Shell LNG Strategy, 12 MTPA Expansion, PETRONAS Joint Venture, and 2 Major Offtake Agreements (2021 to 2025)

LNG Market Risks, Shell Confronts 200 MTPA Supply Wave and EU Methane Rules

In 2025, Shell aggressively cemented its strategy to dominate the global Liquefied Natural Gas (LNG) market, but this expansion confronts immediate and significant market and regulatory headwinds. While the company’s bullish forecast for a 60% surge in LNG demand by 2040 underpins its growth plans, it is simultaneously preparing to navigate a period of market oversupply and heightened regulatory pressure that crystallized during the year.

- In 2025, Shell committed to expanding its LNG capacity by up to 12 million metric tonnes by 2030 and achieved a major operational milestone with the first cargo shipped from the LNG Canada project in June 2025. This contrasts with the 2021-2024 period, which was defined by securing European energy supply post-Ukraine and benefiting from high commodity prices.

- The primary market threat is an impending supply glut. Forecasts from multiple agencies, including the IEA and J.P. Morgan, indicate that between 170 MTPA and 257 MTPA of new liquefaction capacity will come online by 2030, primarily from the US and Qatar. This wave is expected to create an oversupplied market and suppress prices from 2026 to 2030.

- Regulatory risk intensified in 2025 with the approaching implementation of the EU Methane Regulation. Starting in 2027, the rules impose stringent monitoring and reporting standards on gas importers, posing a significant compliance and cost challenge for suppliers. Intense lobbying from the U.S. during 2025 has led the European Commission to consider “flexibilities, ” but the final rules remain a key uncertainty.

- Shell’s strategic pivot toward fossil fuels attracted significant investor scrutiny. A shareholder resolution filed in January 2025 explicitly challenged the “disconnect” between the company’s LNG growth ambitions and its net-zero climate commitments, highlighting a growing risk to its social license to operate.

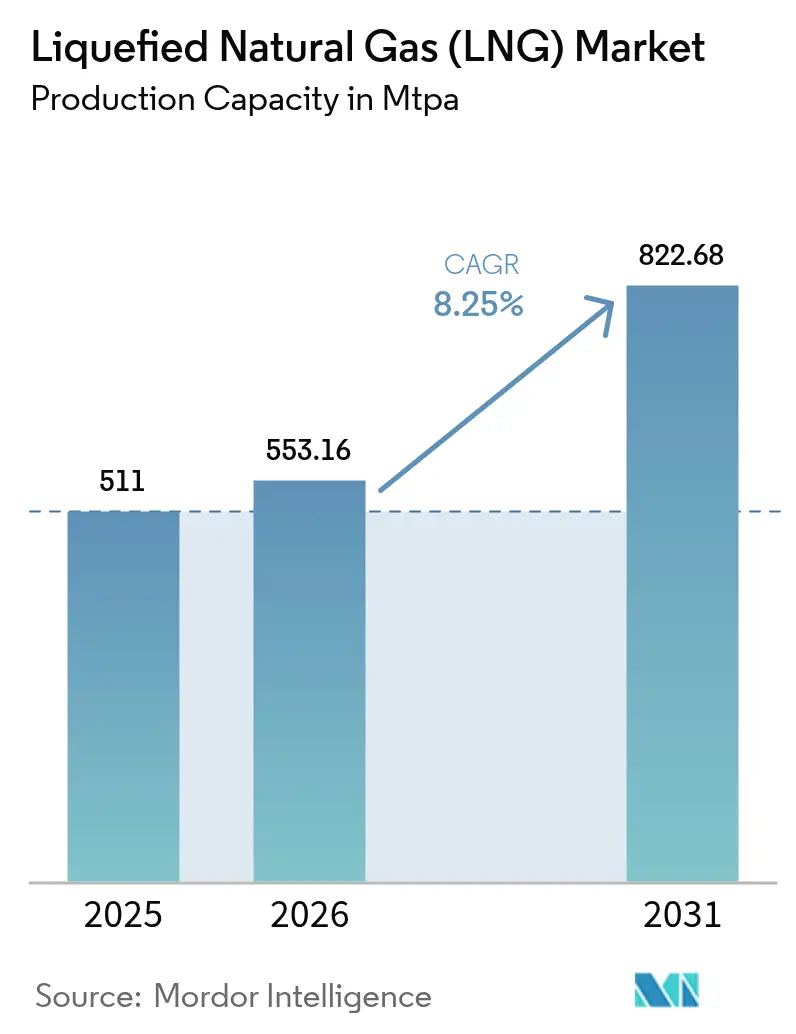

LNG Production Capacity Projected to Reach 822 Mtpa

The section heading discusses Shell confronting a ‘200 MTPA supply wave.’ The chart, which projects a massive increase in global LNG production capacity to 822 Mtpa, directly illustrates the scale and origin of this market-altering supply increase.

