Onshore Wind PPAs for Data Centers, 833% PJM Price Spike, 7.9 GW Illinois Procurement, and 11 State Bills (2021 to 2026)

Grid Balkanization Risks, Hyperscaler Self-Procurement Bypasses 10 GW Utility Plans

The rapid expansion of data centers, driven by artificial intelligence, is forcing a structural break in the U.S. power sector. The established model of centralized utility resource planning is being bypassed by hyperscalers using self-directed procurement programs to secure power directly from renewable generators. This shift, codified in frameworks like Illinois’s Climate and Equitable Jobs Act (CEJA) and the proposed POWER Act (HB 5513), creates a parallel energy system that offers hyperscalers cost and speed advantages but externalizes significant stability and cost risks onto the public grid and its captive ratepayers.

- Between 2021 and 2024, the primary mechanism for this was the virtual power purchase agreement (VPPA), a financial tool that allowed corporations to meet annual ESG targets by purchasing RECs from new renewable projects. This was viewed as a positive development, aligning corporate capital with decarbonization goals under existing state laws like CEJA, which facilitated over 7.9 GW of renewable energy procurement.

- The dynamic fundamentally shifted from 2025 to today as the sheer scale of AI-driven power demand became apparent. Proposed legislation like Illinois’s HB 5513 signaled a move to formalize and expand this bypass model, just as grid operators began sounding alarms. PJM Interconnection, which serves Illinois, saw its capacity market clearing prices for 2025/2026 surge an unprecedented 833%, explicitly citing data center load growth as a primary driver.

- This creates a balkanized grid where utilities like Com Ed continue with integrated resource plans, including a pipeline of over 10 GW in state-supported renewables, while hyperscalers simultaneously contract for gigawatts of new generation outside this public planning process. This uncoordinated development introduces significant forecasting and reliability challenges for grid operators.

