Data Center Power Crisis 2026: Why AI Infrastructure Investment Now Requires Energy Integration

Power Scarcity Drives AI Data Center Vertical Integration in 2026

The primary constraint on the growth of artificial intelligence is no longer silicon but the availability of reliable power, forcing infrastructure investors to abandon standalone data center acquisitions in favor of a vertically integrated strategy that combines digital assets with power generation. Before 2024, investors treated data centers as specialized real estate, focusing on fiber connectivity and location. The strategy in 2025 and beyond, exemplified by Global Infrastructure Partners (GIP), recognizes that the multi-gigawatt power demands of AI render this model obsolete. Securing the energy supply is now as critical as securing the physical data center, leading to a fundamental realignment of investment strategy across the sector.

- In 2022, GIP and KKR executed a traditional, large-scale data center acquisition by purchasing Cyrus One for $15 billion, a move focused on capturing a portfolio of existing digital real estate.

- This strategy shifted dramatically by May 2024, when GIP led a $6.2 billion deal to acquire Allete, a regulated utility company. This marked a deliberate move to internalize power generation capabilities, directly addressing the energy bottleneck for its data center assets.

- The formation of the AI Infrastructure Partnership (AIP) in 2025 codified this new model. The consortium, led by GIP and backed by Black Rock, Microsoft, and MGX, was created with the dual mandate to invest in both data centers and their supporting power infrastructure, a clear departure from the siloed investment approaches of prior years.

- The partnership’s $40 billion acquisition of Aligned Data Centers in October 2025 was not just a real estate play; it was the acquisition of a 5 GW power footprint to be fed by GIP’s growing energy portfolio, solidifying the integration of data and power as the new industry standard.