(Source: Mordor Intelligence)

Shell Capital Discipline, $5-7 B Cost Cuts and Argentina LNG Project Exit (2025)

Shell executed a highly disciplined capital allocation strategy in 2025, funneling resources into its most profitable integrated gas projects while ruthlessly cutting costs and exiting ventures that failed to meet its high-return criteria. This financial repositioning is designed to fund its ambitious LNG expansion and maximize shareholder returns in an increasingly volatile market.

- At its Capital Markets Day in March 2025, Shell accelerated its financial discipline by increasing its structural cost reduction target from a previous goal of $2-3 billion to a cumulative $5-7 billion by the end of 2028, freeing up capital for its core LNG business.

- The company demonstrated its commitment to growth in core regions by announcing the Final Investment Decision (FID) for the HI Gas Project in Nigeria in November 2025. This project is a key part of its plan to deliver new upstream and integrated gas volumes between 2025 and 2030.

- In a clear signal of its selective investment approach, Shell withdrew from its partnership with state-controlled YPF on the Argentina LNG export project in December 2025. The decision reflects a strategic pivot away from nascent, higher-risk ventures toward more established, cost-advantaged assets.

- While Shell doubled down on gas, other energy firms continued to diversify. For example, Total Energies has been active in the U.S. offshore wind market, illustrating a contrasting approach to the energy transition.

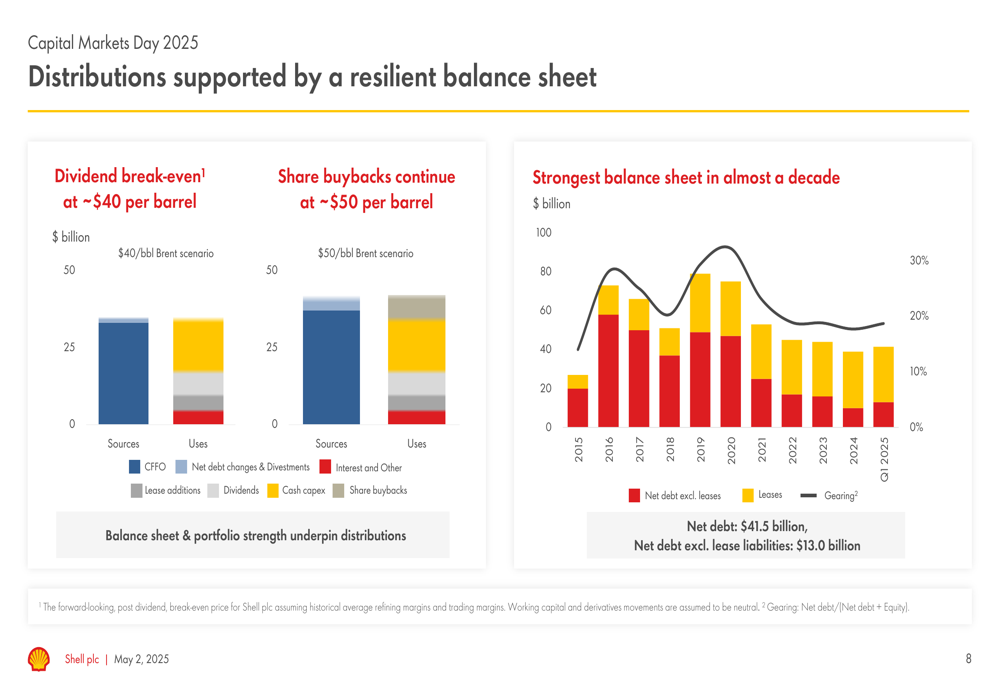

Shell Touts Strong Balance Sheet in 2025

The section focuses on Shell’s ‘Capital Discipline’ and cost-cutting. A chart highlighting Shell’s ‘Strong Balance Sheet’ serves as a direct indicator of the successful implementation and outcome of this financial strategy.

(Source: Investing.com)

Table: Shell Strategic Investments and Divestments in 2025

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| YPF / Argentina LNG | Dec 2025 | Shell withdrew from the initial phase of the LNG export project. This move signals capital discipline and a strategic decision to avoid higher-risk, early-stage developments in favor of more certain projects. | Mexico Business News |

| HI Gas Project | Nov 2025 | Shell announced the Final Investment Decision (FID) for the project in Nigeria. This reinforces its commitment to its integrated gas business in a core operational region and contributes to its future supply pipeline. | Decade of Gas |

| LNG Canada | Jun 2025 | The joint venture, in which Shell holds a 40% stake, shipped its first cargo. This marks the successful operational start-up of a major, long-life asset that adds 14 MTPA of capacity in its first phase. | LNG Canada |

| Structural Cost Reduction Program | Mar 2025 | Shell increased its cost-saving target to $5-7 billion by 2028. This program is designed to improve financial performance and fund capital-intensive growth projects in LNG and other core areas. | Shell |

2 Major Agreements, Shell’s ADNOC Offtake and LNG Canada JV Operations

Shell’s commercial activities in 2025 were centered on bringing massive joint ventures online and securing new long-term supply agreements to fortify its market-leading portfolio. These moves are critical to feeding its global trading operations and ensuring it has a diversified and cost-competitive supply base to navigate the expected market turbulence ahead.

