The 2026 Memory Crisis: How AI Is Triggering A Global Supply Chain Bottleneck

Industry Risk: AI Demand Creates a Structural Memory Shortage for 2026

A fundamental realignment of the semiconductor supply chain is underway, creating a structural shortage of memory chips for the consumer electronics market that will peak in 2026. Before 2025, the memory market followed predictable cyclical patterns of supply and demand. Now, the high-margin, price-inelastic demand for High-Bandwidth Memory (HBM) from the Artificial Intelligence (AI) sector has forced manufacturers to permanently deprioritize production of conventional DRAM and NAND flash used in smartphones and PCs, exposing the consumer market to severe price shocks and supply constraints.

- Between 2021 and 2024, memory chip supply adequately served both the data center and consumer electronics markets, with pricing subject to typical cyclical fluctuations. Starting in 2025, this balance disintegrated as AI-driven data centers began consuming a disproportionate share of output, with projections showing they will claim up to 70% of global memory production by 2026.

- This shift is driven by economics; AI memory like HBM generates 3 to 5 times the profit margin of standard RAM, incentivizing major producers like Samsung, SK Hynix, and Micron to reallocate fab capacity. Micron Technology has already sold out its entire HBM supply for 2026, confirming that the most profitable production lines are unavailable to the consumer sector.

- The consequences materialized in late 2025 and early 2026 with record price increases. Analysts forecast quarter-over-quarter price hikes of up to 60% for conventional DRAM and 38% for NAND Flash in Q 1 2026, a direct result of supply being diverted to the more lucrative AI market.

- This supply diversion represents a critical AI manufacturing constraint, where the needs of AI infrastructure now dictate component availability for the entire technology ecosystem, a stark departure from the consumer-led dynamics of the previous decade.

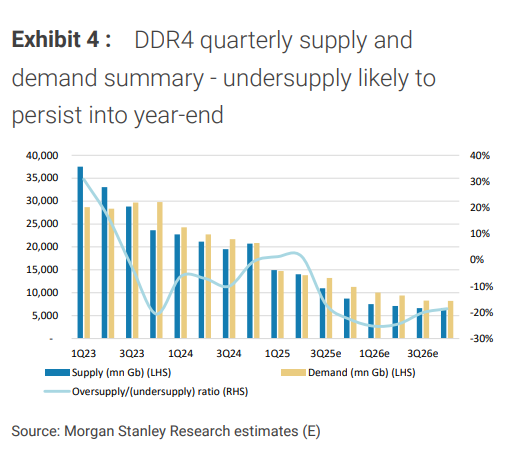

DDR4 Memory Undersupply Forecasted Through 2026

This chart perfectly visualizes the section’s main point: a structural shortage of conventional memory (DDR4) caused by the pivot to AI, with demand clearly outpacing supply through 2026.

(Source: EnkiAI)

Investment: Record Profits Confirm Memory Makers’ Pivot to AI

Financial results and investment patterns from 2025 to today confirm that capital is flowing decisively toward high-margin AI memory production, cementing the supply shortage for consumer-grade chips. While the 2021-2024 period saw balanced investments across different memory types, the AI boom has triggered a focused wave of capital expenditure aimed exclusively at HBM and the latest-generation server DRAM. This investment strategy prioritizes the high-spending data center market, leaving smartphone and PC manufacturers to compete for a shrinking pool of legacy components.

Memory Market Rebounds on AI Demand

This chart directly supports the section’s focus on record profits and financial results, showing massive revenue growth for memory suppliers explicitly driven by the AI boom.

(Source: EnkiAI)

- Major technology companies are fueling this trend with a projected $680 billion investment in AI infrastructure in 2026 alone, creating intense, sustained demand for high-performance memory. This massive capital injection into the AI power crisis ensures data centers can and will outbid consumer device makers for priority supply.

- The financial returns validate this strategic shift, with Samsung Electronics reporting a staggering 1, 458% year-over-year increase in operating profit in Q 2 2024, largely attributed to the high demand for its AI memory chips.

- Anticipating continued tightness, memory producers began signaling significant price hikes. In August 2024, SK Hynix notified customers of a planned 15-20% price increase for its DDR 5 DRAM, citing the need to reallocate production lines to HBM.