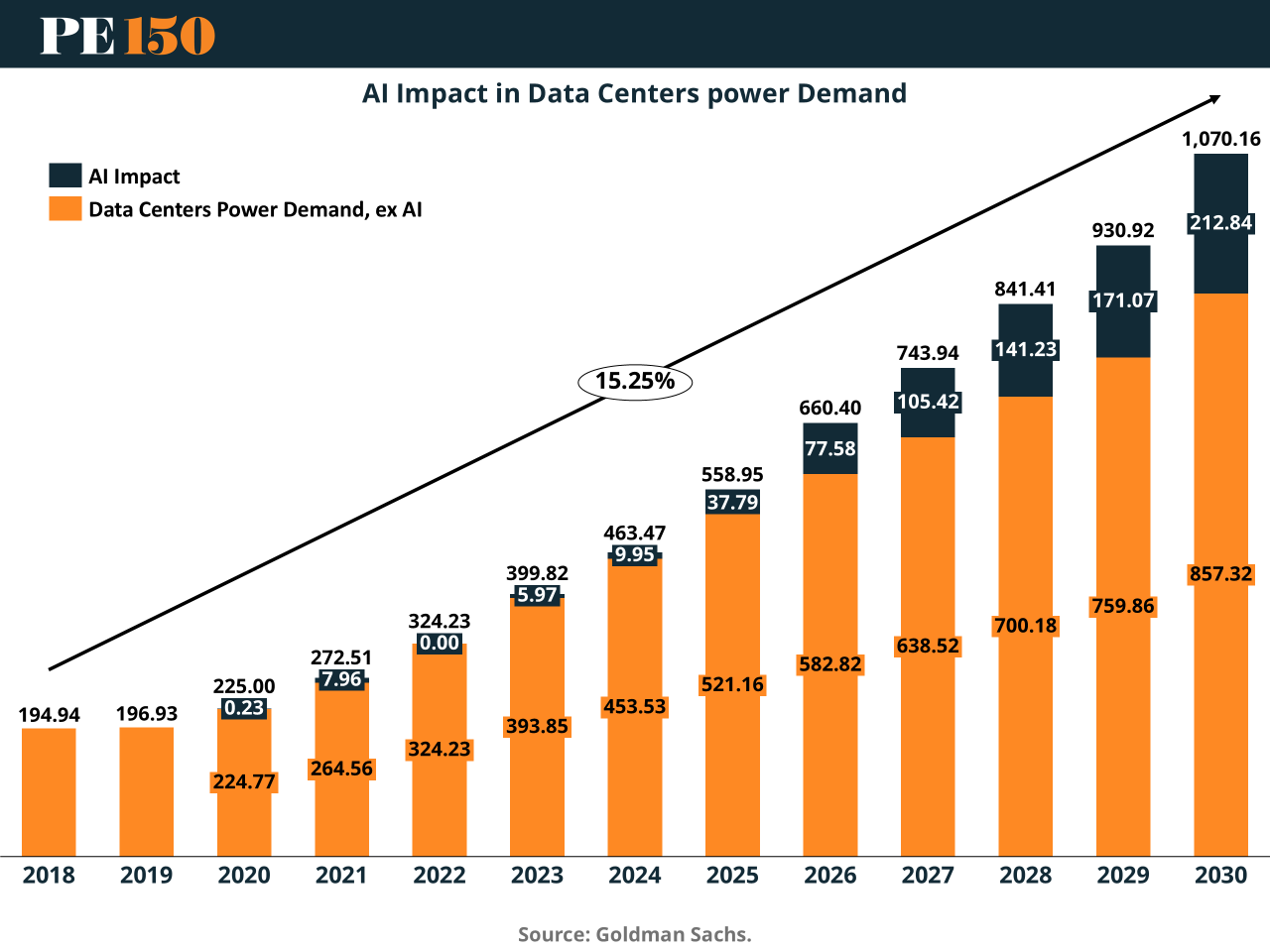

AI Power Demand Driving Exponential Growth

This section identifies power scarcity as the primary constraint on AI growth. This chart directly illustrates the problem by showing that demand from AI is the specific driver of exponential growth in data center power consumption.

(Source: PE 150)

The AI Infrastructure Market is Poised for a $1 Billion Power-and-Data Stack Boom in 2026

Capital deployment in the digital infrastructure sector has pivoted decisively towards large-scale, integrated investments that bundle data center capacity with power generation, reflecting the new economic reality of the AI era. The unprecedented valuations, such as the ~40 x revenue multiple for Aligned Data Centers, are justified by investors not as a premium for real estate but for the access to scarce, large-scale power capacity. This trend is creating a new class of investment where multi-billion-dollar deals are structured to solve the energy problem first, with data center construction as the downstream objective.

Data Center CAPEX to Hit $6.7T by 2030

The section describes a new, multi-billion dollar ‘power-and-data stack’. This chart perfectly quantifies the scale of this investment and includes a $1.3T ‘Energizers’ segment, directly reflecting the integration of power generation.

(Source: AI-CIO.com)

- The scale of this new investment stack is defined by the AI Infrastructure Partnership’s goal to raise $30 billion in equity to fund up to $100 billion in total investments, explicitly targeting both data centers and power infrastructure.

- Hyperscalers are pursuing parallel strategies, such as Meta Platforms’ $27 billion financing arrangement with Blue Owl in October 2025, which is dedicated to funding the construction of its own proprietary AI data centers and the immense power required to run them.

- Even before its landmark 2025 moves, GIP demonstrated this foresight with its $6.2 billion acquisition of utility Allete, a direct investment into the power supply chain itself.

- Competitor activity confirms this trend, with Brookfield and Bloom Energy forming a $5 billion partnership in October 2025 to deploy dedicated onsite power solutions, showing that the entire ecosystem is now focused on solving the AI data center energy challenge outside of traditional grid reliance.

Table: Key Data Center and Energy Integration Investments (2024-2025)

| Investor(s) / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| GIP / Black Rock / ACS | Nov 2025 | Formation of a €23 billion ($26.8 billion) joint venture to develop a new data center business, expanding GIP’s digital infrastructure footprint in partnership with a construction major. | Capacity Magazine |

| Meta Platforms / Blue Owl | Oct 2025 | $27 billion financing deal for Meta to fund the construction of its own AI data centers, showcasing the hyperscaler self-build and self-powering strategy. | Global Data Center Hub |

| GIP / MGX / AIP Consortium | Oct 2025 | $40 billion acquisition of Aligned Data Centers to secure a 5 GW platform of 78 facilities, providing immediate scale for the integrated data-and-power strategy. | Bloomberg |

| GIP / CPP Investment Board | May 2024 | $6.2 billion acquisition of utility company Allete, a strategic move to secure power generation assets to supply future and existing data center portfolios. | Utility Dive |

Strategic Alliances Will Define the Future of Integrated AI Data Center Ecosystems in 2026

The nature of partnerships in the AI infrastructure space has transformed from simple landlord-tenant relationships into complex, multi-party consortia designed to de-risk development by aligning capital, technology, customers, and energy supply. The defining characteristic of these new alliances is the creation of a closed-loop ecosystem. By bringing the primary chip designer (Nvidia), cloud consumer (Microsoft), infrastructure operator (GIP), and deep-pocketed capital providers (MGX, Black Rock) into a single vehicle, the AI Infrastructure Partnership model mitigates demand risk and ensures the massive capital outlay is directed at pre-sold capacity.