- The most significant commercial milestone was the operational start of the LNG Canada project, where Shell is the largest partner with a 40% stake. The first cargo departure in June 2025 transitions the multi-billion-dollar investment into a revenue-generating asset, with each partner individually marketing its share of the 14 MTPA Phase 1 output.

- In November 2025, Shell strengthened its supply position in the Middle East by signing its first long-term sales and purchase agreement with Abu Dhabi’s ADNOC for offtake from the Ruwais LNG project. This diversifies its portfolio with supply from a key low-cost producing region.

- The complexities of large-scale offtake agreements were highlighted by an ongoing commercial dispute with Venture Global LNG. An arbitral tribunal found in favor of Venture Global in August 2025, underscoring the contractual risks inherent in the commissioning phase of new LNG facilities.

Global LNG Market Valued at $105.3B with 10% Growth

This section highlights two major commercial agreements. The chart provides the essential business context by quantifying the high value and significant growth of the global LNG market, which motivates the signing of such large-scale deals.

(Source: Market.us)

Table: Shell Key LNG Partnerships and Commercial Agreements in 2025

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| ADNOC / Ruwais LNG | Nov 2025 | Signed a long-term LNG sales and purchase agreement, Shell’s first with ADNOC. The deal secures future volumes from the UAE, enhancing supply diversity and strengthening ties with a major national oil company. | Rigzone |

| Venture Global LNG | Aug 2025 | An arbitral tribunal ruled in favor of Venture Global in a dispute over commissioning cargoes from its Calcasieu Pass facility. The dispute highlights significant commercial and contractual risks in the LNG value chain. | Bracewell LLP |

| PETRONAS, Petro China, Mitsubishi Corp., KOGAS / LNG Canada | Jun 2025 | The joint venture successfully dispatched its first LNG cargo. As a 40% owner, this marks a major operational success for Shell, adding significant new supply to its global portfolio. | Europétrole |

| Blackstone | Mar 2025 | Shell confirmed it will supply energy and secure long-term offtake from a power plant acquired by Blackstone, reinforcing its role as a key energy supplier to the private equity sector. | Martindale Consultants |

Canada and UAE vs. Argentina, Shell’s Geographic LNG Focus Shifts in 2025

In 2025, Shell’s geographic strategy for LNG supply became clearer, prioritizing large-scale projects in stable, developed jurisdictions like Canada while increasing its offtake footprint in the low-cost Middle East and selectively divesting from nascent opportunities in regions like Argentina.

- Canada emerged as a pivotal new supply hub for Shell with the first cargo shipped from LNG Canada in British Columbia in June 2025. This asset provides a new, direct, and shorter route to key Asian markets, diversifying supply away from the US Gulf Coast and other traditional sources.

- The Middle East was reaffirmed as a strategic pillar. Shell listed Qatar as a key area for its planned 12 MTPA capacity expansion and signed a new long-term offtake agreement with ADNOC in the UAE, locking in volumes from the world’s lowest-cost producing region.

- Africa remains a core focus, demonstrated by the Final Investment Decision for the HI Gas Project in Nigeria in November 2025. This shows a continued commitment to developing resources in a legacy region with established infrastructure and expertise.

- Conversely, South America saw a strategic retreat, with Shell’s withdrawal from the YPF-led Argentina LNG project in December 2025. This decision highlights a deliberate avoidance of greenfield projects in markets with higher perceived economic and political risk.

LNG Strategy Maturity, Shell Doubles Down on Integrated Gas Model in 2025

Shell’s actions in 2025 confirm the full maturity of its integrated gas strategy, which leverages its unmatched global trading scale and a portfolio of long-life, cost-advantaged assets to navigate market cycles. The company is no longer just a producer; it is a system-level market optimizer positioned to manage and profit from volatility.

- While the 2021-2024 period saw the strategy validated by high prices and energy security concerns, 2025 marked a shift toward preparing for a supply-rich environment. This was evident in the accelerated cost-cutting program and the selective culling of non-core projects.

- The decision in March 2025 to scale back on renewables and double down on gas and LNG marks a definitive strategic verdict. It signals a belief that Shell’s deepest competitive advantage lies in the complex, capital-intensive gas value chain, a market where its scale provides a formidable barrier to entry.