Table: Key Financial Signals in the Memory Market

| Company / Sector | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Big Tech Collective | 2026 (Projected) | Plan to invest $680 billion in AI infrastructure, creating massive and inelastic demand for high-performance memory chips like HBM. | Intellectia.AI |

| Samsung Electronics | Q 2 2024 | Reported a 1, 458% year-over-year increase in operating profit, driven primarily by soaring demand and pricing for its AI memory chips. | Forbes |

| SK Hynix | Q 3-Q 4 2024 | Announced a 15-20% price increase for DDR 5 DRAM to manage demand and prioritize the shift of production capacity toward more profitable HBM. | Tweak Town |

| Micron Technology | 2026 | The company’s complete supply of high-performance HBM chips is reportedly sold out for the entirety of 2026, indicating extreme supply tightness at the high end of the market. | Intellectia.AI |

Partnerships: Alliances Form to Secure On-Device AI Dominance

Strategic partnerships formed in 2025 and 2026 are focused on integrating advanced AI directly into smartphones, which further intensifies demand for high-capacity memory and exacerbates the supply crisis. Unlike earlier partnerships centered on software ecosystems, these new alliances are fundamentally about co-developing hardware and software to run powerful AI models on-device. This requires significantly more RAM per unit, directly competing with data centers for limited memory production.

- The collaboration between Samsung and Google to co-develop a new AI-native operating system for all future Galaxy products, announced in February 2026, is a primary example. This move establishes a new baseline for flagship devices that necessitates higher memory configurations to support persistent on-device AI functionalities.

- This trend creates a dual-demand shock: while data centers require vast quantities of HBM for training, the smartphone market now requires larger amounts of high-speed LPDDR RAM for inference. With manufacturers already prioritizing HBM, the supply of LPDDR for smartphones is consequently squeezed.

- Such partnerships signal that flagship smartphone vendors are committed to an AI-centric roadmap, even if it means accepting higher component costs. This willingness to pay a premium for memory to enable key features reinforces the market power of memory suppliers and solidifies higher prices across the board.

Geography: South Korea Becomes the Epicenter of the Global Memory Bottleneck

The global memory supply crisis is geographically concentrated in South Korea, home to the world’s leading memory manufacturers, Samsung and SK Hynix. While demand is global, driven heavily by U.S.-based technology giants like Google, Meta, and Microsoft, the production decisions made in South Korea are the primary determinant of global supply and pricing. This concentration of production capability for the most advanced memory chips has turned the region into the critical control point for the entire AI hardware ecosystem.

AI Demand Drives Gains for Memory Makers

This chart is the best fit as it shows the performance of specific manufacturers, including Samsung and SK Hynix, who are named in the section as the South Korean epicenter of the bottleneck.

(Source: EnkiAI)

- Between 2021 and 2024, South Korea’s role was that of a stable global supplier. From 2025 onward, its strategic pivot to prioritizing HBM production for AI data centers has made it the source of a global supply constraint for consumer electronics.

- The United States, as the primary consumer of AI chips for its hyperscale data centers, is the main driver of this production shift. The economic pressure exerted by U.S. tech companies’ procurement strategies directly impacts the availability of memory for other markets and device categories worldwide.

- Other manufacturing regions have been unable to scale up production of conventional memory to fill the gap, as building new semiconductor fabs requires years of lead time and immense capital investment. This leaves the consumer electronics industry with no immediate alternative to the constrained supply from South Korea.

Technology Maturity: HBM Reaches Full Commercial Scale, Displacing Conventional DRAM

The 2026 memory crisis is a direct result of High-Bandwidth Memory (HBM) achieving full technological and commercial maturity, establishing it as the new, high-margin anchor of the memory market. Before 2025, HBM was a niche, albeit growing, segment. Today, it is a mainstream, high-demand component whose production economics are forcing a systemic reallocation of manufacturing resources away from conventional memory like DDR 4 and LPDDR. The technology is no longer in a pilot or early adoption phase; its complete sell-out for 2026 at premium prices confirms it is a mature, commercially dominant product.

AI Chip Memory Demand Skyrockets

This chart directly illustrates the section’s theme of technology maturity by showing the exponential growth in memory required for AI chips, which is the force driving HBM to commercial scale.

