AEM Electrolysis Deals: 250 MW In Solare Partnership, 50 MW H 2 Pro Project, and $750 M in DOE Funding (2021 to 2026)

Next-Gen Electrolyzer Adoption, Versogen and H 2 Pro Pilot Projects

Industry adoption is bifurcating between the large-scale deployment of established PEM technology for immediate industrial demand and strategic, targeted pilot projects for next-generation systems like AEM and E-TAC designed to resolve specific cost and renewable integration barriers. While mature technologies are being procured in the hundreds of megawatts for centralized green ammonia and refinery projects, emerging technologies are proving their commercial value through smaller, application-specific deployments that validate new business models and technical capabilities.

- Between 2021 and 2024, the market focused on demonstrating the viability of established technologies at scale, leading to procurement decisions for large-scale PEM and Alkaline systems to meet near-term decarbonization targets.

- The period from 2025 to 2026 marks a clear shift toward validating the commercial readiness of next-generation technologies. This is exemplified by Plug Power securing a 275 MW PEM electrolyzer contract for a green ammonia project, which contrasts with H 2 Pro‘s 50 MW project in Spain using its novel E-TAC technology to prove a direct-connect, off-grid solar-to-hydrogen model.

- Anion Exchange Membrane (AEM) electrolysis is moving from research to commercialization through targeted market entry. The partnership between U.S.-based Versogen and India’s In Solare Energy aims to build a 250-300 MW AEM electrolyzer factory, tailoring the technology for a high-growth region with strong government support for green hydrogen.

Electrolyzer Technology and Scale Visualized

This diagram explains the different electrolyzer technologies mentioned in the section, such as AEM and PEM, providing visual context for the split between large-scale and pilot projects.

(Source: IDTechEx)

$750 M in DOE Funding, Versogen Next-Gen Electrolyzer Scale-Up

Public funding and capital-efficient licensing models are the primary financial mechanisms accelerating next-generation electrolyzer technologies from the laboratory to commercial deployment, de-risking the critical and expensive manufacturing scale-up phase. This contrasts with established players who leverage corporate balance sheets and project financing for large, proven technology deployments.

- A primary catalyst for U.S. domestic manufacturing is the Department of Energy’s (DOE) $750 million funding allocation for 52 projects focused on advancing electrolysis manufacturing and recycling. This federal support is critical for startups and specialized technology firms to build production capacity and compete with scaled incumbents.

- Versogen‘s strategy in India exemplifies a capital-light approach. By licensing its AEM technology to In Solare Energy, Versogen secures market access and a path to gigawatt-scale production without bearing the full capital expenditure of building and operating the manufacturing facility itself.

- The market is also seeing the emergence of new service models, such as Green Hydrogen-as-a-Service (GHaa S), which are enabled by AI and digital twins. These models reduce the upfront investment required by end-users and are being adopted to optimize operations and energy procurement, which accounts for 60-80% of production costs.

Table: Next-Generation Electrolyzer Investments and Funding

| Entity / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| U.S. Department of Energy (DOE) | Apr 2026 | Announced $750 million in funding for 52 projects to advance clean hydrogen electrolysis, manufacturing, and recycling, aiming to reduce the cost of clean hydrogen in the U.S. | energy.gov |

| Plug Power / Hy 2 gen | Apr 2026 | Selected to supply a 275 MW PEM electrolyzer system for Hy 2 gen’s green ammonia project in Quebec, Canada, one of the largest contracts of its kind. | Fuel Cells Works |

| H 2 Pro / Doral Hydrogen | Mar 2026 | Signed an agreement for a 50 MW green hydrogen project in Spain, utilizing H 2 Pro’s innovative E-TAC technology in an off-grid configuration. | H 2 Pro |

Versogen 2 Key Partnerships, In Solare and Matteco Deals (2026)

Strategic partnerships in 2026 are focused on securing market access in high-growth regions and resolving specific material science bottlenecks, demonstrating a shift from the broad research collaborations of 2021-2024 to targeted commercialization efforts. These alliances are structured to simultaneously de-risk market entry and accelerate technology maturation.

