PEM Electrolysis Cost Barriers, 275 MW Plug Power-Hy 2 gen Deal, $2000/k W CAPEX, and 4 Commercial Projects (2021 to 2026)

Electrolyzer Project Viability, Plug Power 275 MW Deal Hinges on Economics

The industrial sector’s adoption of electrolyzers for decarbonization has shifted from small-scale pilots before 2025 to large commercial-scale commitments, but project viability is now determined by economic factors like subsidies and electricity pricing rather than technological maturity. While technically proven, large-scale projects face a significant cost gap against incumbent fossil-fuel-based production methods, making supportive policy and low-cost energy contracts the critical enablers for final investment decisions in 2026.

- Prior to 2025, industry activity centered on technology validation through smaller pilot projects. The period from 2025 to today is defined by the announcement of major commercial deployments, such as Plug Power securing the Front-End Engineering Design contract for a 275 MW PEM electrolyzer system for Hy 2 gen’s green ammonia project in Quebec.

- The Levelized Cost of Hydrogen (LCOH) from these projects consistently ranges from €2.5/kg to over €5.3/kg, based on electricity prices of €25-€100/MWh. This is substantially higher than the production cost of grey hydrogen, which sits around $1.50/kg, and far from the industry’s 2030 target of $1/kg.

- This economic reality means that the primary risk for project developers has moved from technology to finance. The success of new projects now hinges on securing long-term Power Purchase Agreements (PPAs) for renewable electricity at or below $0.03/k Wh and leveraging government support mechanisms like production tax credits or contracts for difference.

- Demand is broad, with electrolyzers being applied to produce green ammonia, green methanol, and to provide hydrogen for Direct Reduced Iron (DRI) steelmaking. This variety shows a clear decarbonization pathway for hard-to-abate sectors, but the high cost of green hydrogen remains the common barrier across all applications.

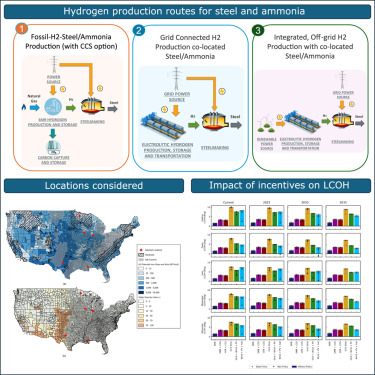

Incentives Are Key to Lowering Hydrogen Costs

This chart quantifies how policy incentives reduce hydrogen costs, directly supporting the section’s argument that economic factors, not technology, are the primary driver of project viability.

(Source: ScienceDirect.com)

Plug Power 4 Key Industrial Alliances Drive Electrolyzer Deployments (2026)

In 2026, strategic partnerships are the primary mechanism for de-risking large-scale electrolyzer projects, bundling technology, offtake agreements, and access to renewable energy to overcome prohibitive standalone costs. These collaborations are essential for assembling the capital-intensive value chains required to make green hydrogen economically feasible for industrial consumers.

Ammonia Market Shifts to Renewable Production

As the section highlights a partnership for a decarbonized ammonium nitrate plant, this chart visualizes the broader market shift to renewable ammonia, illustrating the end-market opportunity driving these collaborations.

- The partnership between Plug Power and Hy 2 gen Canada for the Courant Project exemplifies a technology-offtaker model. By supplying a 275 MW PEM electrolyzer, Plug Power provides the core technology for a large-scale green ammonia plant, creating a guaranteed offtake market for the hydrogen produced.

- A collaboration between utility-scale developer ACWA Power and technology firm AVL focuses on advancing Solid Oxide Electrolyzer Cell (SOEC) pathways. This partnership signals a strategic push toward higher-efficiency technologies to reduce the long-term operating costs associated with electricity consumption.

- The alliance between DRIFT and Enapter aims to develop marinised electrolyzer technology for offshore green hydrogen production. This initiative seeks to unlock vast, high-capacity factor renewable energy sources, directly addressing the critical need for low-cost, consistent power for electrolysis.

