Green Hydrogen Distribution Bottleneck, $701 M Tube Trailer Market, 400 km Oman Pipeline, and Multiple EU Projects Face Delays (2025 to 2026)

The global push for a hydrogen economy has reached a critical imbalance in 2026. While innovation in production technologies from firms like Sunfire and Siemens Energy accelerates, the midstream segment of storage and distribution is failing to keep pace. This creates a significant bottleneck that jeopardizes national net-zero ambitions and billions in clean energy investments. The hydrogen logistics network remains fragmented and reliant on stop-gap measures, highlighting a stark mismatch between production potential and the physical reality of moving molecules. This analysis examines the state of hydrogen distribution, focusing on the roles of tube trailers and pipelines and the infrastructure gap that has become the hydrogen economy’s most pressing challenge.

Distribution Bottleneck Risks, Hydrogen Projects Face Delays from Underdeveloped Infrastructure

The hydrogen industry’s rapid expansion in production is dangerously outpacing the development of essential distribution infrastructure, creating a systemic bottleneck that threatens project viability and climate targets. While the 2021 to 2024 period was defined by pilot projects and production announcements, the 2025 to 2026 period is defined by a logistical crisis as large-scale facilities come online without a clear, cost-effective path to market.

- Research from Heriot-Watt University finds that hydrogen transport infrastructure is advancing at only half the pace of technologies like electrolysis and fuel cells, putting billions of dollars in clean energy projects at risk.

- The sector has become heavily dependent on compressed gas tube trailers as a default distribution method, a solution that is economically and logistically unsustainable for the industrial-scale demand now emerging.

- For example, one analysis estimates that servicing a single large industrial facility would require 325 tube trailer deliveries per day, a logistical impossibility that underscores the need for pipelines.

- This systemic failure threatens the business case for major producers like Air Products and component manufacturers such as Cummins, whose projects rely on the offtake from large industrial users that require reliable, high-volume supply.

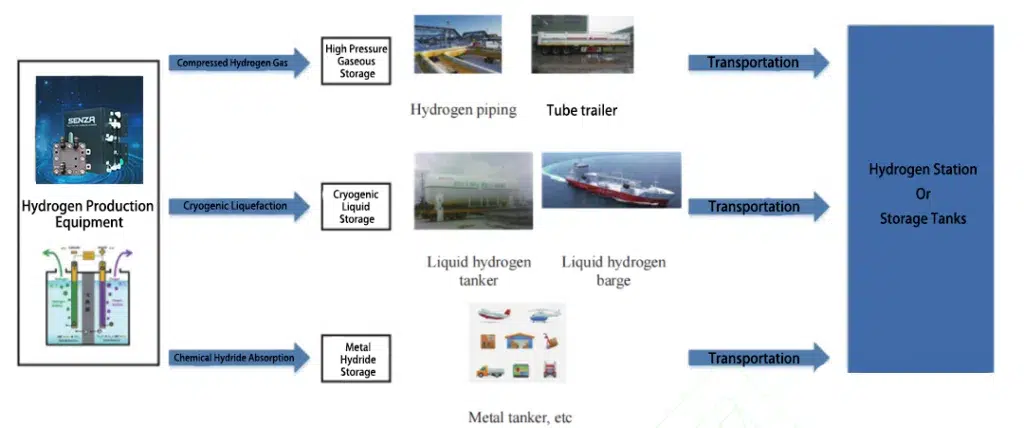

Visualizing Hydrogen’s Distribution Pathways

This flowchart illustrates the various paths hydrogen takes from production to market, providing context for the distribution bottlenecks and infrastructure gaps discussed in the article.

(Source: SENZA)

$24 B by 2026, Hydrogen Transport Investment Fails to Match Explosive Market Growth

Despite projections for the hydrogen storage and transport market to grow fivefold by 2035, current investment levels in physical pipeline infrastructure are insufficient to prevent near-term bottlenecks, creating a classic “chicken-and-egg” dilemma. Capital for high-cost pipelines is stalled by a lack of guaranteed offtake, which in turn is stalled by the absence of reliable, low-cost transport, a situation that may lead to more large-scale project cancellations like the one seen by Cummins and Topsoe.

Liquid Hydrogen Transport Market to Double

This forecast supports the article’s point about explosive growth, projecting the liquid hydrogen transport market to grow from $20.2 billion in 2026 to $43 billion by 2035.

