Green Hydrogen in Cement 2026: 10 x Cost Gap vs. Coal, €600 M Decarbonization Plans, and 3 MW Pilot Projects (2021 to 2026)

Green Hydrogen in Cement, Pilot Projects Define Adoption Amid Cost Hurdles

The adoption of green hydrogen in cement production shifted from conceptual validation between 2021 and 2024 to integrated, policy-backed pilot projects by 2026, yet prohibitive fuel costs remain the primary barrier to commercial-scale deployment. While technical feasibility is increasingly proven in demonstration environments, the extreme operational expenditure increase compared to fossil fuels means no project can proceed without substantial external financial support, confining adoption to strategic, subsidized initiatives.

- Between 2021 and 2024, the industry validated hydrogen combustion primarily in adjacent high-temperature processes, setting the technical foundation for cement applications. Heidelberg Materials successfully used 100% hydrogen to produce asphalt, and Wienerberger AG began retrofitting brick kilns with hydrogen-capable burners. These projects proved the viability of the core technology outside of a full cement kiln environment.

- Starting in 2025, activity progressed to cement-specific pilots, demonstrating a higher Technology Readiness Level. A key project in Spain advanced a 3 MW scale solution to use hydrogen from syngas for direct kiln firing. Concurrently, large cement producers like Akmenės cementas announced massive decarbonization budgets exceeding €600 million, which include fuel switching to hydrogen as a potential pathway alongside carbon capture.

- Despite this technical progress, the economic case has not materialized. The fundamental constraint is the operational cost, with the price of green hydrogen remaining over ten times that of coal on an energy-equivalent basis. This reality ensures that all active projects are dependent on government funding or carbon pricing schemes, rather than market-based returns.

