Shell’s CCUS Strategy 2025: From Pilots to Profits with Major Investments & DAC Bets

Shell’s Commercial-Scale CCUS Projects Signal a Major Strategic Shift in 2025

In 2025, Shell transitioned its Carbon Capture, Utilization, and Storage (CCUS) strategy from exploratory agreements and operating controversial legacy projects to executing major commercial-scale Final Investment Decisions (FIDs), signaling a clear intent to build a new service-based business line.

- Between 2021 and 2024, Shell‘s activities were characterized by foundational Memorandums of Understanding (Mo Us) with partners like Petronas and ONGC and the continued operation of its Quest project, which faced scrutiny over its lifecycle emissions and reliance on over $654 million in government subsidies.

- The year 2025 marked a definitive shift with the FID for the Polaris CCS project in Canada, which will capture 650, 000 tonnes of CO₂ annually from Shell‘s Scotford refinery, and a $714 million joint investment to expand the Northern Lights project.

- This move from internal asset decarbonization to a commercial service model was validated in August 2025 when the Northern Lights project began injecting third-party CO₂ and secured a 15-year offtake agreement with Stockholm Exergi for 900, 000 tonnes per year.

- Shell further diversified its applications in 2025 by investing in emerging Direct Air Capture (DAC) technologies, backing startups Avnos and Rep Air Carbon to develop the planned Pelican DAC hub in Louisiana and de-risk next-generation carbon removal.

Shell’s 2025 Investment Data Reveals Targeted, Large-Scale Capital Deployment

Shell‘s 2025 CCUS investments demonstrate a strategic escalation from the broad $10-$15 billion low-carbon budget of 2023-2025 to targeted, multi-hundred-million-dollar capital deployments in commercial-scale infrastructure and venture-stage technologies.

- The most significant capital commitment in 2025 was the $714 million joint investment with Equinor and Total Energies to fund the Phase 2 expansion of the Northern Lights carbon transport and storage project, increasing its capacity to 5 million tonnes per year.

- In December 2025, Shell took an FID on the Polaris CCS Project at its Scotford complex in Canada, a direct investment to decarbonize its own refinery and chemical operations while anchoring the new Atlas Carbon Storage Hub.

- Beyond large infrastructure, Shell made strategic venture investments to secure future technology options, committing up to $17 million (jointly with Mitsubishi) in DAC startup Avnos and up to $3 million in Rep Air Carbon.

Table: Shell’s Key CCUS Investments in 2025

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Polaris CCS Project | December 2025 | Final Investment Decision (FID) for a project to capture 650, 000 tonnes/year of CO₂ from Shell‘s Scotford refinery, directly reducing Scope 1 emissions. | Shell Canada announces FID for carbon capture projects |

| Avnos (with Mitsubishi) | November 2025 | Investment of up to $17 million to fund the first commercial-scale plant for a hybrid DAC technology that co-captures CO₂ and water. | Shell, Mitsubishi invest $17 M in hybrid direct air capture … |

| Northern Lights Expansion (with Equinor, Total Energies) | March 2025 | Joint investment of $714 million to expand the project’s annual CO₂ injection capacity from 1.5 million to 5 million tonnes, enabling a commercial service model. | Shell, Equinor, Total Energies to invest $714 million in … |

| Rep Air Carbon (with Mitsubishi) | January 2025 | Provided up to $3 million in development funding to accelerate the commercialization of an electrochemical DAC technology for the Pelican DAC hub project. | Shell, Rep Air & Mitsubishi Drive Carbon Capture Innovation |

Shell’s 2025 Partnership Strategy Focuses on Commercial Hubs and Technology Alliances

In 2025, Shell solidified its CCUS ecosystem by moving from the exploratory joint studies of 2021-2024 to forming binding alliances and joint ventures focused on scalable technology deployment and the development of commercial storage hubs.