- The AI Infrastructure Partnership (AIP), formed in 2025 by GIP, MGX, Nvidia, Microsoft, x AI, and Temasek, is the primary example of this new model. Its purpose is to acquire and develop assets like Aligned Data Centers with built-in demand from its own partners.

- This contrasts with earlier, less integrated partnerships like GIP and KKR’s co-ownership of Cyrus One. While a major digital infrastructure play, it lacked the embedded customer and power-generation components that define the 2025 strategy.

- Competitors are replicating this integrated approach. In October 2024, KKR and Energy Capital Partners announced a $50 billion strategic collaboration explicitly aimed at investing in the transition of the power grid and the build-out of digital infrastructure, recognizing the two are inseparable.

- The $5 billion partnership between Brookfield and Bloom Energy in October 2025 to deploy onsite power generation for data centers is another signal of this trend, creating alliances that directly bypass traditional grid constraints by co-locating power and compute.

Global AI Infrastructure Hotspots Emerge as the World Races for Power and Land in 2026

Investment in AI data centers is geographically concentrating in regions that offer the critical combination of available land, supportive energy policy, and access to large-scale power, with the United States emerging as the principal battleground. The shift from 2021-2024, which saw more geographically dispersed development, to the current period is marked by a focus on securing multi-gigawatt campuses in specific U.S. states. This concentration is driven by projections that U.S. data center power demand could reach 390 TWh, forcing developers to seek locations where energy development is feasible and politically supported.

US Data Center Power Demand to Surge by 2030

The section identifies the United States as the main ‘battleground’ for AI infrastructure due to power needs. This chart provides the specific forecast for the surge in US data center power demand, validating the section’s geographic focus.

(Source: AI-CIO.com)

- The primary focus of GIP’s AI Infrastructure Partnership and its acquisition of Aligned Data Centers is the U.S. market, targeting states with favorable regulatory environments for both data centers and new power generation projects.

- The U.S. government has recognized this geographic constraint, with the White House issuing an executive order in July 2025 to accelerate federal permitting for data center infrastructure and high-voltage transmission lines, a policy designed to keep AI development centered in the U.S.

- While the U.S. is the epicenter, the race for AI infrastructure is global. An agreement for a 5 GW data center campus in Abu Dhabi (Stargate UAE) and the Thai government’s approval of $3.1 billion in new data center projects in early 2026 indicate that other nations are aggressively competing to build their own AI hubs. This may present new challenges related to Data Center Risk 2026: War Reshapes ME Investment.

AI Infrastructure Maturity Transitions from Real Estate Play to Utility-Scale Energy Challenge in 2026

The definition of a commercially mature data center asset has fundamentally evolved; it is no longer sufficient for an asset to be a powered shell with fiber access, but must now come with a clear, securable path to obtaining hundreds of megawatts or even gigawatts of power. Between 2021 and 2024, maturity was defined by operational track record and a roster of tenants. Today, maturity is measured by the asset’s access to power and its ability to support the extreme rack densities and cooling requirements of AI hardware. This shift makes energy expertise a core competency for data center investors, blurring the lines between digital infrastructure and power generation.

Power Demand Pipeline Skyrockets in 2024

This section explains the evolution from a ‘real estate play’ to a ‘utility-scale energy challenge’. This chart, showing the ‘Large Load Pipeline’ more than doubling, directly quantifies this shift to a massive, utility-level problem.

(Source: Techno-Statecraft)

- The progression is visible in GIP’s own portfolio. The 2022 acquisition of Cyrus One represented an investment in a mature, traditional data center operator. By 2025, the acquisition of Aligned Data Centers was valued based on its massive 5 GW power capacity, a metric that was secondary just a few years prior.