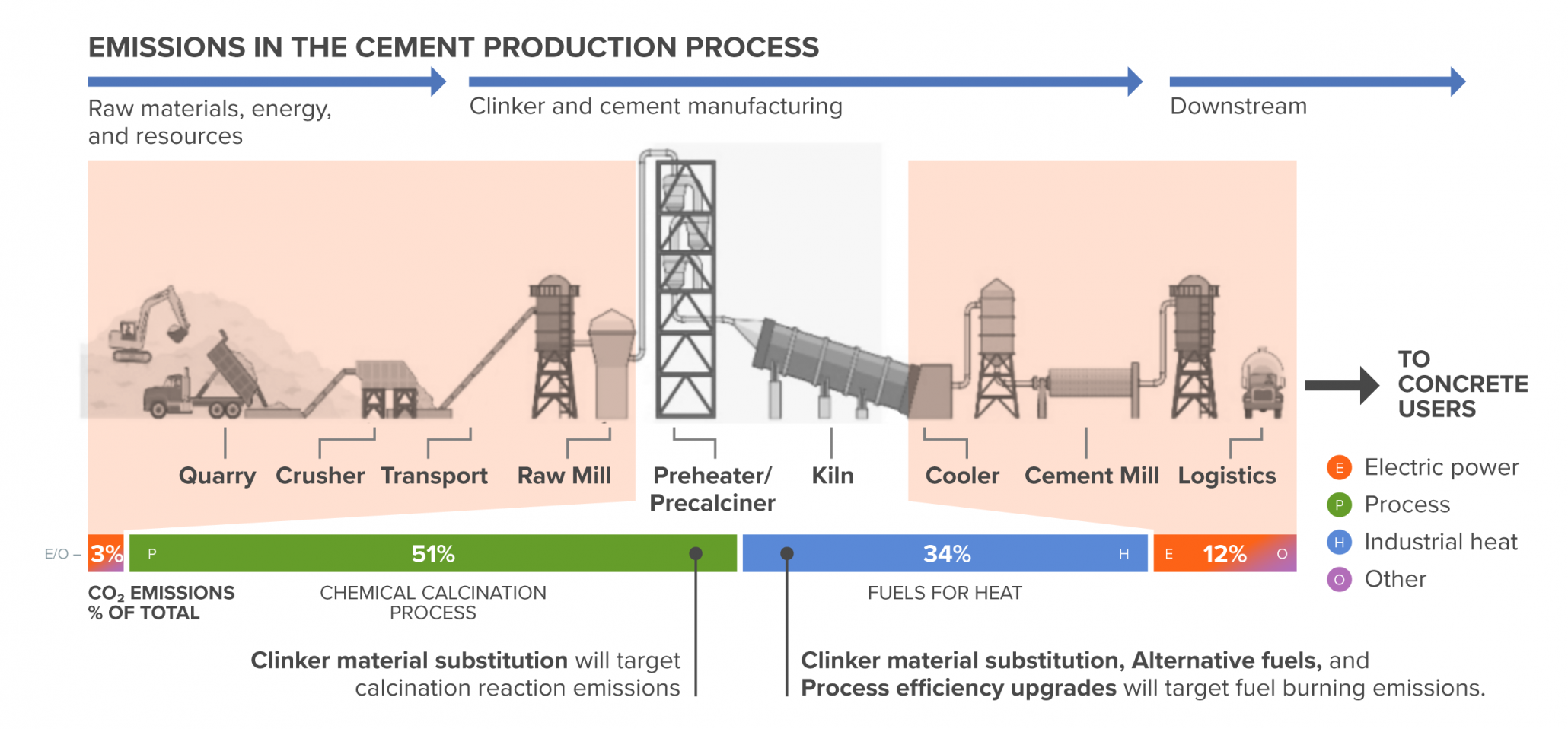

Fuel for Heat Drives 34% of Cement Emissions

This chart shows that burning fuel for heat is responsible for a third of cement’s CO2 emissions, visually identifying the exact problem that using green hydrogen as a fuel aims to solve.

(Source: Project Drawdown®)

€600 M Decarbonization Budget, Akmenės Cementas Highlights Policy-Driven Investment

Investment in hydrogen-based cement decarbonization through 2026 is characterized not by commercial viability but by strategic capital allocation underwritten by public funding and policy mandates. The final investment decisions for these high-CAPEX projects are entirely dependent on non-market financial mechanisms designed to bridge the profound cost gap with incumbent technologies, positioning them as government-backed strategic initiatives rather than market-driven ventures.

- Major capital commitments are being allocated to broad decarbonization programs where hydrogen competes with other technologies. The planned €600 million investment by Lithuania’s Akmenės cementas is for a suite of technologies that includes carbon capture and fuel switching, indicating that hydrogen is one of several capital-intensive options being evaluated, not a default choice.

- Direct government subsidies are the primary enabler for pilot projects moving forward. The Wienerberger AG brick kiln retrofit secured government funding to proceed, and the 3 MW Spanish cement pilot is supported by the EU’s CORDIS program. These initiatives mirror broader support mechanisms like the EU Hydrogen Bank, which directly subsidizes the cost per kilogram of produced green hydrogen.

- While over $150 billion was invested globally in the hydrogen value chain between 2021 and 2024, this capital is aimed at building the upstream supply chain. This massive capital injection into the upstream supply chain, with major electrolyzer manufacturers like Sunfire, ITM Power, Siemens Energy, and Cummins scaling production, is a prerequisite for eventually lowering the long-term cost of green hydrogen for industrial users.

Table: Strategic Decarbonization Investments and Funding

| Project / Funder | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Akmenės cementas | 2026 | Over €600 million ($648 million) allocated for a plant-wide decarbonization program, including potential fuel switching to hydrogen and a primary focus on Carbon Capture, Utilisation & Storage (CCUS). | Carbon Herald |

| H 2-CEMENT Project (Spain) | 2026 | EU funding via CORDIS for a 3 MW scale pilot to demonstrate kiln firing using hydrogen derived from purified syngas. The project aims to validate the technology in an operational environment. | CORDIS EU |

| EU Hydrogen Bank | 2026 | Provides direct subsidies per kilogram of green hydrogen produced via a competitive auction mechanism. This is designed to close the cost gap for producers and stimulate offtake agreements with industries like cement. | Ff E |

| Wienerberger AG | 2026 | Secured government funding to support the retrofit of two tunnel kilns, replacing 224 natural gas burners with hydrogen-capable models for brick manufacturing. | Agg-Net |

