Exxon Mobil CCUS Strategy, $331 M DOE Grant Canceled, $10 B Investment Cut, and 2 Key Projects at Risk (2025)

CCUS Projects at Risk, Exxon Mobil Faces Policy Whiplash

In 2025, Exxon Mobil’s strategy for industrial-scale decarbonization was fundamentally destabilized by abrupt U.S. policy changes, exposing the high financial risks of projects dependent on government incentives. The company’s model of “distributed decarbonization, ” which focused on providing centralized Carbon Capture, Utilization, and Storage (CCUS) services to a network of industrial emitters, was predicated on stable policy. The passage of the “One Big Beautiful Bill Act” (OBBBA) in mid-2025 initiated the repeal of crucial clean energy tax credits, including Section 45 Q for carbon sequestration and Section 45 V for clean hydrogen, directly undermining the economic foundation of Exxon Mobil’s flagship projects.

- In early 2025, the strategy appeared on track, exemplified by a major agreement to capture and store 2 million metric tons of CO₂ annually for Calpine’s power plant and an offtake deal with Marubeni for 250, 000 tonnes of low-carbon ammonia.

- The OBBBA legislation reversed this momentum by altering the tax credits that made these large-scale projects financially viable, shifting the primary business risk from technological execution to political uncertainty.

- The immediate impact was the cancellation of a $331 million Department of Energy (DOE) grant for Exxon Mobil’s Baytown hydrogen facility, which was part of a broader termination of $3.7 billion in awards for 24 clean energy projects nationwide.

- This policy whiplash demonstrated that even with proven technology and clear market demand, the viability of the current generation of large-scale Carbon Capture projects is almost entirely contingent on durable government support.

