Chevron Data Center Power, 4 GW GE Vernova Plan, $9 B Investment, and 2.5 GW Texas Project (2025)

Grid Bypass Projects, Chevron’s 4 GW Plan for Data Center Power

In 2025, Chevron initiated a significant strategic maneuver to bypass grid infrastructure constraints by developing dedicated, behind-the-meter natural gas power plants for the burgeoning Artificial Intelligence industry. This strategy leverages its core strength in natural gas to offer the high-reliability power that AI data centers require, positioning the company as a key enabler of the digital economy rather than a direct competitor in the utility-scale renewables market. This approach directly capitalizes on grid transmission bottlenecks that hinder the rapid connection of new power-hungry facilities.

- Prior to 2025, Chevron‘s lower-carbon efforts were primarily directed at biofuels and traditional Carbon Capture, Utilization, and Storage (CCUS), with distributed energy generation not being a central part of its public-facing strategy.

- A definitive shift occurred on January 28, 2025, with the announcement of a landmark partnership with GE Vernova and activist investor Engine No. 1 to develop up to four gigawatts (4 GW) of natural gas-powered generation connected directly to data centers.

- This strategic framework quickly materialized into tangible projects, most notably a planned 2.5 GW natural gas facility in the Permian Basin, Texas, which entered the critical permitting and engineering phases in late 2025.

- By co-locating generation with data centers, Chevron circumvents the grid constraints and lengthy interconnection queues that challenge renewable energy projects, offering a faster and more reliable power solution for a sector where uptime is critical.

- This model establishes a “twin-engine” advantage, where Chevron both utilizes AI to optimize its own drilling operations and simultaneously creates a new, long-term demand for its core natural gas product by supplying the AI sector itself.

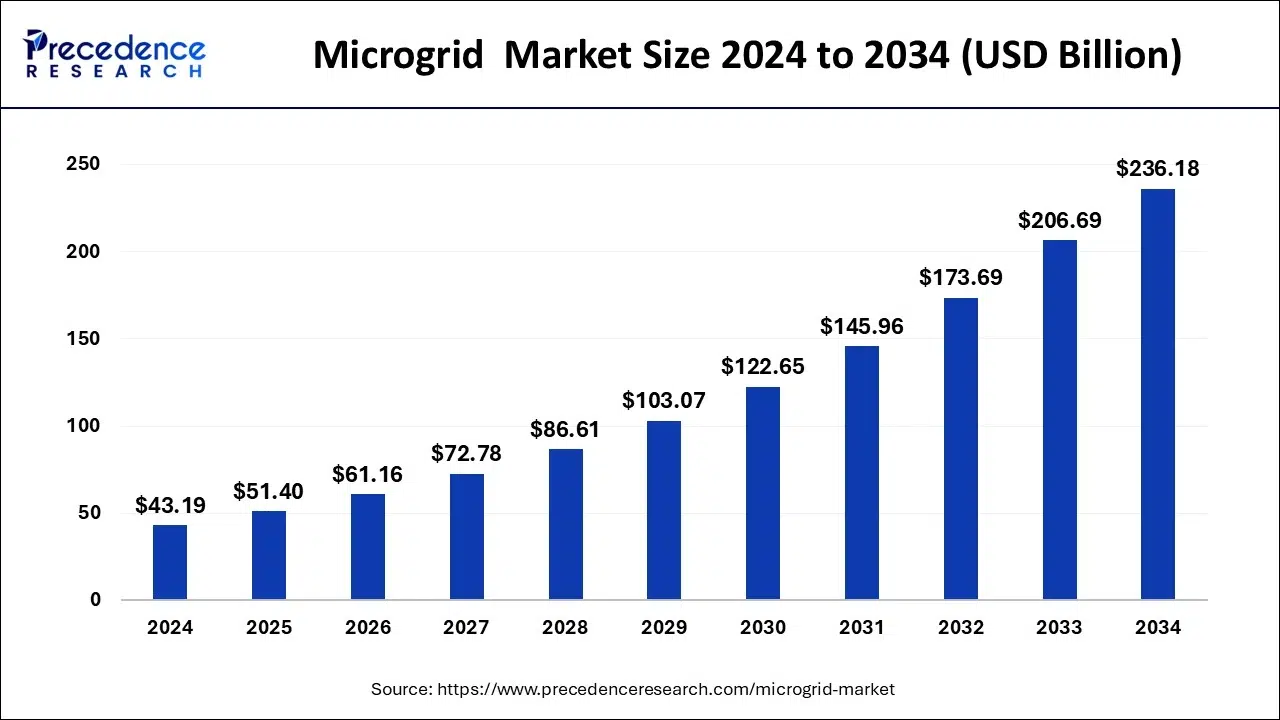

Microgrid Market Projected to Exceed $236B by 2034

The section discusses Chevron’s ‘Grid Bypass Projects,’ which are a form of decentralized power generation. This chart, showing the massive growth in the microgrid market, directly quantifies the market opportunity for the strategy described.