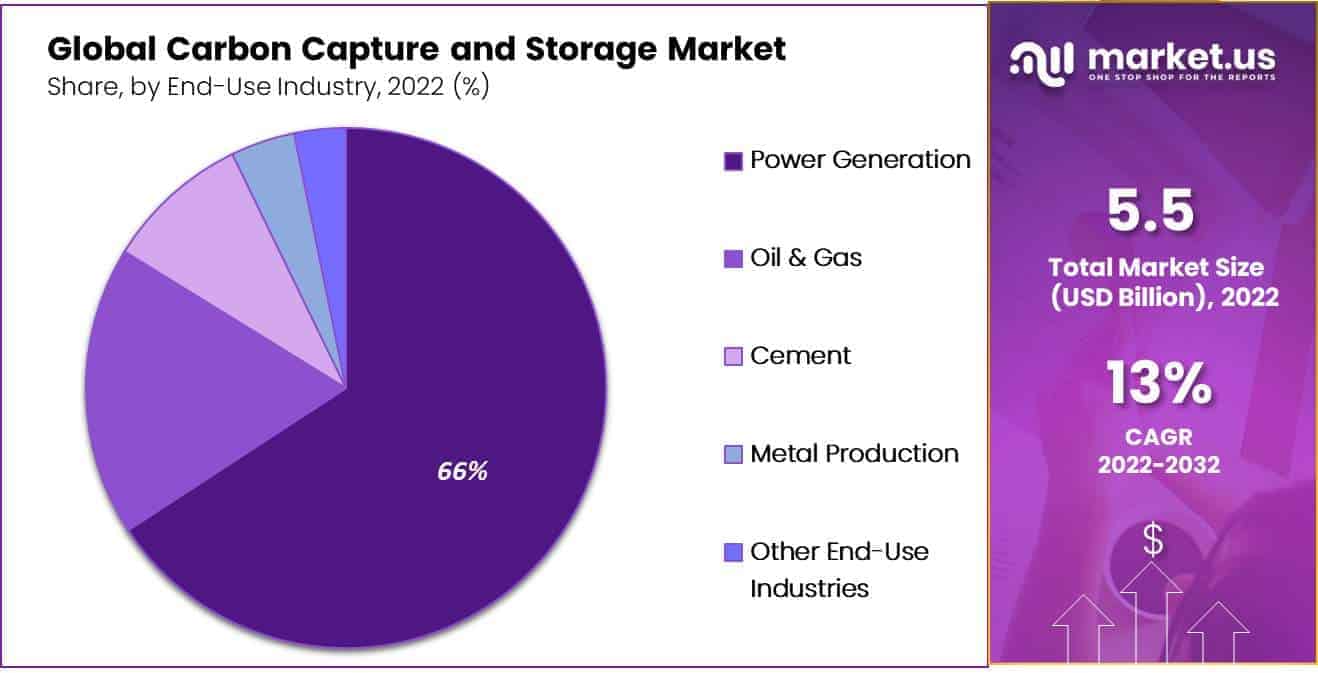

Oil & Gas Dominates CCUS End-Use Market

The oil and gas sector represents the largest end-use segment for carbon capture applications, highlighting the key industrial client base for strategic alliances. Power generation and other industrial sectors follow as significant markets.

(Source: Market.us)

- A pivotal change in 2025 was the formation of an exclusive global alliance with Technip Energies to accelerate delivery of Shell‘s proprietary CANSOLV® CO₂ Capture System, creating a standardized go-to-market solution for industrial clients.

- To support its Canadian ambitions, Shell created a 50/50 joint venture with ATCO En Power in December 2025 to build the Atlas Carbon Storage Hub, establishing a commercial infrastructure asset designed to serve its Polaris project and third-party emitters.

- The long-standing joint venture with Equinor and Total Energies for the Northern Lights project fully matured in 2025, becoming an operational, cross-border CO₂ storage service for Europe following its first injections in August.

- Shell expanded its network into the emerging DAC sector through technology-focused collaborations, partnering with Rep Air Carbon and Mitsubishi to develop the large-scale Pelican DAC Hub in Louisiana.

Table: Shell’s Key CCUS Partnerships in 2025

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| ATCO En Power | December 2025 | A 50/50 joint venture to develop the Atlas Carbon Storage Hub in Alberta, providing permanent sequestration for the Polaris project and third parties. | Shell Canada announces FID for carbon capture projects |

| Petroleum Development Oman (PDO) | October 2025 | Collaboration to jointly study and identify CCUS opportunities in Oman, exploring a new geographic market for future development. | Shell and PDO team up for CCUS projects in Oman |

| Technip Energies | July 2025 | Exclusive global alliance to combine Shell‘s CANSOLV® technology with Technip‘s project delivery expertise, creating a scalable, end-to-end solution. | Technip Energies & Shell Global Alliance for Carbon Capture |

| MITSUI & CO. | June 2025 | Joint research to develop a CCUS value chain business in the Asia-Pacific region, focusing on cross-border CO₂ transport and storage. | What is Carbon Capture, Utilization & Storage (CCUS)? … |

| Equinor, Total Energies | March 2025 | As part of the Northern Lights JV, partners committed $714 M for expansion and signed a 15-year offtake deal with Stockholm Exergi. | Shell, Equinor, Total Energies to invest $714 million in … |

Shell’s CCUS Geographic Focus Broadens from Canada to Europe and the US Gulf Coast

In 2025, Shell‘s CCUS geographic focus expanded from its established operational base in Canada to executing major European hub operations and initiating new projects in the U.S. Gulf Coast and the Asia-Pacific region.