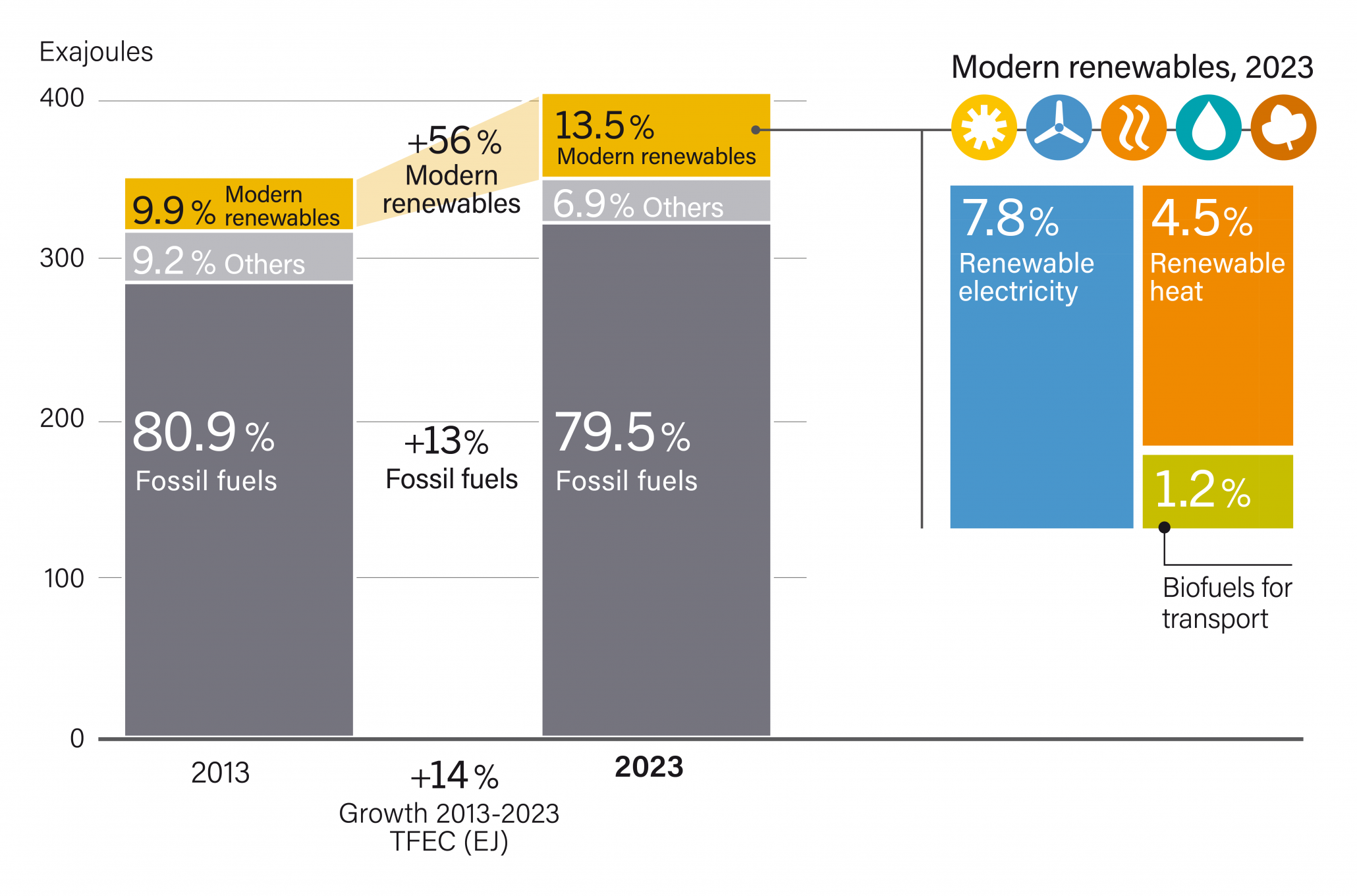

Fossil Fuels Retain 80% Share of Global Energy

This chart establishes the strategic importance of CCUS for ExxonMobil. It shows the continued dominance of fossil fuels, which underscores why policy changes that put CCUS projects ‘at risk’ represent a significant threat to the company’s core business.

(Source: REN21)

$10 B Cut, Exxon Mobil Slashes Low-Carbon Investment Plan

The mid-2025 policy reversal triggered a rapid and significant retrenchment in Exxon Mobil’s low-carbon capital expenditure, signaling a pivot back to a more conservative investment posture for projects with high subsidy exposure. The loss of anticipated government funding and tax credits forced a direct re-evaluation of the profitability and risk profile of its most ambitious low-carbon initiatives, leading to immediate and severe budget cuts.

- The most direct financial blow was the cancellation of the $331 million DOE grant, which was intended to support the development of the Baytown low-carbon hydrogen facility.

- This created a ripple effect, placing the entire $7 billion Baytown plant, planned to be the world’s largest, at high risk of significant delays or outright cancellation due to the altered economic landscape.

- By December 2025, Exxon Mobil formalized its strategic retreat by announcing a one-third reduction in its planned low-carbon technology investments for the 2025-2030 period, slashing the budget from $30 billion down to $20 billion.

Chart Details Cash Flow During 2025 Investment Cuts

This is a direct match. The section heading explicitly mentions the ‘$10 B Cut’ and slashed investment plan, and this chart provides the corresponding financial data by detailing the impact on cash flow.

(Source: Exxon Mobil Investor Relations)

Table: Exxon Mobil 2025 Low-Carbon Investment Reversals

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Low-Carbon Solutions Budget | Dec 10, 2025 | Reduced the 2025-2030 investment plan by $10 billion (from $30 B to $20 B) in response to the repeal of tax incentives, signaling a broad retrenchment from capital-intensive clean energy projects. | edie |

| Baytown Low-Carbon Hydrogen Plant | Aug 11, 2025 | Announced that the $7 billion project was at risk of delay or cancellation, as its economic viability was heavily dependent on the now-repealed 45 V clean hydrogen tax credits. | Energy Capital HTX |

| DOE Grant for Baytown Plant | May 30, 2025 | The U.S. Department of Energy canceled a previously awarded $331 million grant for the Baytown project as part of a wider termination of clean energy funding. | Upstream |

Exxon Mobil Partnerships: Calpine and Marubeni Deals Show Pre-Crisis Strategy (2025)

Before the policy-driven crisis of mid-2025, Exxon Mobil’s partnerships demonstrated a clear and logical strategy to build a services market for carbon management and low-carbon fuels. These agreements were designed to secure anchor customers and validate the “distributed decarbonization” model, leveraging the company’s infrastructure and expertise in the U.S. Gulf Coast. These deals represent a snapshot of a strategy that was viable under a stable, supportive policy regime.

- The agreement with Calpine, signed in April 2025, was a cornerstone of the services model, committing Exxon Mobil to transport and store up to 2 million metric tons of CO₂ annually, effectively creating a third-party market for carbon storage.

- In May 2025, the company secured a long-term offtake agreement with Japanese trading house Marubeni to supply 250, 000 tonnes of low-carbon ammonia per year, creating a guaranteed revenue stream for its planned Baytown hydrogen facility.