Europe Leads Hydrogen-for-Cement Pilots, EU Policy Creates Concentrated Activity

Europe has solidified its position as the global center for hydrogen-in-cement pilot activity, driven by a combination of targeted funding and robust carbon pricing policies that are beginning to penalize fossil fuel use. While other regions are developing hydrogen strategies, the EU’s proactive regulatory environment, particularly the launch of the Carbon Border Adjustment Mechanism (CBAM), creates the most compelling, albeit still challenging, business case for industrial decarbonization projects.

China Dominates Global Cement Production Capacity

This chart provides critical context for the section’s focus on Europe, showing that while the EU may lead in hydrogen pilots, its efforts are in a market dominated by Asian production.

(Source: Clean Air Task Force)

- European nations are home to the most advanced cement-specific hydrogen projects as of 2026. Spain is hosting a 3 MW kiln firing demonstration, and Lithuania’s Akmenės cementas is evaluating it as part of a major plant overhaul. This concentration of activity is a direct result of EU-level funding programs and the impending financial impact of the EU Emissions Trading System (ETS) and CBAM, which begins its full implementation in January 2026.

- In the 2021-2024 period, innovation was more globally distributed across adjacent sectors. Japan, for example, launched the world’s first commercial engine capable of generating electricity with a 30% hydrogen blend, demonstrating the viability of co-firing as a risk-mitigation strategy.

- Other regions are building foundational hydrogen economies, but with less specific focus on cement. The U.S. Inflation Reduction Act’s 45 Q tax credit of $85 per tonne of CO 2 primarily incentivizes CCUS. Meanwhile, interest in countries like India, evidenced by the NITI Aayog’s decarbonization roadmap and projects from firms like Alstom, shows growing momentum, but deployment remains behind Europe’s.

TRL 6-8 Reached, Hydrogen Combustion Proven in Pilots but Lacks Commercial Scale

The technology for combusting hydrogen in industrial kilns reached a Technology Readiness Level (TRL) of 6 to 8 by 2026, confirming its technical feasibility in operational and relevant environments, but it remains commercially immature. The progression from validating components and adjacent applications to integrated cement pilots has de-risked the technology, yet it cannot overcome the primary barriers of prohibitive fuel cost and the absence of scaled supply infrastructure.

- The period between 2021 and 2024 was crucial for proving the core technology in high-temperature applications that serve as proxies for cement. Heidelberg Materials’ successful trial of 100% hydrogen in asphalt production and Wienerberger’s brick kiln retrofits demonstrated that burners and control systems could perform as required.

- By 2026, the technology made the leap into dedicated cement pilots, such as the 3 MW demonstration project in Spain. This represents a move to TRL 7 (system prototype demonstration in an operational environment), closing a key gap in validating performance with the specific thermal and chemical demands of a cement kiln.

- However, hydrogen technology readiness lags behind competing decarbonization pathways. Carbon Capture, Utilisation, and Storage (CCUS) is considered TRL 7-9 and is being deployed at a larger scale. Simpler retrofits like Selective Non-Catalytic Reduction (SNCR) for NOx control are fully mature at TRL 9, offering a lower-cost, lower-risk (though non-CO 2-related) upgrade path for plant operators.

SWOT Analysis, Green Hydrogen Strengths Undercut by Economic Weaknesses

Green hydrogen’s potential to eliminate 40% of a cement plant’s CO 2 emissions from fuel combustion provides a clear technological strength, but this is rendered commercially unviable by its extreme cost disadvantage compared to fossil fuels. This fundamental economic weakness makes its adoption entirely dependent on policy-driven opportunities, while threats from more mature and cost-effective decarbonization pathways like CCUS remain significant.