- Industrial end-users are also driving collaboration, as seen with Tubos Reunidos Group’s participation in the H 2 SKID project. This strategic initiative to develop a 1.25 MW portable electrolyzer is designed to accelerate the industrial validation and on-site supply of green hydrogen, demonstrating a need for flexible and modular solutions.

Table: Key Electrolyzer Partnerships and Projects (2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Plug Power / Hy 2 gen Courant Project | April 2026 | FEED contract for a 275 MW PEM electrolyzer system for a decarbonized ammonium nitrate plant in Quebec, creating a large-scale offtake agreement. | Process Worldwide |

| DRIFT and Enapter | March 2026 | Partnership to adapt and develop marinised electrolyzer technology for offshore green hydrogen production installations, targeting access to low-cost renewable energy. | Fuel Cells Works |

| ACWA Power and AVL | February 2026 | Collaboration to work on high-efficiency Solid Oxide Electrolyzer Cells (SOEC) and co-electrolysis pathways for utility-scale green hydrogen production. | ACWA Power |

| Tubos Reunidos Group / H 2 SKID Project | January 2026 | Participation in developing a 1.25 MW portable electrolyzer to accelerate industrial validation and supply of green hydrogen for on-site use. | Fuel Cells Works |

Europe and North America Lead, Plug Power Electrolyzer Demand Grows

While green hydrogen ambitions are global, in 2026, Europe and North America are the epicenters of tangible electrolyzer deployment, driven by strong regulatory incentives and the presence of established industrial offtakers ready to decarbonize. These regions are translating policy into large-scale projects, creating the most significant near-term demand for electrolyzer manufacturing capacity.

North America to Lead Global Market Share

This chart validates the section’s claim by forecasting that North America will command a leading 43.5% market share, quantifying the region’s role as an epicenter for electrolyzer demand.

(Source: Research Nester)

- Prior to 2025, green hydrogen activity and pilot projects were more geographically dispersed. The current landscape shows a concentration of large-scale project development in regions with the most robust policy frameworks and industrial demand.

- North America, particularly the US and Canada, has become a key growth market. The US Inflation Reduction Act (IRA) and the development of regional hydrogen hubs are fueling significant market expansion, while Quebec, Canada, is host to the 275 MW Hy 2 gen project, one of the largest announced deployments.

- Europe remains the fastest-growing region, underpinned by ambitious policy targets such as the European Union’s goal for 6 GW of installed electrolyzer capacity. This has created a strong demand signal, encouraging investment across the value chain and fostering projects like the H 2 SKID initiative in Spain.

- Asian nations are building strategic foundations for future demand. Japan is advancing its first large-scale low-carbon ammonia project, while Indonesia is developing a national strategy anchored by 17 clean ammonia projects, positioning themselves as future major importers and producers.

$2, 000/k W CAPEX, Plug Power PEM vs. SOEC Efficiency Battle

Electrolyzer technology is commercially mature for deployment, but 2026 is defined by a critical trade-off between the bankable, lower-efficiency PEM and Alkaline systems and the higher-efficiency, higher-CAPEX SOEC systems that promise better long-term economics. The market is currently bifurcated, with established technologies winning today’s large contracts while next-generation systems are positioned as a solution to the sector’s cost challenges.

SOEC Market Forecast to Exceed $4.2B

This chart provides a specific market forecast for SOEC technology, directly reinforcing the section’s discussion of the trade-off between established PEM and higher-efficiency SOEC systems.

(Source: Grand View Research)

- The period from 2021–2024 focused on demonstrating the operational viability of various electrolyzer technologies. In 2026, the central challenge has become economic performance at scale, particularly the high capital cost, which stands at approximately $2, 000 per kilowatt (k W) installed outside of China.

- Proton Exchange Membrane (PEM) electrolyzers and Alkaline (ALK) systems are the most commercially mature options, dominating current large-scale projects due to established supply chains. However, their electrical efficiency of 50–55 k Wh/kg results in high electricity consumption and operational expenditures.

- Solid Oxide Electrolyzer Cells (SOEC) represent the most efficient pathway, especially when integrated with industrial waste heat. This can significantly reduce electricity consumption, with companies like Hysata reporting a breakthrough efficiency of 41.5 k Wh/kg. However, SOECs currently face higher CAPEX and material degradation challenges.