- A technology collaboration with IBM to explore quantum computing for discovering new carbon capture materials shows a parallel commitment to longer-term R&D, which is less exposed to short-term policy shifts but aims to lower future project costs.

LCI Hydrogen Key to Lowering Net Zero Cost

This chart explains the economic rationale for pursuing hydrogen projects, which directly relates to the strategic partnerships with Calpine and Marubeni mentioned in this section, as these deals are focused on developing hydrogen and CCUS infrastructure.

(Source: ExxonMobil)

Table: Key Exxon Mobil 2025 Strategic Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| IBM | Jul 20, 2025 | Engaged in a long-term R&D collaboration to use quantum simulations for discovering better catalysts and materials for carbon capture, aiming to reduce future costs. | Medium |

| Marubeni | May 2025 | Signed a long-term offtake agreement for 250, 000 tonnes of low-carbon ammonia per year from the Baytown facility, securing a key customer for its hydrogen production. | Oxford Institute for Energy Studies |

| Calpine | Apr 23, 2025 | Finalized a CO₂ transportation and storage agreement to manage up to 2 million metric tons of emissions annually, establishing its CCS-as-a-service business model. | Exxon Mobil |

US Gulf Coast, Exxon Mobil’s Centralized Hub Strategy Faces New Risk

Exxon Mobil’s geographic strategy heavily concentrated its low-carbon ambitions in the U.S. Gulf Coast, a region rich in industrial infrastructure, port access, and suitable geology for CO₂ storage. This hub-based approach, centered around Baytown, Texas, was designed for maximum operational and capital efficiency. However, the events of 2025 revealed that this geographic concentration also created a highly concentrated exposure to U.S. federal policy risk.

- Prior to 2025, the strategic focus was on securing assets and partnerships in the Gulf Coast, which was seen as an ideal execution environment.

- The deals with Calpine and Marubeni, both tied to the Baytown hub, demonstrate how the regional strategy was being implemented to create a closed-loop ecosystem of supply (hydrogen, CCS) and demand (industrial emitters, offtake partners).

- The mid-2025 policy shift transformed this geographic advantage into a liability, as the financial viability of the entire hub was threatened by a single legislative event in Washington D.C.

- This contrasts with a more geographically diversified approach, which might have spread political risk across different jurisdictions but would have been less capital-efficient. The 2025 crisis validates the high-risk, high-reward nature of Exxon Mobil’s concentrated bet.

Oil & Gas Electrification Market Projects Strong Growth

This chart aligns with the ‘Centralized Hub Strategy’ for the US Gulf Coast, a major industrial area for ExxonMobil. Electrifying operations is a key decarbonization lever for such hubs, and the growth in this market is directly relevant to the strategy and risks discussed.

(Source: maximize market research)

CCUS Technology Maturity, Exxon Mobil Proves Commercial Readiness Is Not Enough

In 2025, Exxon Mobil proved that its core CCUS technology is commercially mature, but it also learned that technological readiness is insufficient to ensure project success in the absence of a stable and supportive economic framework. The company’s ability to execute large-scale projects like the Calpine storage agreement relied on technologies with a high Technology Readiness Level (TRL 9), shifting the primary source of risk from the engineering lab to the legislative chamber.

- The focus of activity before 2025 was largely on proving that CCUS could work reliably at scale. The projects launched in 2025 operated on the assumption that this question was answered, with the Global CCS Institute rating the technology as fully commercial.

- The central challenge that emerged in 2025 was not whether the technology worked, but whether it could be profitable without the substantial tax credits offered by the Inflation Reduction Act (IRA).

- The policy reversal proved that for now, the answer is no. The economics of DAC and CCUS remain fundamentally dependent on government incentives to bridge the cost gap with conventional alternatives. While some companies like Bloom Energy are finding subsidy-free niches in areas like powering data centers, large-scale industrial decarbonization has not reached that point.

- This highlights a critical market failure: even with mature technology and willing industrial partners, the high capital cost of decarbonization infrastructure cannot be supported by the market alone, making policy the single most important variable. This is a challenge faced by other SOFC providers like Ceres Power as they also target the data center market.

Industrial Electrification and Renewables Growing by 2022

The section argues that CCUS ‘commercial readiness is not enough.’ This chart supports that argument by showing the growth of competing decarbonization pathways (electrification and renewables), which represent a key market challenge for CCUS technology.

(Source: REN21)

SWOT Analysis: Exxon Mobil’s Decarbonization Strategy and Its Policy Exposure

The analysis of Exxon Mobil’s 2025 activities reveals that while the company possesses significant operational strengths and identified clear market opportunities, its low-carbon strategy’s structural dependence on external policy created a critical vulnerability. The rapid unraveling of its plans following the mid-year legislative changes underscores this imbalance.

