Geological Hydrogen Exploration, $403 M Koloma Fund, Hy Terra’s Oman Mo U, and 5 Pilot Projects (2021 to 2026)

5+ Exploration Projects, Geological Hydrogen Moves From Theory to Commercial Pilots

The geological hydrogen sector has decisively shifted from theoretical discussions to active, funded exploration and appraisal, but high commercial risk persists. Before 2025, the industry’s focus was largely on academic studies and analyzing historical anomalies like the continuously producing well in Bourakébougou, Mali. The period from 2025 to 2026 is now defined by tangible commercial actions, including confirmed discoveries and preparations for production tests that will determine economic viability.

- Prior to 2025, commercial activity was minimal, with the sector defined more by geological modeling and scientific papers than by active drilling campaigns. The Mali well served as a proof-of-concept but was widely seen as a geological outlier rather than a scalable model for a new energy resource.

- The turning point occurred in January 2026, when MAX Power Mining Corp. confirmed Canada’s first natural hydrogen drilling discovery at its Lawson project, moving the concept from “verified subsurface reality.” This event validated modern exploration theses in a new geography.

- Momentum is building toward commercial validation with Hy Terra scheduling production testing at its Mc Coy 1 well in Kansas for Q 2 2026. This test is a critical milestone for the entire industry, as it aims to provide the first public data on sustained flow rates from a purpose-drilled hydrogen well in the U.S.

- The range of commercial applications is also broadening beyond passive exploration. In February 2026, Vema Hydrogen completed drilling pilot wells for its Engineered Mineral Hydrogen (EMH) project in Quebec, a novel approach designed to stimulate hydrogen generation in-situ.

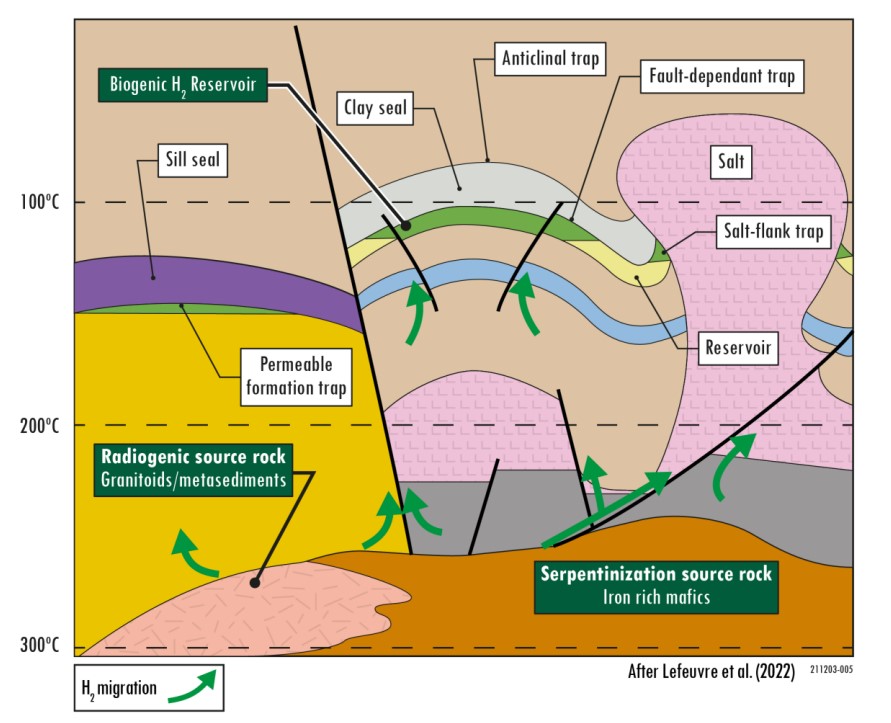

Geological Models Guide Hydrogen Exploration

This section describes the industry’s shift from theory to active exploration. The chart shows the geological model—source, migration, and trap—that forms the theoretical basis for these new exploration projects.

(Source: Getech)

Koloma $403 M Funding, Geological Hydrogen Investment Signals Market Validation (2025 to 2026)

A significant influx of venture and public capital in 2026 validates geological hydrogen as a tangible asset class, attracting both high-risk private funds and strategic government support. This financial backing is a crucial enabler, funding the high-cost drilling and technology development required to move from discovery to production. The mix of private and public funding indicates growing confidence in the resource’s potential to become a disruptive, low-cost energy source.

- The most significant signal of private sector confidence is the $403 million raised by Koloma, a prominent U.S. startup, from investors including Khosla Ventures, ASTUTIA Ventures, and Prelude Ventures. This level of funding for an early-stage exploration company underscores strong belief in the commercial potential.

- Public funding is also materializing to de-risk key technologies. The European Union awarded technology firm Mantle 8 €2.06 million in March 2026 to advance its systems for detecting and modeling natural hydrogen resources in Europe.