(Source: Global Market Insights)

- The global hydrogen storage and transportation market is projected to expand from USD 24.36 billion in 2026 to USD 128.85 billion by 2035, representing a compound annual growth rate (CAGR) of 20.1%.

- In contrast, the more immediate, lower-CAPEX tube trailer market is seeing modest growth, projected to expand at a 7.5% CAGR to reach US$ 701.1 million by 2033, reflecting the market’s current reliance on small-scale distribution.

- This investment gap is creating skepticism among financial institutions, with Europe’s economic councils expressing concerns about the widespread use of hydrogen, which adds policy uncertainty and chills private investment in long-term infrastructure.

Table: Hydrogen Market Growth Projections (2026-2035)

| Forecast Provider | Market Segment | 2026 Value ($B) | Forecast Horizon Value ($B) | Forecast Year | CAGR (%) | Source |

|---|---|---|---|---|---|---|

| Market Growth Reports | Hydrogen Storage & Transportation | $24.36 | $128.85 | 2035 | 20.1% | Market Growth Reports |

| Persistence Market Research | Hydrogen Storage | $2.9 | $11.7 | 2033 | 22.9% | Persistence Market Research |

| Persistence Market Research | Hydrogen Tube Trailer | $0.425 | $0.701 | 2033 | 7.5% | Persistence Market Research |

Europe vs. Central Asia, Hydrogen Infrastructure Gaps Threaten Regional Ambitions

While Europe is advancing flagship “hydrogen backbone” projects, regional disparities in infrastructure readiness are becoming stark, with areas like Central Asia facing compounded challenges that threaten their development plans. The period of 2025-2026 marks a difficult transition from strategic planning to physical execution, revealing which regions have the policy and capital to build versus those with stalled ambitions.

German Hydrogen Backbone Faces Overcapacity Risk

This graphic highlights the regional infrastructure gap, showing Germany’s hydrogen backbone capacity could be 20-40 times greater than actual demand, illustrating the execution challenges facing Europe.

(Source: CleanTechnica)

- In Europe, Germany is moving forward with its national “hydrogen backbone, ” and the EU is reforming grid rules to support cross-border energy projects connecting Nordic production with German industrial demand from users like steelmaker SSAB.

- However, in Central Asia, a March 2026 report from S&P Global identifies infrastructure gaps and water scarcity as the primary threats to the region’s hydrogen development plans.

- The Middle East is showing progress, with Oman planning a 400-kilometer pipeline network to connect green hydrogen production sites with industrial consumers and export terminals.

- This geographic fragmentation creates significant risk, as the viability of industrial decarbonization projects, such as those in the cement sector involving firms like Akmenės cementas, depends entirely on access to reliable and affordable hydrogen.

Pipeline vs. Trailer Maturity, Hydrogen Distribution Faces A Scalability Mismatch

In 2026, hydrogen distribution technology is split between mature but unscalable tube trailers and scalable but commercially underdeveloped pipelines, creating a critical maturity gap. This mismatch is the primary technical bottleneck throttling the growth of the entire hydrogen value chain, impacting everything from electrolyzer manufacturers like ITM Power to end users.

Pipelines vs. Trailers: A Transport Dilemma

This analysis visualizes the article’s core argument about a scalability mismatch, showing that pipelines are cost-effective for high demand while trailers are suited for lower, localized demand.

(Source: ScienceDirect.com)

- Tube trailers are a fully commercialized technology, with standard models carrying 300-500 kg of hydrogen at 2, 400 psi. While they were sufficient for early pilots (2021-2024), they are logistically and economically unviable for the industrial-scale projects emerging now, being most effective only for distances under 300 km.

- Advanced trailers with higher pressures (up to 6, 500 psi) and capacities (up to 1, 244 kg) exist but do not solve the fundamental problem of low storage density and the need for massive truck fleets at scale.

- Pipelines are the only technologically mature solution for transporting vast quantities of hydrogen efficiently but remain commercially immature due to extremely high upfront capital expenditure and long development timelines.

- A hybrid model is emerging as the most pragmatic approach, using pipelines for high-volume “backbone” transport and trailers for flexible last-mile delivery, but this integrated system is still in its infancy.