- The technological challenge is now about power delivery and cooling at an unprecedented scale. This is forcing operators and investors to explore alternative energy solutions, including the potential for using small modular reactors for Alibaba Nuclear Power: Fueling AI Data Centers in 2026 or a broader Data Center Energy 2026: Equinix’s Nuclear Pivot.

- Hyperscaler projects like Meta’s multi-gigawatt AI data centers, Prometheus and Hyperion, validate this new definition of maturity. These are not buildings but utility-scale energy projects, establishing a new technical and financial baseline for what is considered a viable AI-ready site.

- The financing reflects this shift. In Q 3 2025 alone, project finance banks committed $15 billion to greenfield hyperscale projects, with funding viability increasingly tied to the project’s power-sourcing agreements and energy infrastructure plan.

SWOT Analysis: The Integrated Data Center and Power Strategy

The strategic pivot to an integrated data center and power generation model offers a powerful competitive advantage by solving AI’s biggest bottleneck, but it also introduces significant new layers of capital intensity and operational risk. This SWOT analysis contrasts the market dynamics before and after the AI-driven power crisis became the central strategic driver.

Table: SWOT Analysis for Integrated AI Infrastructure Strategy

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Expertise in acquiring and operating standalone digital infrastructure assets. Strong track record in traditional infrastructure private equity. | Massive capital backing (Black Rock acquisition, $100 B AIP fund). Vertically integrated model controls both data centers (Aligned, Cyrus One) and power (Allete). Pre-sold demand from partners (Microsoft, x AI). | The model shifted from being a real estate landlord to an integrated utility provider for the AI economy, creating a significant competitive moat. |

| Weaknesses | Dependence on third-party power markets and grid stability. Exposure to volatile energy prices as a major consumer. | Extreme capital intensity required for dual investments in power and data. Increased operational complexity of managing both utility and tech assets. Long lead times for new power plant construction. | The strategy internalizes energy risk but in doing so takes on the financial and operational burden of becoming a power generator, a far more complex business. |

| Opportunities | Benefit from rising demand for colocation and cloud services. Consolidate a fragmented data center market. | Achieve market dominance by controlling the physical layer of the AI value chain. Offer a unique, de-risked solution to hyperscalers. Capitalize on the structural scarcity of AI-ready, gigawatt-scale sites. | The core opportunity is no longer just renting space but solving the fundamental power constraint of the entire AI industry, enabling significant value capture. |

| Threats | Competition from other data center operators and private equity firms. Rising real estate and construction costs. | Regulatory and permitting delays for new power generation and transmission lines. Grid instability threatening uptime. A potential slowdown in AI compute demand. Competition from hyperscalers (e.g., Meta) building their own power. | The primary threats have shifted from real estate competition to systemic risks in the energy sector, including policy, regulation, and physical grid limitations. |

The Future of AI Infrastructure in 2026: Why the Energy Sector is the Next Frontier

The most critical strategic development for 2026 will be the execution of new power generation projects specifically to support AI data center expansion, as this is the long-pole in the tent for the entire investment thesis. While capital has been committed and data center operators have been acquired, the success of this strategy hinges entirely on the ability of firms like GIP to bring new, reliable power sources online at a pace that matches AI’s insatiable growth. The focus will shift from financial deal-making to engineering and construction.

Power Provider Cites Data Centers as Top Market

The section’s forward look states that the future of AI infrastructure is executing new power generation projects. This chart provides direct evidence, showing a power generation company identifying data centers as its largest market.

(Source: Arya’s Substack)

- If the Aligned acquisition closes successfully in H 1 2026, watch for immediate announcements of large-scale Power Purchase Agreements (PPAs) or direct investment in new solar, wind, or natural gas plants to service its 5 GW portfolio.

- The next major investment by the AI Infrastructure Partnership will be a key signal. Watch to see if it targets another data center operator or if it makes a direct, multi-billion-dollar investment into a power generation company or a portfolio of renewable energy projects.

- The effectiveness of government policy will be tested. Watch for the real-world impact of the July 2025 executive order on permitting. A failure to accelerate approvals for transmission lines and power plants could stall the entire private sector build-out. This represents a key area of Data Center Risk 2026: Surviving the US-Iran Conflict.

- The valuation premium for power access could increase. If power constraints worsen, future data center M&A will see an even greater “AI premium” for assets with secured, large-scale power contracts, validating GIP’s high-multiple acquisition of Aligned and driving further consolidation around energy-rich players like Digital Realty.