EU CBAM 2026: €9 B Revenue Forecast, 10% Article 6 Credit Cap, and Growing Carbon Software Market (2021 to 2026)

CBAM Financial Risks: €50/Tonne Penalties and EU ETS Price Exposure

The transition from a reporting-only exercise to a full financial obligation on January 1, 2026, coupled with the May 2026 draft rules, has crystallized the Carbon Border Adjustment Mechanism (CBAM) from a theoretical risk into a tangible cost, exposing importers to direct EU ETS price volatility and steep non-compliance penalties.

- From October 1, 2023, to December 31, 2025, businesses operated under a transitional phase requiring only quarterly emissions reporting, with penalties for non-submission ranging from €10 to €50 per tonne. The definitive phase, which began in 2026, now requires importers to purchase and surrender CBAM certificates, with the first financial settlement in 2027 covering 2026 imports.

- This creates direct financial exposure to the EU’s Emissions Trading System (EU ETS). The first official CBAM certificate price for Q 1 2026 was set at €75.36 per tonne of CO 2. Analyst forecasts project this to rise, with a Reuters survey predicting an average of €80.61/tonne in 2026 and €93.29/tonne in 2027, exposing businesses to significant and volatile costs.

- The May 13, 2026, draft rules provided the first detailed framework for reducing this liability by claiming credit for carbon prices paid in a third country. However, the rules also introduced a critical limitation: the use of international credits generated under Article 6 of the Paris Agreement is capped at 10% of an importer’s total obligation, restricting the use of offsets and reinforcing the primacy of direct carbon pricing.