Hydrogen Distribution SWOT, Strengths in Flexibility vs. Weakness in Scalability (2026)

The strategic analysis for hydrogen distribution in 2026 reveals a system whose primary strength in flexibility is overshadowed by a critical weakness in scalability. The industry is threatened by policy uncertainty and a persistent investment deadlock, with its greatest opportunity lying in repurposing existing infrastructure and aggressive government de-risking actions.

- Strengths: The primary strength is the operational flexibility of the existing tube trailer fleet, which allows for market seeding and servicing of dispersed, low-volume customers.

- Weaknesses: The central weakness is the stark mismatch between production ambitions and distribution capacity, leading to a logistical bottleneck that inflates costs and jeopardizes large projects.

- Opportunities: Key opportunities include repurposing natural gas pipelines for hydrogen, developing integrated multimodal hubs at ports, and public-private partnerships to scale up higher-capacity mobile solutions like liquid hydrogen.

- Threats: The main threat is the “chicken-and-egg” investment dilemma, where private capital remains on the sidelines, a risk compounded by wavering policy support from key economic institutions.

Table: SWOT Analysis for Hydrogen Distribution (2026)

| SWOT Category | Key Factor | Supporting Evidence (2026) | Source |

|---|---|---|---|

| Strengths | Flexibility for Early Markets | Tube trailers are commercially available, serving small-volume industrial and transport sites. Protium operates a fleet at 350 bar for last-mile delivery. | Protium |

| Weaknesses | Lack of Scalability and High OPEX | Supplying a large facility requires an unsustainable fleet of trucks. Transport infrastructure is developing at half the pace of production technology. | Heriot-Watt University |

| Opportunities | Infrastructure Repurposing and De-Risking | The EU is reforming grid policies to support hydrogen infrastructure, and Germany is pursuing a “hydrogen backbone, ” much of it based on repurposed gas lines. | Invest in Denmark |

| Threats | Investment Deadlock and Policy Uncertainty | High CAPEX for pipelines cannot be justified without offtake guarantees, but users are hesitant without low-cost delivery. European economic bodies express skepticism. | Clean Technica |

2027 Outlook, Hydrogen Transport Requires Aggressive De-Risking to Avoid Stagnation

If governments and regulators fail to implement aggressive de-risking mechanisms for backbone pipeline projects in the next 12-18 months, the hydrogen economy faces a high probability of stagnation. This scenario would be characterized by stranded production assets, canceled projects, and a fragmented, high-cost distribution market that fails to achieve climate goals.

Hydrogen Tube Trailer Market Sees Growth

This chart supports the SWOT analysis’s “Strength” of flexibility by showing the market for hydrogen tube trailers, a mature technology, is projected for steady growth through 2026.

(Source: Fairfield Market Research)

- If this happens: Governments implement aggressive de-risking policies like transport-focused Contracts for Difference (Cf Ds) and long-term revenue guarantees for pipeline operators. Watch this: A significant increase in Final Investment Decisions (FIDs) for major pipeline corridors and a corresponding rise in long-term offtake agreements from industrial users. This could be happening: The distribution bottleneck begins to resolve post-2028, unlocking private capital and enabling large-scale industrial decarbonization, benefiting offtakers in sectors like mobility who rely on partners like Forvia.

- If this happens: The market-led investment approach continues without significant policy intervention. Watch this: Continued investment flowing only into the tube trailer market and small, localized hydrogen loops, while major production facilities are forced to delay commissioning or operate below capacity. This could be happening: The bottleneck becomes a permanent structural weakness, leading to investor flight and a failure to meet 2030 decarbonization targets.

- If this happens: Investment pivots to advanced mobile solutions as a medium-term bridge. Watch this: Accelerated funding for liquid hydrogen (LH 2) and ammonia transport infrastructure, along with higher-capacity (1, 000+ kg) tube trailers. This could be happening: An interim solution emerges, buying time for pipeline construction but cementing a higher operational cost for delivered hydrogen for the next 5-10 years.

The questions your competitors are already asking

This report covers one angle of the growing bottleneck in hydrogen storage and distribution. The questions that matter most depend on your work.

- What is actually happening with the 400 km Oman hydrogen pipeline and other delayed EU projects?

- How do hydrogen pipelines compare to tube trailers for cost and scalability in addressing the distribution bottleneck?

- What are the opportunities for infrastructure and logistics companies in the $701M hydrogen tube trailer market?

- Which companies are gaining or losing ground in the hydrogen tube trailer market?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.