(Source: Bloomberg.com)

- The performance leap offered by HBM is essential for large-scale AI, making it a non-negotiable component for companies like NVIDIA and their data center customers. An AI server requires, on average, six times more DRAM content than a standard server, with HBM being the most critical portion.

- In contrast, the technology for conventional DRAM is fully mature but now suffers from being a lower-margin product. As a result, capital and R&D are being diverted away from innovating or expanding capacity for these legacy chips, leading to the supply squeeze.

- The crisis is not due to a failure in memory technology but rather a market success. HBM’s value proposition is so compelling for the AI sector that it has created an irreversible economic incentive for manufacturers to abandon the lower end of the market, turning what was once a commodity into a hyperscale interconnects bottleneck.

Scenario Analysis: Market Bifurcation and the New Price Floor

If memory prices continue to climb by another 40-50% through the first half of 2026 as predicted, watch for mid-tier smartphone brands to announce significant changes to their product roadmaps, either delaying launches or releasing models with reduced memory specifications. The most probable scenario for 2026 is a sharp bifurcation of the smartphone market, establishing a new, higher price floor for consumer devices and delaying the widespread availability of advanced on-device AI.

Memory Crunch Wipes Out Smartphone Forecasts

This chart visualizes the scenario analysis by comparing previous and revised forecasts, showing how the memory shortage is directly causing a projected decline across the smartphone market.

(Source: EnkiAI)

- High-End Price Hikes: Flagship devices from Apple and Samsung will incorporate advanced AI but at a significant price premium. The bill-of-materials cost for DRAM in a low-end phone is projected to rise from 10% to 30%, a cost that will be passed directly to consumers, pushing the global smartphone Average Selling Price (ASP) to a record high of $523.

- Mid-Range “Spec Shrinkflation”: Manufacturers targeting the budget and mid-range segments will be forced into “spec shrinkflation, ” where new models may ship with less RAM than their predecessors to maintain target price points. This will hollow out the value proposition in the market’s most competitive segments.

- Historic Shipment Decline: The culmination of these pressures is a projected historic market contraction. Analyst firm IDC forecasts a 12.9% decline in global smartphone shipments for 2026, the sharpest drop on record, as manufacturers are unable to absorb the component costs and scale back production. This indicates the market has no near-term solution to the AI-driven memory shortage.

Frequently Asked Questions

Why is there a memory shortage predicted for 2026?

The shortage is caused by a massive shift in manufacturing priorities. The Artificial Intelligence (AI) sector’s demand for high-margin High-Bandwidth Memory (HBM) is so strong that manufacturers like Samsung, SK Hynix, and Micron are reallocating production away from conventional DRAM and NAND used in consumer products. Since HBM is 3 to 5 times more profitable, the consumer electronics market is being deprioritized, leading to a structural supply bottleneck.

How will this memory crisis affect me when buying new electronics?

You can expect higher prices and potentially lower-spec devices. Flagship smartphones and PCs will likely become more expensive as they absorb the rising cost of memory. Mid-range and budget devices may experience “spec shrinkflation,” where new models are released with less RAM than their predecessors to maintain price points. This could lead to a historic 12.9% decline in global smartphone shipments in 2026.

Which companies are profiting from this situation?

The primary beneficiaries are the major memory manufacturers. The text highlights that Samsung Electronics saw its operating profit increase by a staggering 1,458% year-over-year in Q2 2024 due to high demand for its AI memory. Similarly, SK Hynix has announced price hikes of 15-20% for its DRAM, and Micron Technology has reportedly sold out its entire HBM supply for 2026, locking in high-margin revenue.

What makes this shortage different from past, cyclical memory shortages?

Unlike previous shortages that were part of a predictable boom-and-bust cycle, this is a permanent, structural realignment of the market. The demand from the AI sector is price-inelastic and so large—projected to consume 70% of global memory production by 2026—that it has fundamentally changed production economics. AI infrastructure needs now dictate component availability for the entire tech ecosystem, a stark departure from the previously consumer-led market.

Why can’t other manufacturers just produce more of the older-style memory to fill the gap?

Building new semiconductor fabs requires immense capital investment and several years of lead time. With financial capital flowing decisively toward expanding production for high-margin HBM, there is little economic incentive for companies to invest billions in new or expanded fabs for lower-margin conventional DRAM. This leaves the consumer electronics industry with no immediate alternative to the constrained supply.