- The market is also seeing development in other technologies like Anion Exchange Membrane Electrolysis (AEMEL), which aims to combine the benefits of PEM and ALK systems. The overall dynamic is a race to scale manufacturing and drive down the CAPEX of all technologies toward the industry’s sub-$500/k W target.

SWOT Analysis, Plug Power Electrolyzer Market Position and Risks

The electrolyzer market in 2026 presents strong growth opportunities driven by industrial decarbonization mandates, but its progress is threatened by persistent high costs and dependency on government policy. This creates a precarious balance for technology providers and project developers, where market demand is clear but the business case remains challenging without external support.

Electrolyzer Market Poised for Exponential Growth

This forecast of exponential growth to over $115 billion powerfully illustrates the ‘strong growth opportunities’ that form the core of the SWOT analysis discussed in this section.

(Source: Cervicorn Consulting)

Table: SWOT Analysis for Electrolyzer Industrial Decarbonization (2026)

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Technology viability demonstrated in pilots. Multiple technology pathways (ALK, PEM, SOEC) available. | Technology readiness for large-scale deployment confirmed. Growing political will for decarbonization. | The technology works at scale. The market has moved from a science problem to an economics and manufacturing problem. |

| Weaknesses | High CAPEX and unproven manufacturing scale-up. Nascent supply chains for key components. | CAPEX remains high (~$2, 000/k W outside China). LCOH is uncompetitive (€2.5-€5.3/kg) without subsidies. | The “cost chasm” between green and grey hydrogen is a persistent, quantified barrier that technology alone has not solved. |

| Opportunities | Massive potential market in hard-to-abate sectors (steel, ammonia, chemicals). | Strong policy drivers (IRA, EU targets) create demand. Co-location with renewables offers a path to low OPEX. | The addressable market is confirmed and growing, with policy support now acting as a primary market-making force. |

| Threats | Competition from other decarbonization pathways (e.g., CCUS). Volatility in renewable electricity prices. | Dependence on government subsidies creates policy risk. Slow PPA negotiations and grid connection delays. | The primary threat is now economic and political, not technical. Project viability is fragile and dependent on factors outside developers’ control. |

Future Scenarios, Plug Power Projects Hinge on Closing the Cost Chasm

The trajectory for 2027 hinges on whether the industry can begin closing the “cost chasm” by demonstrating tangible reductions in both electrolyzer CAPEX and the delivered price of green electricity. The success or failure of flagship projects announced in 2026 will serve as critical signals for the market’s future growth rate.

- If current economic barriers persist, expect a slowdown in final investment decisions for new large-scale projects in 2027. Only the most heavily subsidized projects will move forward, and announcements may outpace actual construction starts. Watch for project delays or scope reductions as developers contend with unfavorable cost structures.

- A key signal to watch is electrolyzer CAPEX reduction. Monitor whether new gigawatt-scale manufacturing facilities, especially in Europe and North America, begin to produce systems at a cost closer to the sub-$500/k W target. Progress here would be the most significant catalyst for market acceleration.

- Another critical signal is the bankability of integrated projects. The ability of large-scale renewable and electrolyzer projects to secure the requisite sub-$0.03/k Wh electricity via long-term PPAs will be a major bellwether. The financial close and construction progress of projects like Hy 2 gen’s will be scrutinized by the entire industry.

- If these cost and financing milestones are achieved, the market could enter a phase of exponential growth. If not, the 2026 “transition year” could extend into a multi-year period of slower, more fragmented deployment than current forecasts suggest.

The questions your competitors are already asking

This report covers one angle of the commercial viability of large-scale electrolyzers for industrial decarbonization. The questions that matter most depend on your work.

- What is actually happening with Plug Power’s 275 MW PEM electrolyzer deal for Hy 2 gen’s green ammonia project since the announcement?

- What is the outlook for large-scale electrolyzer deployment in the steel, ammonia, and chemical sectors by 2026?

- What is the cost breakdown of a utility-scale PEM electrolyzer system, from the $2000/kW CAPEX to the final Levelized Cost of Hydrogen (LCOH)?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.