Versogen’s Strategic Partnership in India

This chart directly illustrates the Versogen and InSolare partnership mentioned in the section, detailing the scale and strategic goals of the new Indian manufacturing facility.

(Source: LinkedIn)

- The partnership between Versogen and In Solare Energy is a template for market entry, combining Versogen’s core AEM technology with In Solare’s local manufacturing capability and market knowledge to build a 250-300 MW factory tailored to India’s National Green Hydrogen Mission.

- H 2 Pro‘s partnership with Doral Hydrogen for a 50 MW project in Spain is designed to validate a new business model. It proves the commercial and technical viability of its E-TAC technology for off-grid, solar-direct hydrogen production, a critical use case for regions with high renewable energy penetration.

- The collaboration between Matteco and Dunia Innovations, announced in January 2026, directly targets the materials science challenges of AEM electrolyzers. By focusing on next-generation functional layers, the partnership aims to solve durability and performance bottlenecks that could hinder mass production.

Table: Next-Gen Electrolyzer Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| H 2 Pro and Doral Hydrogen | Mar 2026 | Co-developing a 50 MW off-grid solar-to-hydrogen project in Spain using H 2 Pro’s E-TAC technology to prove the system’s efficiency with intermittent renewables. | gasworld |

| Versogen and In Solare Energy | Feb 2026 | Partnership to develop and commercialize AEM electrolyzers in India. In Solare will establish a manufacturing plant with an initial capacity of 250-300 MW. | Power Magazine |

| Matteco and Dunia Innovations | Jan 2026 | Launched a collaboration to develop next-generation functional layers for AEM electrolyzers, addressing material bottlenecks for large-scale deployment. | Fuel Cells Works |

India vs. Spain, Versogen and H 2 Pro Geographic Focus

The geographic deployment of next-generation electrolyzers is shifting from established R&D hubs in the U.S. and Europe to regions like India and Spain, which offer a combination of strong government policy, abundant renewable resources, and a clear market need for green hydrogen. This marks a transition from technology development to market-driven commercialization.

- During the 2021-2024 period, development was largely concentrated in established technology centers, with institutions like Germany’s Fraunhofer Institutes and U.S. national labs leading research efforts on new materials and systems.

- In 2026, India has emerged as a key battleground for AEM technology. Versogen’s partnership with In Solare is a direct response to India’s National Green Hydrogen Mission, which provides powerful incentives for local manufacturing and deployment to meet ambitious national targets.

- Spain is becoming a crucial proving ground for electrolyzer technologies designed to work with variable renewables. Its high solar irradiance makes it an ideal location for H 2 Pro and Doral Hydrogen to demonstrate the economic case for their 50 MW off-grid, solar-powered E-TAC project.

AEM Technology Status, Versogen Moves to Commercial Scale

Anion Exchange Membrane (AEM) electrolysis has advanced from a promising lab-scale concept to a commercially viable technology in 2026, validated by initial manufacturing partnerships and accelerated by the integration of Artificial Intelligence in materials discovery. Concurrently, novel architectures like H 2 Pro’s E-TAC are entering the demonstration phase at a significant scale, indicating a broadening technology front.