- Shell’s trading and optimization division, the world’s largest, is the central pillar of this mature strategy. It is designed to capture arbitrage opportunities between European and Asian markets and manage portfolio risk, turning the expected price volatility of 2026-2030 from a threat into an opportunity.

- The emphasis on gas for industrial and power applications is also a strategic choice, targeting sectors where electrification is difficult. This focus is different from companies like Bloom Energy, which are targeting specific high-growth niches like data centers with alternative technologies like fuel cells.

Shell LNG SWOT Analysis, 12 MTPA Growth Plan and Market Risks (2021-2025)

In 2025, Shell amplified its historic strengths in the integrated LNG market through disciplined project execution and strategic offtake agreements. However, this intensified focus also magnifies its exposure to emerging market, regulatory, and investor-related threats that became more pronounced during the year.

- Strengths: Shell’s leadership in LNG trading and its diversified, low-cost production portfolio were key assets.

- Weaknesses: The strategy’s high capital intensity and direct exposure to commodity price cycles remain inherent weaknesses.

- Opportunities: The primary opportunity is capturing long-term Asian demand growth and leveraging its trading arm to consolidate market share during the anticipated period of oversupply.

- Threats: A looming supply glut, increasingly stringent methane regulations in key markets like the EU, and persistent shareholder activism on climate change pose the most significant threats to the strategy’s long-term value.

Emerging LNG Technologies and Customer Segments Identified

This section is a SWOT analysis. The chart, which identifies ‘Emerging LNG Technologies and Customer Segments,’ provides direct input for the ‘Opportunities’ and ‘Threats’ components of such a strategic analysis.

(Source: MarketsandMarkets)

Table: SWOT Analysis for Shell’s LNG Strategy

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Benefitted from high prices and European demand for energy security. Trading arm capitalized on extreme market volatility. | Brought LNG Canada online, adding new low-cost supply. Positioned trading arm to manage expected oversupply and capture arbitrage. | The strategy’s strength was validated, shifting from profiting on scarcity to preparing to optimize during a period of abundance. |

| Weaknesses | High capital expenditure on long-cycle projects under construction (e.g., LNG Canada). Growing investor questions on fossil fuel alignment. | Investor pressure intensified, with a climate resolution gaining 20.56% support. The pivot from renewables made this divergence more explicit. | The perceived weakness of being a fossil fuel major became more acute as the company’s strategy formally de-emphasized renewables. |

| Opportunities | Secured market share in Europe as Russian pipeline gas was replaced. | Solidified long-term strategy around forecasted 60% Asian demand growth by 2040. Signed new offtake with ADNOC to diversify supply. | The primary long-term opportunity officially shifted from European energy security to structural demand growth in Asia. |

| Threats | Project execution risk, cost inflation, and supply chain delays were the primary threats. | The main threats evolved to market-level risks: a looming supply glut of 170+ MTPA by 2030 and the compliance costs of the EU Methane Regulation. | Threats transitioned from internal project management challenges to external, systemic market and regulatory risks. |

2026 Outlook, Shell’s Trading Arm to Test the 170 MTPA LNG Supply Wave

Looking to 2026, the central test for Shell’s LNG strategy will be its ability to deploy its powerful trading division to navigate the initial impacts of the global supply wave, defend its margins, and validate its thesis that it can thrive in a more competitive, lower-priced environment.

- If the first wave of new LNG capacity from the US and Qatar arrives on schedule or ahead of it, watch for Shell’s trading arm to actively increase its arbitrage trading between the Atlantic and Pacific basins. This could involve using its vast fleet and regasification capacity to optimize cargo flows and capture value from regional price spreads.

- If Asian demand growth, particularly in China and South Asia, shows signs of slowing due to economic headwinds or faster-than-expected renewables adoption, watch for an increase in cargoes being directed to Europe. This would be a leading indicator that the market is struggling to absorb new supply, potentially leading to a more prolonged period of price weakness.

- If the final implementation details of the EU Methane Regulation prove to be stringent with limited “flexibilities, ” watch for potential shifts in the cost-competitiveness of US LNG into Europe. This could see Shell prioritizing supply from its other low-methane intensity assets, like those in Qatar, to serve the European market.

Global LNG Market Forecasts Strong Decade Growth

The section discusses the ‘2026 Outlook’ and a coming supply wave. A chart forecasting ‘Strong Decade Growth’ provides the perfect long-term contextual backdrop for an outlook-focused section, framing the conditions Shell’s trading arm will face.

(Source: Market.us)

The questions your competitors are already asking

This report covers one angle of Shell’s LNG expansion amidst significant market and regulatory headwinds. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the global LNG market as the 200 MTPA supply wave approaches?

- Is Shell a good investment as it expands its LNG capacity into a forecast market glut?

- What is the outlook for LNG pricing from 2026 to 2030?

- What are the compliance strategies for LNG suppliers to meet the EU’s 2027 Methane Regulation?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.