- Regional governments are creating direct financial incentives to spur exploration. In February 2026, Australia’s Northern Territory Government opened a new round of its Geophysics and Drilling Collaborations program, offering co-funding grants between $50, 000 and $200, 000.

Table: Geological Hydrogen Sector Investments (2026)

| Company / Entity | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Koloma | Q 2 2026 | Raised $403 million from investors including Khosla Ventures and Prelude Ventures to fund exploration and technology development, establishing it as the most well-funded startup in the sector. | Tracxn |

| Mantle 8 | Mar 2026 | Secured a €2.06 million grant from the European Union to advance its proprietary technologies for detecting and modeling natural hydrogen resources, based in Grenoble, France. | Innovation News Network |

| Australian Exploration Companies | Feb 2026 | Eligible for grants of $50, 000 to $200, 000 from the Northern Territory Government’s GDC program to co-fund exploration activities, de-risking early-stage prospecting for hydrogen and other critical minerals. | NT Government |

Exploration Alliances, Hy Terra and ARA Natural Resources Target Oman Geology

Strategic partnerships are forming to combine regional geological expertise with specialized exploration technologies, accelerating the global search for viable hydrogen deposits. This collaborative model is essential for navigating diverse regulatory environments and de-risking entry into new territories. These alliances pool capital and knowledge to tackle the high upfront costs and geological uncertainties inherent in this nascent industry.

- In March 2026, Australian explorer Hy Terra signed an 18-month exclusive Memorandum of Understanding (Mo U) with ARA Natural Resources to jointly evaluate geologic hydrogen opportunities in Oman, a region known for its favorable ophiolite formations.

- This partnership is a prime example of a critical strategy: it combines ARA’s deep in-country geological knowledge with Hy Terra’s specialized focus on natural hydrogen exploration techniques and technologies.

- Governments are also facilitating partnerships through structured bid rounds. The Philippines Department of Energy awarded two service contracts in January 2026 in the world’s first competitive tender for native hydrogen, formalizing collaboration between the state and private explorers.

Table: Geological Hydrogen Partnerships (2026)

| Partners | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Hy Terra & ARA Natural Resources | Mar 2026 | Signed an 18-month exclusive Mo U to jointly evaluate and pursue geologic hydrogen opportunities in Oman. The alliance leverages ARA’s regional expertise and Hy Terra’s hydrogen exploration focus. | Fuel Cells Works |

| Philippine Government & Private Bidders | Jan 2026 | The Department of Energy awarded two native hydrogen exploration service contracts in the Philippines, marking the conclusion of the world’s first competitive bid round for the resource. | Department of Energy PH |

North America vs. Global, Geological Hydrogen Exploration Hotspots Emerge

While early interest in geological hydrogen was diffuse, by 2026 North America and Australia have emerged as the primary hubs for drilling, investment, and policy development. This geographic concentration is driven by a combination of promising geological formations, existing oil and gas expertise, and proactive government initiatives aimed at capturing a first-mover advantage.

USGS Map Shows US Hydrogen Prospectivity

The section identifies North America as an emerging hub for geological hydrogen. This USGS map visually confirms high prospectivity across the US, explaining why the region is a hotspot for investment and policy development.

(Source: USGS.gov)

- Between 2021 and 2024, the global focus was limited, often referencing the single producing well in Mali, Africa, as the main real-world example and lacking a clear geographic center for new investment.

- From 2025, North America became the center of tangible activity. MAX Power Mining Corp. made its discovery in Saskatchewan, Canada, while Hy Terra advanced its project in Kansas, USA. This was bolstered by U.S. Geological Survey (USGS) maps confirming high prospectivity in the American Midwest and along the East Coast.

- U.S. state governments are actively encouraging development. In January 2026, Michigan’s Governor signed Executive Directive 2026-1, creating a formal initiative to prepare the state’s regulatory and economic framework for geological hydrogen exploration.

- Australia is another key region, with explorers like Prominence Energy and Gold Hydrogen actively pursuing projects, supported by government co-funding programs like the Northern Territory’s Geophysics and Drilling Collaborations (GDC).

- The geographic scope is now expanding, with companies like H 2 Au pursuing licenses in South Africa and Hy Terra entering Oman, signaling a broadening search for the world’s most promising geological plays.

1, 000 x Production Increase, Element One Catalyst Technology Nears Validation

The technology for geological hydrogen is maturing rapidly from passive discovery to active stimulation, with new catalysts and engineered systems designed to enhance in-situ production, though scaled extraction remains unproven. While conventional oil and gas technology is sufficient for initial exploration, innovators are developing solutions to either improve recovery from natural reservoirs or create hydrogen underground on demand.

- From 2021 to 2024, the dominant technology was the adaptation of conventional oil and gas methods, including seismic analysis and standard drilling rigs, to search for and characterize hydrogen seeps and accumulations.

- By 2026, the technology has bifurcated. Passive exploration, using existing methods, was validated by MAX Power’s drilling discovery. The next hurdle is proving these wells can sustain economic flow rates.