Abatement Curve Compares Decarbonization Costs

This marginal abatement cost curve visualizes the core of the SWOT analysis, illustrating the economic trade-offs and cost competition between hydrogen and other technologies like CCUS.

(Source: ScienceDirect.com)

Table: SWOT Analysis for Green Hydrogen in Cement

| SWOT Category | 2021 – 2023 | 2024 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Theoretical zero-carbon heat source. Proven in adjacent industries (e.g., asphalt production with Heidelberg Materials). | Demonstrated technical feasibility in a cement-specific pilot at 3 MW scale. Addresses the 40% of emissions from fuel combustion. | The technology’s strength shifted from a theoretical potential to a demonstrated capability within a relevant cement kiln environment. |

| Weaknesses | High projected cost of green hydrogen ($3.00-$6.00/kg). Anticipated CAPEX premium for retrofits. | Cost gap is quantified and confirmed as prohibitive: green hydrogen is 10 x-12 x more expensive than coal per gigajoule ($33-$50/GJ vs. $2-$4/GJ). | The primary weakness evolved from a high-level cost concern into a stark, quantified economic barrier preventing standalone commercial projects. |

| Opportunities | General momentum from over $150 billion in global hydrogen investments and national hydrogen strategies. | Specific, actionable policy mechanisms come online, including the EU Hydrogen Bank’s direct subsidies and the 2026 start of the EU CBAM. | The opportunity matured from broad investment trends to targeted policy instruments that can directly fund pilot projects and create a market. |

| Threats | Competition from established alternative fuels like Refuse-Derived Fuel (RDF), which offer a lower-cost pathway. | CCUS emerges as a more mature (TRL 7-9) and direct competitor, with large firms like Akmenės cementas evaluating it in tandem with hydrogen. | The competitive threat has crystallized around CCUS, which addresses both fuel and process emissions and is perceived as a more scalable near-term option. |

2026 Scenario: Co-firing and Niche Projects Await H 2 Cost and Carbon Price Signals

For the year ahead, the adoption of hydrogen in the cement industry will likely be confined to incremental co-firing and a few heavily subsidized, full-conversion demonstration projects. Final Investment Decisions for widespread retrofits are on hold, contingent upon a significant drop in the green hydrogen price to below $2/kg and a substantial rise in effective carbon prices that make fossil fuel use financially unsustainable.

Hydrogen’s Climate Benefit Hinges on Production

This chart explains the premise of the 2026 scenario by showing that only hydrogen from renewable sources is truly low-carbon, clarifying why the industry awaits a low ‘green hydrogen’ price signal.

(Source: Energy Central)

- If green hydrogen production costs remain elevated near $4.00/kg, watch for project developers to pivot from full-conversion plans to co-firing hydrogen with natural gas at lower blend rates (e.g., 10-30%). This approach mitigates the extreme OPEX impact while allowing firms to gain operational experience and achieve partial decarbonization.

- If the effective carbon price in the EU ETS unexpectedly accelerates past $100/tonne, watch for an uptick in front-end engineering and design (FEED) studies for hydrogen retrofits. A high and stable carbon price is the most critical signal needed to start closing the economic gap with coal.

- These market conditions could be happening simultaneously: cement producers in regions without strong subsidies may increasingly favor lower-CAPEX decarbonization options. This includes expanding the use of alternative fuels like RDF or installing mature technologies like SNCR for NOx compliance, pushing major decisions on hydrogen retrofits beyond 2030.

The questions your competitors are already asking

This report covers one angle of the transition from technical validation to subsidized pilot projects for hydrogen in cement production. The questions that matter most depend on your work.

- Heidelberg Materials’ activities in hydrogen. Is the burner technology progressing from asphalt pilots to full cement kiln deployment?

- What is the outlook for commercial-scale hydrogen burner deployment in cement kilns by 2026, considering the 10x fuel cost gap vs. coal?

- What is the cost breakdown of a cement kiln burner retrofit for 100% hydrogen combustion?

- Which cement producers are adopting hydrogen in pilot projects, and what is the scale of their decarbonization funding?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.