North America Leads Global Carbon Capture Market

North America holds the largest share of the global carbon capture and storage market, followed by Europe and the Asia-Pacific. This illustrates the key geographic arenas where companies are expanding their CCUS operations.

(Source: The Business Research Company)

- From 2021 to 2024, Canada was the primary center of activity, dominated by the operational Quest facility and early-stage planning for the Polaris project in Alberta, which served as a key learning ground for Shell.

- Europe became a major commercial hub for Shell in 2025, as the Northern Lights project in Norway became fully operational, establishing a CO₂ transport-and-storage service for industrial emitters across the continent.

- Shell deepened its presence in North America in 2025 by taking an FID on the Polaris project in Canada and establishing a new beachhead in the U.S. with the planned Pelican DAC Hub in Louisiana.

- The company continued to lay the groundwork for future growth in new regions through 2025 collaborations in the Asia-Pacific (with MITSUI & CO. and Exxon Mobil in Singapore) and the Middle East (with PDO in Oman).

Shell’s Technology Strategy: Commercializing Mature Systems While Seeding DAC Innovation

In 2025, Shell advanced a dual-track technology strategy, aggressively commercializing its mature point-source capture systems through strategic alliances while de-risking next-generation Direct Air Capture (DAC) via targeted venture investments.

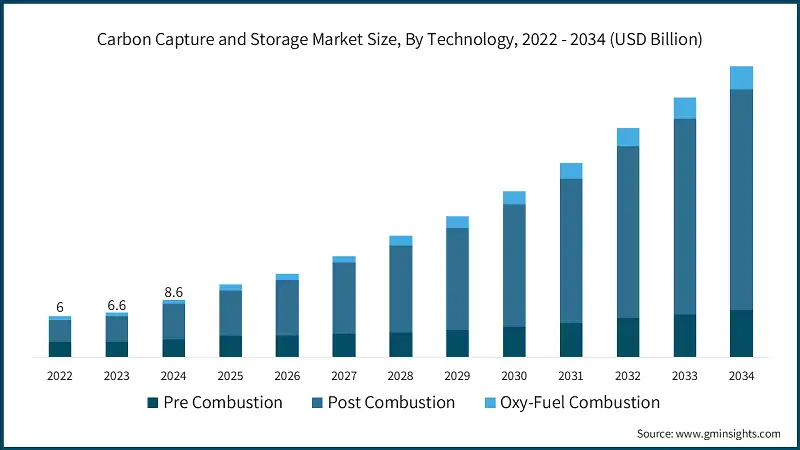

CCUS Market Forecast by Capture Technology Type

Post-combustion capture technology is forecast to lead the CCUS market, underscoring the industry’s focus on commercializing mature systems for existing facilities. Pre-combustion and oxy-fuel combustion also represent key technology segments for investment.

(Source: Global Market Insights)

- In the 2021-2024 period, Shell focused on operating existing amine-based technology at the Quest project and licensing its CANSOLV® system, which lacked a unified, large-scale commercial deployment model.

- Shell elevated its proprietary CANSOLV® system to a scalable commercial offering in 2025 through its global alliance with Technip Energies, validating its readiness for deployment in large, hard-to-abate industrial projects.

- In parallel, Shell diversified into earlier-stage technologies by investing in DAC startups, backing Avnos‘s novel hybrid water-and-CO₂ capture system and Rep Air Carbon’s electrochemical process to build a portfolio of future carbon removal options.

- The company also revealed its own in-house development of a solid sorbent-based DAC technology in October 2025, indicating a comprehensive approach to securing a long-term position in both point-source capture and atmospheric carbon removal.

Shell’s SWOT Analysis: Leveraging Strengths Amid Policy Dependence and Performance Scrutiny

Shell‘s 2025 strategy leverages its technological strengths and operational experience to capture market opportunities but faces threats from policy dependence and public scrutiny over the real-world performance and economics of its projects.

- Strengths: Shell possesses proprietary capture technology and significant operational experience, which it is now effectively monetizing through structured alliances and joint ventures.

- Weaknesses: The high cost and energy intensity of CCUS remain a core challenge, making projects heavily reliant on subsidies and risking public backlash over their net climate benefit.

- Opportunities: A rapidly growing global CCUS market and robust government incentives provide a clear path for Shell to build a profitable, low-carbon service business.

- Threats: The economic viability of Shell‘s entire CCUS portfolio is exposed to shifts in government policy and carbon pricing, while underperformance could inflict significant reputational damage.