(Source: Precedence Research)

$9 B US Investment, Chevron 2025 Capital Plan for O&G and Power Gen

Chevron is underpinning its strategic entry into power generation with substantial capital allocations drawn from its profitable oil and gas business, creating a self-reinforcing cycle where core operations fund new growth ventures. The company’s 2025 financial planning demonstrates a dual focus on maximizing returns from existing assets while directing significant funds toward building out this new energy-for-AI vertical. This financial structure ensures the power generation initiatives are well-supported through long development cycles.

- For the 2025 fiscal year, Chevron planned to invest nearly $9 billion in its U.S. energy projects, a sum that supports both increased natural gas production in areas like the Permian Basin and the initial development of the power plants that will consume that gas.

- Looking ahead, the company announced an organic capital expenditure budget of $18 billion to $19 billion for 2026, signaling a sustained commitment to funding long-cycle projects, including the new data center power initiatives.

- These investments are part of a broader commitment to allocate $10 billion to lower-carbon projects between 2022 and 2028, a category that includes the hydrogen and CCUS initiatives designed to support and decarbonize the natural gas value chain.

Chevron Revenue Dominated by O&G Segments

This section details Chevron’s dual investment in O&G and Power Gen. The chart shows Chevron’s current heavy reliance on O&G revenue, providing the strategic context and justification for diversifying into power generation.

(Source: Blog – Bullfincher)

Table: Chevron 2025-2026 Strategic Capital Allocation

| Investment Area | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| 2026 Capex Budget | 2026 (Planned) | $18 B – $19 B budget to balance short-cycle oil and gas projects with long-cycle initiatives like data center power generation. | Chevron Newsroom |

| U.S. Energy Projects | 2025 | Nearly $9 billion invested in U.S. projects, including Permian Basin production growth to supply gas for new power plants. | Chevron Newsroom |

| Low-Carbon Ventures | By 2028 | $10 billion commitment to projects in hydrogen, CCUS, and renewable fuels that support the broader energy transition strategy. | Industrial Info |

Energy Industry Investment Priorities Highlighted

The section is a table outlining Chevron’s strategic capital allocation. This chart provides broader industry context by highlighting investment priorities, allowing a comparison of Chevron’s strategy against industry trends.

(Source: Turbomachinery Magazine)

Chevron 3 Major Energy Partnerships, GE Vernova and Engine No. 1 (2025)

Chevron‘s 2025 distributed energy strategy is not a solo endeavor but is constructed upon a network of key alliances that bring together fuel supply, technology, and investment expertise. These partnerships allow the company to de-risk its entry into the power generation market and accelerate project development by leveraging the core competencies of its collaborators. The structure of these deals reflects a pragmatic approach to building a new business line.

- The cornerstone collaboration is the joint development plan with GE Vernova and Engine No. 1. This alliance combines Chevron’s natural gas resources, GE’s turbine technology and manufacturing capabilities, and Engine No. 1’s strategic focus on energy transition investments.

- A partnership with One H 2, announced in October 2025, demonstrates a different facet of its distributed energy strategy. This collaboration aims to create a “pipeline on wheels” by deploying mobile hydrogen fueling stations for transportation and industrial customers, bypassing the need for fixed infrastructure.

- The ongoing agreement with CF Industries to store 500, 000 tonnes of CO₂ annually is a critical enabling partnership. It provides a pathway to decarbonize the natural gas value chain that underpins the entire data center power strategy, addressing a key environmental concern.

Table: Chevron 2025 Strategic Partnership Agreements

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| GE Vernova & Engine No. 1 | Jan 2025 | Jointly develop up to 4 GW of natural gas-fired power for U.S. data centers, combining fuel, technology, and investment strategy. | Chevron Newsroom |

| One H 2 | Oct 2025 | Expand access to hydrogen fuel through a network of mobile fueling solutions, targeting transportation and industrial customers. | Ressources Insights |

| CF Industries | May 2025 | Agreement for Chevron to capture and store 500, 000 tonnes of CO₂ per year from a manufacturing complex, building out its CCUS service business. | NYU Stern |

Distributed Control System Market Nears $30B

The section details partnership agreements with technology-focused companies like GE Vernova. This chart highlights the significant market value of Distributed Control Systems, a key technology for integrating the complex power and O&G assets that these partnerships will manage.

(Source: MarketsandMarkets)

US Permian Basin, Chevron Focus for 2.5 GW Data Center Power Project

Chevron‘s distributed energy strategy is geographically anchored in the United States, specifically co-locating new power generation with its most abundant and low-cost natural gas resources in the Permian Basin. This geographic focus is a deliberate choice to create a vertically integrated solution, minimizing fuel transportation costs and maximizing operational synergies. The strategy contrasts sharply with geographically dispersed renewable projects that often face significant transmission hurdles.