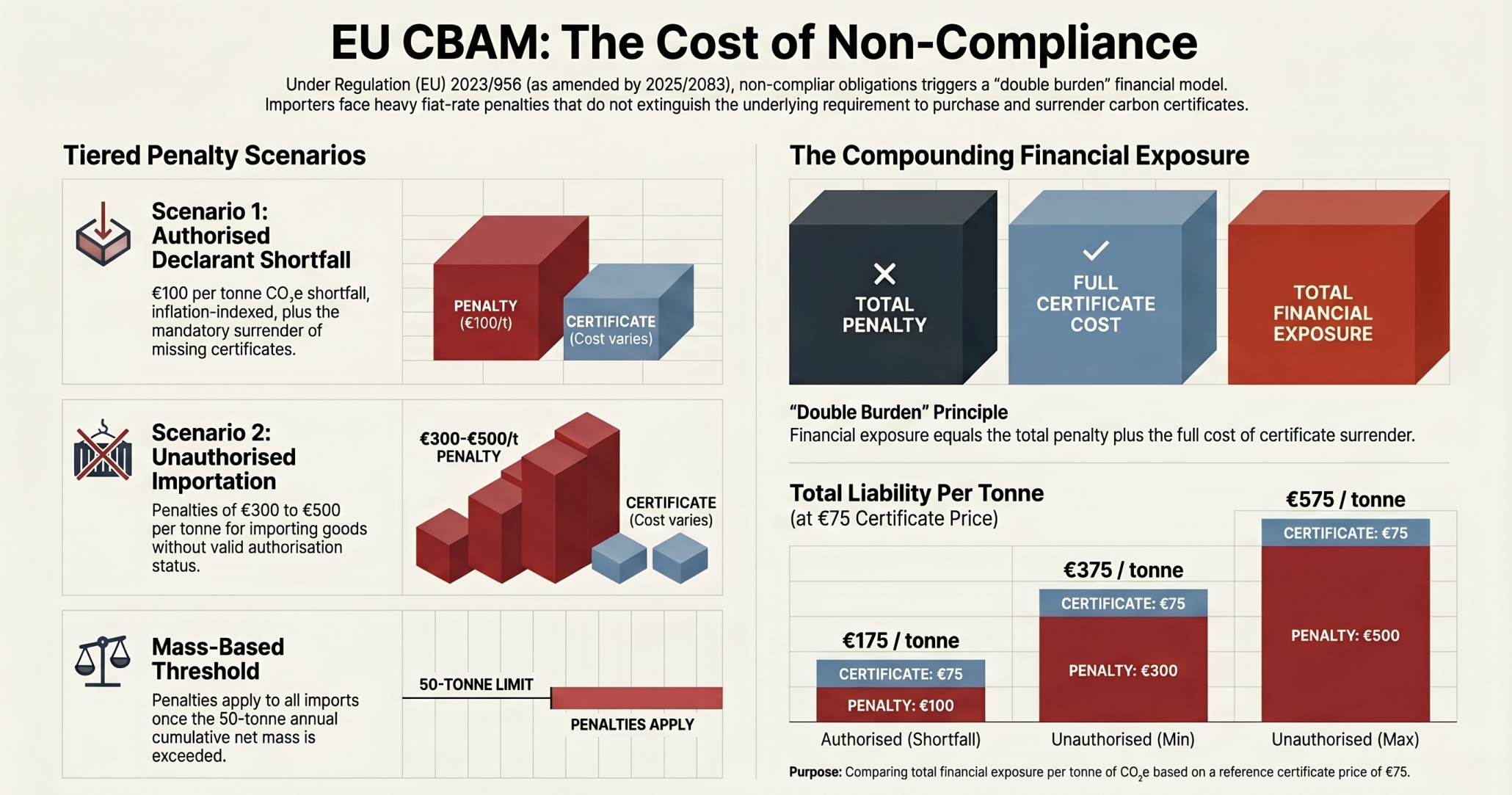

CBAM Non-Compliance Costs Can Exceed €500/Tonne

The section discusses the financial risks of CBAM, specifically mentioning penalties. The chart visually reinforces this by quantifying the high cost of non-compliance, directly aligning with the section’s theme of financial penalties and risk.

(Source: CBAM Journal)

$29 B Carbon Software Market, Precedence Research Forecasts on CBAM Compliance

The immense complexity of CBAM’s Monitoring, Reporting, and Verification (MRV) requirements has ignited a high-growth market for carbon accounting software and advisory services, turning a regulatory burden into a significant commercial opportunity for specialized providers.

- The global carbon accounting software market is experiencing rapid growth directly attributable to regulations like the CBAM. One forecast valued the market at $14.57 billion in 2025 with projections to reach $109.16 billion by 2035.

- Another analysis from Global Growth Insights is even more aggressive, placing the market at $29.3 billion in 2026 and forecasting growth to $233.9 billion by 2035, reflecting a compound annual growth rate of 26%.

- This demand stems from the complex data management obligations placed on EU importers. They are responsible for collecting and verifying embedded emissions data from global suppliers and ensuring its accuracy for accredited verifiers, making specialized software essential for minimizing financial and legal risks.

Infographic Details CBAM Risks and Compliance for Exporters

The section describes the emergence of a large carbon software market driven by CBAM. The infographic, by detailing the complexities of CBAM compliance and associated risks, illustrates why specialized software is becoming essential for exporters, thereby justifying the market growth discussed in the section.

(Source: LinkedIn)

Table: Carbon Accounting & Management Software Market Forecasts

| Forecast Provider | 2025/2026 Market Size ($B) | 2034/2035 Forecast ($B) | CAGR (%) | Source |

|---|---|---|---|---|

| Precedence Research | $14.57 B (2025) | $109.16 B (2035) | 25.1% | Precedence Research |

| Global Growth Insights | $29.3 B (2026) | $233.9 B (2035) | 26.0% | Global Growth Insights |

| Polaris Market Research (Carbon Footprint Management) | $11.6 B (2025) | $20.35 B (2034) | 7.0% | Polaris Market Research |

EU Carbon Price Towers Over Global Peers

The section is a table forecasting the carbon accounting software market. This chart explains the primary driver for this market: the significantly high EU carbon price makes precise carbon accounting a financial necessity for affected companies, thus creating demand for management software.

(Source: CSIS)

Global Impact of CBAM: India and Vietnam Race to Adapt to EU Rules

The CBAM crediting mechanism is actively reshaping global trade dynamics, creating a clear divergence between countries proactively implementing domestic carbon pricing to retain revenue and those facing significant economic risk from unmitigated export costs.

- During the 2021-2024 preparatory phase, most countries remained in a “wait-and-see” mode. The start of the definitive period in 2026 has spurred immediate action, with countries like Malaysia (planning a 2026 carbon tax) and Vietnam (piloting an ETS in 2025) accelerating plans to establish creditable carbon pricing systems to avoid ceding revenue to the EU.

- In contrast, major exporters without robust carbon pricing face substantial financial exposure. A study estimated the potential annual CBAM levy on India could be as high as $469 million for iron and steel alone. The African Development Bank estimates the total cost of CBAM to Africa could reach $25 billion annually.

- This creates a supplier concentration risk for EU importers, who are now financially incentivized to source from nations with established, EU-recognized carbon pricing schemes. This simplifies compliance and reduces the cost of CBAM certificates, potentially altering global supply chains for covered goods like steel, aluminum, and fertilizers.

CBAM Rule Maturity: From Vague Concept to Draft Implementing Rules (2021-2026)

The CBAM regulatory framework has matured from a high-level political concept in the 2021-2024 period to a detailed, operational mechanism with the May 2026 publication of draft implementing rules, providing the first concrete guidance on financially material aspects like third-country credit deductions.

- Between 2021 and 2024, businesses operated with high-level principles from the initial CBAM regulation, focusing primarily on understanding the upcoming reporting requirements of the transitional phase. Key questions around how, and if, foreign carbon prices would be credited remained largely unanswered, creating strategic uncertainty.

- The publication of draft rules on May 13, 2026, marked a critical maturation point. For the first time, the market received specific guidance on eligible carbon prices (e.g., explicit taxes, ETS allowances), the potential use of carbon credits, and critical limitations, most notably the 10% cap on Article 6 credits.