Table: SWOT Analysis for Shell’s CCUS Strategy

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Possessed proprietary technology (CANSOLV®) and operational experience from projects like Quest. | Actively commercializing CANSOLV® through a global alliance with Technip Energies and leveraging operational experience to lead JVs. | Shell validated its ability to shift from being a technology holder to a solutions provider, creating a scalable go-to-market strategy. |

| Weaknesses | High cost of CCUS projects and heavy reliance on public subsidies (e.g., Quest). Projects faced criticism for high lifecycle emissions. | Costs remain high, but large co-investments ($714 M for Northern Lights) and reliance on policy (Canada’s tax credits for Polaris) are now embedded in the strategy. | The weakness of high costs was acknowledged and addressed through a capital-sharing partnership model, de-risking individual project exposure. |

| Opportunities | A nascent but growing market for CCUS, supported by early-stage policy frameworks. | Captured first-mover advantage with the operational Northern Lights hub, signing a 15-year commercial offtake agreement with Stockholm Exergi. | Shell moved from acknowledging the market opportunity to actively capturing it by securing long-term revenue streams for its “decarbonization-as-a-service” model. |

| Threats | Risk of policy changes, negative public perception, and projects underperforming against stated goals (e.g., Gorgon). | Dependence on policy frameworks like the US 45 Q tax credit and Canadian carbon pricing remains a critical risk for project economics. Scrutiny continues with the Pathways Alliance project cost. | The threat of policy dependence was validated as a core business reality, with FIDs and project viability explicitly linked to government incentives. |

Forward-Looking Insights: Execution and DAC Scalability are Shell’s Key Tests for 2026

The critical factor for Shell‘s CCUS business in the coming year is its ability to successfully execute on its 2025 Final Investment Decisions and convert its Direct Air Capture venture investments into scalable, cost-effective pilot projects.

- The market will closely watch the construction of the Polaris project in Canada and the operational ramp-up of the newly expanded Northern Lights facility, as these are primary tests of Shell‘s ability to deliver large-scale infrastructure on time and on budget.

- The progress of the Pelican DAC Hub in Louisiana and the performance of the first commercial-scale plant from portfolio company Avnos will determine if DAC becomes a meaningful pillar of Shell‘s carbon removal strategy.

- Future capital allocation will signal strategic priorities. How Shell divides its low-carbon spending between decarbonizing its own assets versus building third-party CO₂ storage services will indicate its long-term vision.

- The profitability of these ventures remains highly sensitive to regulatory frameworks like the U.S. 45 Q tax credit, which offers up to $180 per ton for DAC. Any shifts in these supportive policies will directly impact future investment decisions and project viability.

Frequently Asked Questions

What was the main change in Shell’s CCUS strategy in 2025?

In 2025, Shell’s strategy shifted from exploratory agreements and managing legacy projects to executing major commercial-scale Final Investment Decisions (FIDs). This marked a significant transition from using CCUS primarily for its own assets to building a new service-based business line offering carbon capture, transport, and storage to third-party industrial customers.

What were Shell’s most significant CCUS investments in 2025?

The most significant investments in 2025 were a $714 million joint investment with Equinor and TotalEnergies to expand the Northern Lights project in Europe, and the Final Investment Decision (FID) on the Polaris CCS project in Canada. Shell also made venture investments of up to $17 million in DAC startup Avnos and up to $3 million in Rep Air Carbon.

How is Shell turning CCUS into a profitable business?

Shell is developing a “decarbonization-as-a-service” model by building large-scale carbon storage hubs, like Northern Lights in Europe and the Atlas Carbon Storage Hub in Canada. It then charges third-party industrial emitters for transporting and permanently storing their CO₂. A key example is the 15-year offtake agreement with Stockholm Exergi to store 900,000 tonnes of CO₂ per year at the Northern Lights facility.

What is Direct Air Capture (DAC) and why is Shell investing in it?

Direct Air Capture (DAC) is a technology designed to remove CO₂ directly from the atmosphere, rather than from an industrial source. In 2025, Shell invested in DAC startups like Avnos and Rep Air Carbon to de-risk next-generation carbon removal technologies and build a portfolio of future options for its planned Pelican DAC hub in Louisiana, diversifying beyond traditional point-source capture.

What are the biggest challenges or risks facing Shell’s CCUS strategy?

The biggest challenges are the high costs and energy intensity of CCUS projects, which makes the business model heavily dependent on government subsidies and carbon pricing (like the US 45Q tax credit). This economic viability is threatened by potential shifts in government policy. The company also faces reputational risk from public scrutiny over the real-world performance and net climate benefit of its projects.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.