- Strengths in project management and financial capacity were unable to insulate the strategy from external political shocks.

- The core Weakness, a high dependency on subsidies for profitability, was exposed and became the defining challenge of the year.

- The Opportunity in industrial decarbonization remains large, but the viable pathways to capture it have narrowed significantly.

- The primary Threat of policy risk, once a theoretical concern, materialized with severe financial and strategic consequences. Even with a breakout in the SOFC data center market, broader decarbonization remains policy-dependent.

ExxonMobil Projects Higher Energy Demand Than Peers

A SWOT analysis critically examines a company’s strategic assumptions. This chart highlights a key assumption where ExxonMobil’s forecast differs from its peers, representing a potential risk or strategic vulnerability ideal for discussion in a SWOT context.

(Source: RFF.org)

Table: SWOT Analysis for Exxon Mobil CCUS Initiatives (2025)

| SWOT Category | Early 2025 (Pre-OBBBA) | Late 2025 (Post-OBBBA) | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Financial strength ($55 B cash flow in 2024), large-scale project execution, and deep geological expertise are leveraged to build a new business line. | Core competencies and financial strength remain intact, but are redirected toward the traditional oil and gas business as the low-carbon case weakens. | Validated that operational strengths alone cannot overcome a flawed economic model. The company’s core business remains its primary value driver. |

| Weaknesses | The business model’s profitability is heavily reliant on IRA tax credits (45 Q, 45 V), creating a dependency on stable government policy. | This dependency is fully exposed as a critical vulnerability. The strategy proves fragile and unable to stand without the subsidies it was designed around. | Validated the hypothesis that the strategy was not economically robust on its own. The weakness was not theoretical; it was a structural flaw. |

| Opportunities | The company is positioned to capture a large share of the industrial decarbonization market by serving as a first-mover in CCS and low-carbon hydrogen infrastructure. | The market opportunity still exists, but the timeline is extended and the path to profitability is now uncertain. The addressable market is effectively smaller without subsidies. | Validated that a market opportunity does not equate to a viable business case. The “demand” was largely an artifact of the subsidy structure. |

| Threats | Political risk and potential changes to the IRA are acknowledged but are considered manageable risks in the pursuit of first-mover advantage. | The primary threat materializes. The “One Big Beautiful Bill Act” directly targets and repeals the incentives, causing immediate financial and strategic damage. | Validated policy risk as the single greatest threat to capital-intensive energy transition projects in the U.S. It is no longer a risk but a realized event. |

Exxon Mobil 2026 Outlook: Baytown FID and the Viability of Unsubsidized CCUS

The critical signal to watch for in 2026 is Exxon Mobil’s Final Investment Decision (FID) on the Baytown project, as this will define the new economic threshold for large-scale low-carbon projects in a post-subsidy environment. The company’s next move will serve as a market-wide indicator of the true commercial viability of CCUS and blue hydrogen without substantial government support.

- If Exxon Mobil proceeds with a scaled-down Baytown project, watch for new, smaller-scale partnerships that rely on different economic models, potentially targeting niche applications where customers are willing to pay a green premium.

- If Exxon Mobil cancels Baytown, watch for a significant reallocation of the remaining $20 billion in low-carbon capital toward less policy-dependent areas like biofuels, advanced recycling, or technologies with a clearer path to unsubsidized profitability.

- The pace and scale of new CCS agreements will be the key metric. The “distributed decarbonization” model may survive, but it will likely be smaller and more targeted. A return to large, multi-million-tonne agreements is improbable without a restoration of robust government incentives.

US Hydrogen Market to Reach $33B by 2030

This section discusses the future of the Baytown project, a major low-carbon hydrogen facility. This chart provides the market context and commercial justification for considering the final investment decision (FID), illustrating the potential size of the US hydrogen market.

(Source: MarketsandMarkets)

The questions your competitors are already asking

This report covers one angle of the impact of policy uncertainty on large-scale CCUS projects. The questions that matter most depend on your work.

- What is the outlook for industrial-scale CCUS deployment in the U.S. following the repeal of the Section 45Q and 45V tax credits?

- What is the status of ExxonMobil’s flagship Baytown hydrogen facility and Calpine CO₂ capture projects since the policy reversal?

- Which companies are gaining or losing ground in the U.S. industrial decarbonization market after the 2025 policy changes?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.