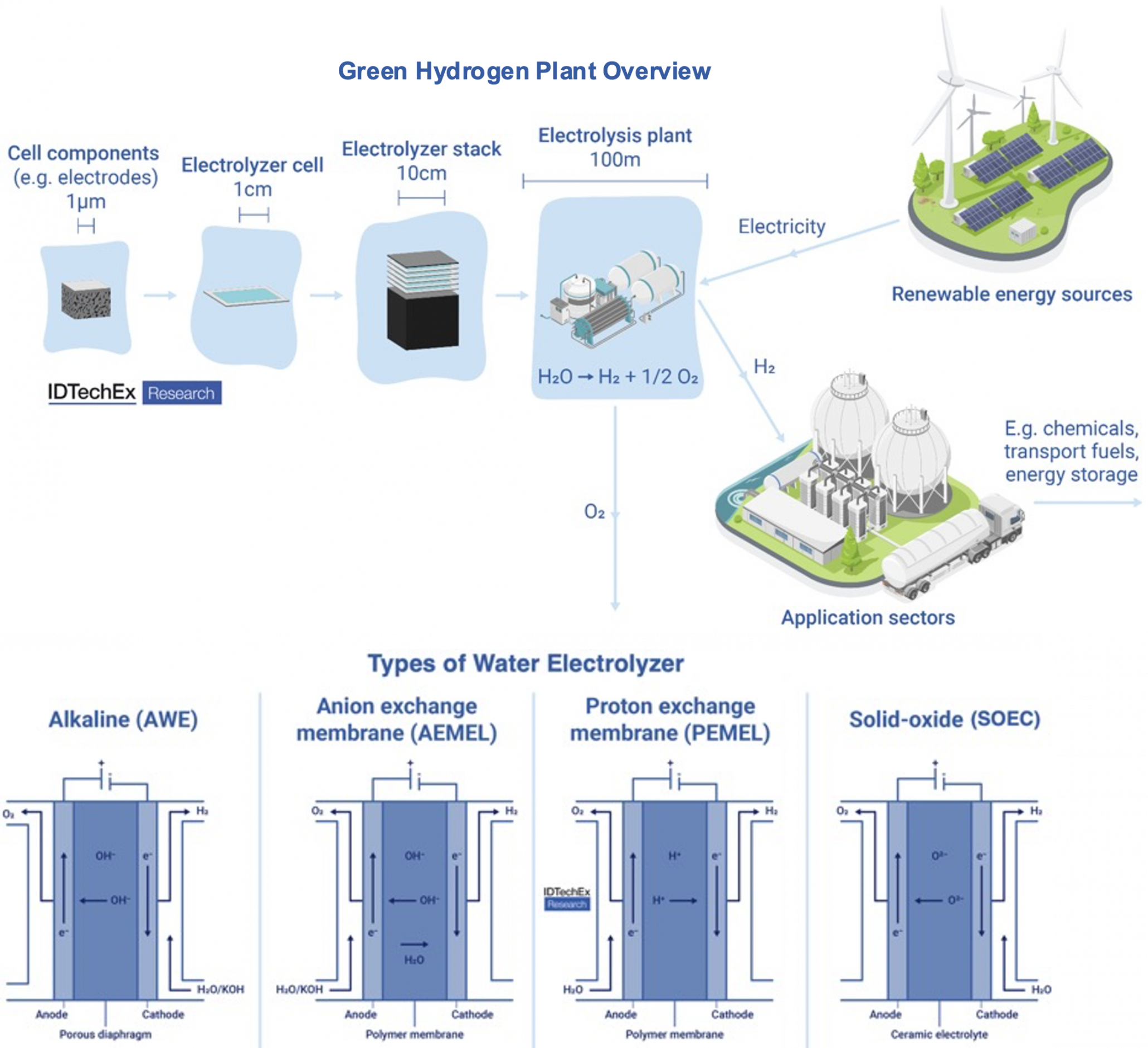

Comparing Four Key Water Electrolyzers

As this section details the advancement of AEM technology, this chart provides a technical breakdown of its components compared to other systems, clarifying its unique architecture.

(Source: IDTechEx)

- Between 2021 and 2024, AEM development was primarily focused on overcoming fundamental challenges with membrane and catalyst durability, which limited its commercial prospects compared to mature PEM and alkaline systems.

- In 2025-2026, the use of AI and machine learning to screen non-PGM catalysts and predict material degradation has drastically shortened R&D timelines. A January 2026 Nature publication highlighted ML-guided catalyst design using a commercial AEM from Versogen, showing a direct link between AI research and commercial technology enhancement.

- While AEM targets the cost advantages of alkaline and the performance of PEM, H 2 Pro’s E-TAC technology represents a more radical innovation. Its decoupled water-splitting process promises over 95% efficiency and is now moving from concept to a 50 MW commercial pilot, validating a new pathway for high-efficiency hydrogen production.

