026?

Commercial viability has become the most important factor, overtaking technological readiness. A project’s survival now depends on its ability to fit into a well-understood commercial model that protects or enhances existing revenue streams. Projects that decarbonize profitable assets, like using CO₂ for enhanced gas recovery (Tangguh) or capturing emissions from a gas power plant with a government-backed contract (Net Zero Teesside), are the ones moving forward.