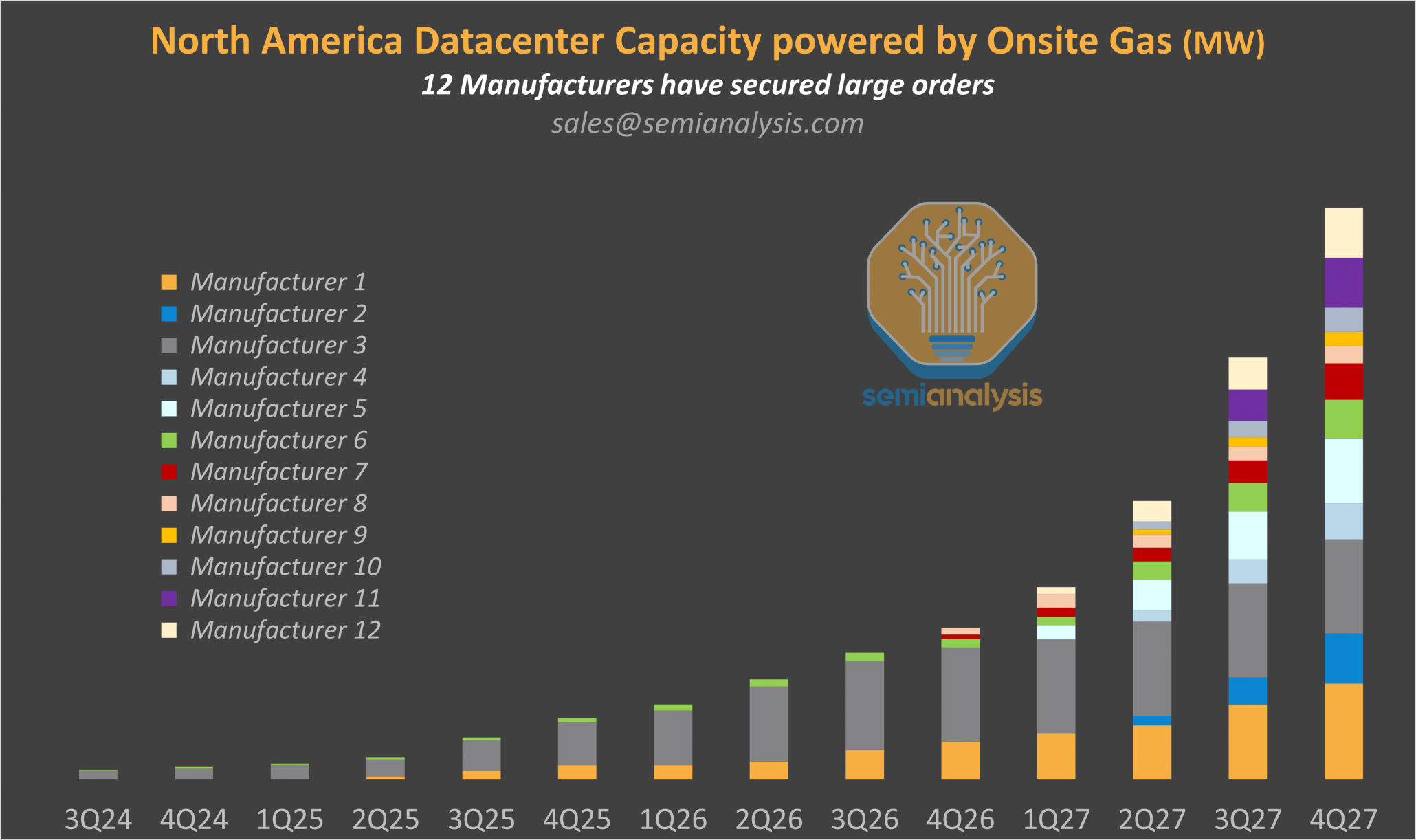

Onsite Gas Power for Datacenters to Surge

The section discusses the large-scale trend of hyperscalers bypassing utilities via self-procurement. The chart, which forecasts a surge in onsite gas power for data centers, directly illustrates a primary method for this self-procurement, highlighting the technology trend that creates the ‘grid balkanization’ risk.

(Source: SemiAnalysis)

$270/MW-day Capacity Price Shock, Com Ed Faces Hyperscaler Cost-Shifting Risks

The economic incentive for hyperscalers to bypass traditional utility procurement is no longer just about long-term price stability; it is now an urgent response to extreme volatility and cost spikes in wholesale capacity markets. This surge directly threatens data center operating models, while the “utility bypass” it encourages transfers the financial burden of necessary grid upgrades onto residential and commercial customers who lack the scale or regulatory freedom to opt out.

- The most acute signal is the PJM Base Residual Auction, where capacity prices for the Com Ed zone are projected to jump from $29/MW-day in 2024/2025 to $270/MW-day in 2025/2026. This represents a direct and material increase in operating costs for any large consumer buying power through standard utility or market-based channels.

- Self-procurement offers a clear financial off-ramp. Wholesale PPA rates for utility-scale solar in 2026 range from $25–$55 per MWh. This is substantially lower than estimated commercial and industrial (C&I) utility rates in Illinois, which can range from $80 to $100/MWh and will eventually incorporate the higher capacity and transmission costs.

- This creates a critical cost-shifting risk. As hyperscalers exit the shared resource pool, they no longer contribute proportionally to the fixed costs of the transmission and distribution grid they still depend on. These costs are then socialized across the remaining ratepayers, leading to higher electricity bills for households and small businesses near data center clusters.

Bloom Energy Highlights Data Center Power Dominance

The section describes the financial risk to utilities like Com Ed when large customers leave the system. The chart highlights a key enabler of this departure: onsite power solutions from companies like Bloom Energy. The adoption of such technologies by hyperscalers is a direct cause of the cost-shifting risk and potential market price shocks discussed.