SWOT Analysis, Versogen Next-Gen Electrolyzer Positioning

Next-generation electrolyzers like AEM and E-TAC possess the strategic strength of lower potential capital costs and higher efficiency, but they face weaknesses related to limited manufacturing scale and a lack of long-term operational data. This creates distinct opportunities in specialized markets while leaving them exposed to threats from the rapid cost reductions and massive scale-up of incumbent PEM and alkaline technologies.

Electrolyzer Market Growth and Tech Split

This chart quantifies the market dominance of PEM and Alkaline technologies, visually representing the primary ‘Threat’ from incumbent systems as described in the SWOT analysis.

(Source: IDTechEx)

Table: SWOT Analysis for Next-Gen Electrolyzers

| SWOT Category | Strengths | Weaknesses | Opportunities | Threats |

|---|---|---|---|---|

| 2021 – 2024 | Theoretical cost advantage due to PGM-free catalysts (AEM). High efficiency potential in lab settings (E-TAC). | Poor membrane durability and catalyst stability. Lack of any commercial-scale manufacturing capacity or operational data. | Rising iridium prices for PEM created a strong R&D push for alternatives. Growing interest in green hydrogen policies. | Domination of the market by established, bankable PEM and Alkaline technologies. Perceived as high-risk, research-grade technology. |

| 2025 – 2026 | Demonstrated PGM-free operation (AEM) and high efficiency (>95% for E-TAC). AI-driven R&D accelerates material improvements. | Manufacturing capacity is still nascent (hundreds of MW vs. GW for incumbents). Long-term durability in commercial operation is unproven. | Strategic partnerships for market entry (Versogen in India). Niche applications like off-grid hydrogen (H 2 Pro in Spain). Massive government funding (DOE’s $750 M). | Incumbents like Plug Power are rapidly scaling PEM production and driving down costs. New supply chain bottlenecks could emerge for novel AEM components. |

Scenario Modeling: Versogen AEM and H 2 Pro E-TAC

The critical strategic action for 2027 is the successful execution of initial large-scale commercial projects, which will validate the bankability of AEM and E-TAC technologies and determine their adoption trajectory versus established PEM and Alkaline systems. The performance of these first-of-a-kind deployments will serve as the key signal for investors and industrial adopters.

The Integrated Green Hydrogen Ecosystem

This diagram illustrates the end-goal scenario for hydrogen integration, providing a visual model for the successful ‘adoption trajectory’ discussed in this section.

(Source: POWER Magazine)

- If This Happens: The 50 MW H 2 Pro project with Doral Hydrogen in Spain consistently meets its efficiency and operational targets through 2027. Watch For: Announcements of follow-on projects from Doral or new partnerships with other European renewable developers. This Could Be Happening: A rapid acceleration of investment into other off-grid, direct-connect renewable-hydrogen projects, establishing E-TAC as the preferred technology for this application.

- If This Happens: In Solare Energy successfully commissions its initial 250 MW AEM facility in India using Versogen‘s technology and secures its first major domestic offtake agreement. Watch For: Statements from Versogen about similar licensing agreements in other regions with strong hydrogen mandates, such as Brazil or Australia. This Could Be Happening: Validation of the technology licensing model as the fastest way to scale next-gen electrolyzer production globally, prompting competitors to follow suit.

- If This Happens: Reports emerge from early AEM deployments detailing lower-than-expected membrane lifetimes or catalyst degradation issues. Watch For: A slowdown in new AEM project announcements and a renewed focus in technical publications on durability rather than cost. This Could Be Happening: A re-consolidation of the market around proven PEM and alkaline technologies, delaying widespread AEM adoption by another 3-5 years.

The questions your competitors are already asking

This report covers one angle of next-generation electrolyzer commercialization. The questions that matter most depend on your work.

- Which companies are gaining ground in the next-generation electrolyzer market, and which are falling behind established players like Plug Power?

- How does AEM electrolysis compare to H2Pro’s E-TAC for off-grid, direct-connect solar-to-hydrogen projects?

- What is the status of the Versogen-In Solare partnership, and is the 250 MW AEM factory in India on track?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.