- Active stimulation technologies are advancing in parallel. In April 2026, Element One announced its patent-pending, nickel-doped spinel catalysts increased hydrogen production by over 1, 000 times compared to natural processes in laboratory settings, enabling real-time, in-situ generation.

- Another novel approach, Engineered Mineral Hydrogen (EMH), is being field-tested. Vema Hydrogen completed drilling its first pilot wells in Quebec in February 2026 to demonstrate its method for engineering subsurface conditions to produce clean hydrogen.

SWOT Analysis, Geological Hydrogen Strengths and Commercialization Hurdles

Geological hydrogen’s primary strength is its disruptive cost potential, which could fundamentally reset the clean hydrogen market. However, this is counterbalanced by significant exploration risks, technological uncertainties, and a lack of established regulatory frameworks, which are only beginning to be addressed in 2026.

- The key strength is a projected production cost as low as $0.50 per kg, an order of magnitude cheaper than both established green hydrogen and blue hydrogen pathways.

- The primary weakness remains the high upfront risk and cost of exploration drilling, with no guarantee that a discovery will translate into a commercially viable producing asset.

- The opportunity is immense, with a potential multi-trillion-ton global resource identified by the USGS and access to a rapidly growing global hydrogen market projected to exceed $200 billion by 2033.

- A major threat comes from the long lead times required for exploration and appraisal, which could allow competitors in the U.S. hydrogen hubs and other government-backed programs to solidify infrastructure and offtake agreements first.

Table: SWOT Analysis for Geological Hydrogen

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Theoretical low-cost potential based on the Mali well and geological models. Seen as a potential renewable resource (continuous generation). | Projected production costs of $0.50-$1.50/kg are substantiated by drilling data. MAX Power’s discovery confirms resource existence outside of historical anomalies. | The resource is now a verified asset class, not just a geological theory. The low-cost potential is the primary driver of investment. |

| Weaknesses | Extremely high exploration risk. Lack of proven exploration techniques. Resource size and accessibility were entirely unknown. | Exploration risk remains high, but is now better understood. The key uncertainty has shifted from “if it exists” to “can it be produced economically.” Lack of flow rate data. | The core weakness shifted from geological uncertainty to commercial and engineering uncertainty. The problem is now one of extraction, not just discovery. |

| Opportunities | Potential to disrupt the hydrogen market if found at scale. Growing global demand for clean hydrogen. | Venture capital firms (Koloma’s $403 M) and public funders (EU grant for Mantle 8) are now actively investing. Governments (Michigan, Philippines) are creating regulatory frameworks. | The market has validated the opportunity with significant capital and policy support, creating a clear pathway for explorers to secure funding and licenses. |

| Threats | Perceived as a fringe or niche resource. Competition from rapidly scaling green and blue hydrogen projects. | Regulatory vacuum persists in many jurisdictions, slowing development. Long lead times for exploration may cede market share to more mature technologies. | The main threat is now timing. The sector must prove commerciality quickly before long-term infrastructure and supply chains for green/blue hydrogen become entrenched. |

Hy Terra Mc Coy 1 Test, A Key Commercial Signal for Geological Hydrogen in 2026

The single most critical event for the geological hydrogen sector in 2026 is the result of Hy Terra’s Mc Coy 1 production test. A successful outcome will trigger a significant increase in investment and exploration, while a failure will reinforce its perception as a high-risk, niche resource that is not yet ready for commercial scale.

Hydrogen Productivity Lags Commercial Demand

This section focuses on the importance of the McCoy 1 test for proving commercial viability. This chart perfectly frames the issue by showing the immense gap between current well productivity and large-scale industrial demand that the test must overcome.

(Source: LinkedIn)

- If the Mc Coy 1 well demonstrates sustained, commercially viable flow rates, watch for a rapid acceleration of investment into junior explorers and the potential entry of major energy companies that have been observing from the sidelines.

- This could also be happening: a successful test would pressure governments in jurisdictions with favorable geology, such as Iowa, Michigan, and parts of Australia, to fast-track regulatory frameworks to attract and retain capital.

- Conversely, if the test shows low or declining flow rates, watch for a pullback in venture funding for passive exploration and a strategic pivot toward “stimulated” or “engineered” hydrogen technologies, like those pursued by Vema Hydrogen and Element One.

- Underwhelming results would also likely cede momentum back to established clean hydrogen pathways, such as the large-scale green hydrogen electrolyzer projects being developed by firms like Sunfire and the massive infrastructure investments planned by companies like Air Products.

The questions your competitors are already asking

This report covers one angle of geological hydrogen’s shift from theory to commercial validation. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the geological hydrogen exploration market?

- What is the outlook for geological hydrogen commercial production by 2026?

- Geological hydrogen well performance and flow rates. What are the key technical risks to commercial viability?

- What is actually happening with HyTerra’s Mc Coy 1 well since the production test announcement?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.