- This shift moves the challenge from strategic ambiguity to tactical execution. Companies must now build compliance systems based on these detailed, though still draft, technical rules for verification, reporting, and financial settlement, which begins in 2027 for the 2026 import year.

CBAM Implementation Timeline Visualized

The section heading explicitly mentions the timeline and maturation of CBAM rules from 2021 to 2026. The chart is a direct and perfect visualization of this implementation timeline, making it an ideal match.

(Source: Senken)

SWOT Analysis: EU CBAM’s Impact on Global Trade and Carbon Markets

The maturation of CBAM into a financially binding instrument presents a dual-edged sword, creating clear opportunities for low-carbon producers and carbon management service providers while posing significant compliance and trade-related threats.

- The framework’s primary strength lies in its potential to level the playing field on carbon costs and drive global decarbonization, but this is matched by a weakness in its inherent complexity and administrative burden.

- Opportunities for competitive advantage for low-carbon producers and the burgeoning carbon software market are significant. However, these are tempered by the threat of trade friction and financial risks associated with data integrity and price volatility.

Table: SWOT Analysis for EU Carbon Border Adjustment Mechanism

| SWOT Category | 2021 – 2024 (Transitional Phase Prep) | 2025 – 2026 (Definitive Phase Launch) | What Changed / Validated |

|---|---|---|---|

| Strengths | Theoretical framework to prevent carbon leakage and level the playing field for EU producers. | Mechanism becomes operational, directly linking import costs to EU ETS price. Drives incentive for non-EU decarbonization. | The financial incentive for decarbonization is now a real, quantifiable cost (€75.36/tonne in Q 1 2026) rather than a future concept. |

| Weaknesses | High uncertainty regarding implementation details, especially crediting of foreign carbon prices. Administrative burden seen as a future cost. | Extreme compliance complexity becomes clear. MRV requirements for third-country data create significant administrative costs and data verification challenges. | The draft rules of May 2026 confirmed the high bar for data verification, adding layers of cost for accredited verifiers and increasing risk for importers. |

| Opportunities | Speculation about a future market for carbon advisory and software services. Low-carbon producers anticipated a future advantage. | Carbon accounting software market booms, with forecasts projecting a $29.3 B market in 2026. Low-carbon producers gain a direct, measurable price advantage in the EU market. | The start of the definitive phase validated the business case for carbon management services and decarbonization investments, shifting them from ESG goals to financial necessities. |

| Threats | Concerns from trading partners about potential “green protectionism” and WTO compliance. Risk of trade disputes was theoretical. | Increased risk of trade friction and retaliatory tariffs as financial impacts become real. Data fraud and use of dubious credits (as seen in past schemes) become a tangible risk for importers facing penalties. | The financial stakes are now high enough (e.g., $25 B potential cost to Africa) to make trade disputes a more probable outcome, and the reliance on third-party data makes fraud a key compliance risk. |

Charts Show CBAM’s Impact on EU and Partner Trade

This section is a table-based SWOT analysis. The selected chart, which illustrates the broader trade impacts on both the EU and its partners, provides the high-level data and context that would be detailed and categorized within the SWOT table.

2027 CBAM Scenario: 10% Credit Cap and EU ETS Price Volatility

Moving into 2027, the primary variables dictating CBAM’s financial impact will be the final interpretation of credit eligibility in the implementing acts and the persistent volatility of the EU ETS price, forcing importers to adopt sophisticated hedging and supply chain strategies.

- If the final rules, expected after the June 10, 2026, feedback period, maintain the strict 10% cap on international credits and impose stringent quality criteria, watch for importers to aggressively rationalize supply chains, prioritizing suppliers in countries with direct carbon taxes or linked ETS schemes over those reliant on offsets.

- The EU ETS price, which directly sets the CBAM certificate cost, remains a major uncertainty. With analyst forecasts for 2027 ranging up to €93.29/tonne and longer-term projections from sources like Enerdata and Bloomberg NEF exceeding €130/tonne by 2030, the need for financial hedging instruments for CBAM obligations is becoming critical.

- A key signal to monitor is how the EU Commission addresses “double claiming, ” where exporters receive a rebate for a domestic carbon price. The draft rules state any such rebate must be subtracted, but enforcing this across myriad global schemes will be a major challenge and a source of potential disputes.

CBAM Costs Increase Significantly After 2026

The section discusses a future CBAM scenario in 2027, focusing on new rules and price volatility. The chart directly supports this by showing a significant increase in costs after 2026, which is when the definitive period of CBAM begins.

(Source: carboneer)

The questions your competitors are already asking

This report covers one angle of the financial and compliance strategies for navigating the EU’s Carbon Border Adjustment Mechanism (CBAM). The questions that matter most depend on your work.

- What is the price outlook for EU ETS allowances and CBAM certificates through 2027?

- How does claiming credit for a third-country carbon price compare to using Article 6 offsets for reducing an importer’s total CBAM obligation?

- Which companies are gaining or losing ground in the carbon accounting software market for CBAM compliance?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.