- While Chevron‘s activities between 2021-2024 involved a global portfolio of projects, its 2025 power generation initiative is distinctly focused on the U.S. domestic market.

- The flagship project, a 2.5 GW natural gas power plant, is sited in the Permian Basin of West Texas, the heart of Chevron‘s U.S. shale production.

- This location is highly strategic, as it places the power plant directly at the source of its fuel supply, creating a highly efficient and cost-effective operational loop.

- By building power infrastructure in the same region as its upstream assets, Chevron insulates its projects from the volatility and constraints of long-distance fuel transport and inter-regional grid congestion.

Oil & Gas Electrification Market to Surge

The section focuses on a power project in the Permian Basin, a major oil and gas hub. This chart directly illustrates the growing trend of electrification within the O&G industry, making it the perfect market context for this specific project.

(Source: maximize market research)

SWOT Analysis of Chevron’s Data Center Power Generation Strategy

An analysis of Chevron’s strategic pivot into powering data centers reveals a commercially astute plan that leverages core strengths but also introduces new risks and dependencies. The strategy is well-positioned to capitalize on the explosive energy demand from the AI sector, but its reliance on fossil fuels creates long-term exposure to regulatory and market shifts toward decarbonization.

Economic Conditions, Volatility Top Energy Industry Concerns

This section is a SWOT analysis of Chevron’s strategy. The chart, which lists top industry concerns like economic volatility, directly illustrates the external ‘Threats’ and challenges that would be a critical component of this analysis.

(Source: Turbomachinery Magazine)

Table: SWOT Analysis for Chevron’s 2025 Data Center Power Initiative

| SWOT Category | Key Factors |

|---|---|

| Strengths | Access to vast, low-cost natural gas reserves in the Permian Basin; World-class large-scale project management and execution capabilities; Strong balance sheet to fund capital-intensive projects; Established technology partnership with GE Vernova. |

| Weaknesses | Increased reliance on a single commodity (natural gas); Reputational risk from investing heavily in new fossil fuel infrastructure amid decarbonization pressures; Long development and permitting cycles for power plants could delay market entry. |

| Opportunities | Massive, inelastic, and growing demand for reliable power from the AI data center industry; Grid congestion and interconnection delays for renewables create an opening for grid-bypass solutions; Potential to pair natural gas generation with CCUS to create a lower-carbon power offering and generate carbon credits. |

| Threats | Future state or federal regulations on carbon emissions that could increase operational costs; Faster-than-expected commercialization of competing high-reliability, clean power technologies like Solid Oxide Fuel Cells (SOFCs), Small Modular Reactors (SMRs), or enhanced geothermal; A shift in U.S. energy policy that restores or enhances subsidies for renewable energy, making it more cost-competitive. |

Fossil Fuels Dominate Energy Mix Despite Renewables’ Growth

As a SWOT analysis table, this section would evaluate Chevron’s position. This chart highlights a key ‘Strength’ and ‘Opportunity’: the continued dominance of fossil fuels (like natural gas for power) validates their strategy of leveraging existing assets to enter the power market.

(Source: REN21)

Chevron’s Next Move: Final Investment Decision on 2.5 GW Texas Plant

The most critical milestone for Chevron‘s distributed energy strategy in the year ahead is the Final Investment Decision (FID) for its planned 2.5 GW Permian Basin power plant. This decision will serve as the ultimate validation of the commercial model, transitioning the strategy from a plan to a tangible, multi-billion-dollar construction project. The terms of the underlying agreements will set the benchmark for this new market segment.

- If the FID is announced, watch for the identity of the data center offtaker and the specific terms of the associated Power Purchase Agreement (PPA). These details will reveal the profitability and risk profile of the venture.

- If the FID is delayed or canceled, watch for commentary related to permitting challenges, difficulties in PPA negotiations, or unfavorable shifts in construction costs or natural gas price forecasts.

- If the project moves forward at pace, these could be happening: other oil and gas majors may announce similar grid-bypass strategies, and traditional utilities could accelerate grid modernization plans to avoid further disintermediation by large industrial customers.

Power Generation Market to Reach $2.19T by 2032

The section discusses a final investment decision for a massive 2.5 GW plant. This chart provides the crucial business case by showing the enormous size and value of the power generation market, justifying such a significant capital expenditure.

(Source: Verified Market Research)

The questions your competitors are already asking

This report covers one angle of Chevron’s distributed energy commercialization. The questions that matter most depend on your work.

- What is actually happening with the Chevron and GE Vernova 4 GW partnership for data center power since the announcement?

- What is the outlook for deploying behind-the-meter natural gas power for AI data centers by 2030?

- Which hyperscalers and data center operators are adopting Chevron’s grid-bypass power solution?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.