(Source: Arya’s Substack)

Table: Power Procurement Cost Comparison: PPA vs. Regulated Utility Tariff

| Procurement Model | Metric | Time Period | Estimated Value ($/MWh) | Source |

|---|---|---|---|---|

| Utility-Scale Solar PPA | Wholesale Rate | 2026 | $25 – $55 | Solar Info Path |

| Standard Utility Tariff (Illinois) | Estimated C&I Retail Rate | 2024 | $80 – $100 | Analyst Estimate |

| Existing Gas Plant Generation | Short-Run Marginal Cost | 2025 | $75 | Bloomberg NEF |

| Existing Coal Plant Generation | Short-Run Marginal Cost | 2025 | $48 | Bloomberg NEF |

Google and Intersect Power Partner on Co-Location to Bypass Grid Constraints (2024)

In response to growing grid congestion and multi-year interconnection queues, the most advanced hyperscalers and energy developers are evolving beyond disconnected financial PPAs. They are now forming strategic partnerships to physically co-locate new data centers with new renewable generation, creating a more integrated and resilient model that internalizes grid risk and accelerates deployment.

- The definitive example is the December 2024 partnership formed by Intersect Power, Google, and TPG Rise Climate. This collaboration aims to develop new renewable energy projects specifically to power co-located Google data center infrastructure.

- This strategy directly confronts the primary physical barrier to data center growth: transmission. Permitting and constructing new high-voltage transmission lines can take between 5 and 15 years, whereas a data center can be built in 1-2 years. By building generation on-site or nearby, this model minimizes reliance on the strained public grid.

- This signals a maturation of the corporate procurement market. Instead of simply buying RECs from a remote project, this model represents a direct investment in creating a localized, reliable power ecosystem, effectively privatizing a portion of the energy infrastructure development process.

Texas Power Requests Vastly Exceed Grid Capacity

The chart vividly demonstrates a key problem facing data center developers: grid connection queues and capacity shortfalls, as seen in Texas. The section provides a specific, real-world example of a strategy to solve this exact problem, where Google partners with a generator to co-locate and ‘bypass grid constraints’.

(Source: SemiAnalysis)

Table: Data Center-Generator Strategic Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Intersect Power, Google, TPG Rise Climate | December 2024 | A strategic partnership to co-locate new renewable power generation with new Google data center load. The goal is to bypass transmission constraints and accelerate the deployment of both clean energy and computing infrastructure by integrating their development. | Intersect Power |

Illinois vs. Virginia, Com Ed and Dominion Face Divergent Regulatory Paths for AI Load

The national response to the data center energy challenge is fracturing, with states adopting starkly different regulatory postures. While Illinois is attempting a structured, legislative approach to manage hyperscaler growth, other established hubs like Virginia are dealing with the chaotic fallout of a less-managed expansion, offering a real-time case study in the consequences of uncoordinated development and providing critical lessons for other jurisdictions.

- In Illinois, the proposed POWER Act (HB 5513) represents a proactive attempt to create a “bring your own power” framework. It seeks to hold data centers accountable for sourcing new clean energy to match their load, aiming to protect the grid and other ratepayers while still attracting a share of the projected $1.2 trillion in new data center investment.

- Northern Virginia, the world’s largest data center market, offers a cautionary tale. The region, served by Dominion Energy, experienced such rapid and concentrated growth that the utility was forced to announce potential delays in connecting new facilities due to severe transmission constraints. This reactive scenario has led to proposals for massive, costly grid upgrades that will be funded by the entire ratepayer base.

- This policy divergence is spreading. At least 11 other states have introduced bills to regulate, tax, or outright ban data centers, while grid operators in other high-growth regions like ERCOT in Texas are grappling with how to maintain reliability amidst soaring demand from both data centers and industrial electrification. Utilities like PGE are also exploring new tariff structures to manage this new load class.

Procurement Model Maturity, Hyperscalers Shift from VPPAs to 24/7 CFE Portfolios

The initial corporate procurement model, which relied on annual matching of energy consumption with renewable energy certificates (RECs), is now considered insufficient for addressing the hourly realities of grid operations. As a result, the most sophisticated energy buyers are transitioning to 24/7 Carbon-Free Energy (CFE) strategies, a more mature and complex approach that aims to match a facility’s electricity use with clean power generation on an hour-by-hour basis.

- From 2021 to 2024, the Virtual Power Purchase Agreement (VPPA) was the dominant self-procurement tool. This financial contract allowed companies to claim 100% renewable energy on an annual basis. While commercially mature, this model did little to reduce a company’s actual hourly emissions, as the facility would still draw from a fossil-heavy grid when its contracted solar or wind farm was not producing.

- From 2025 onward, pioneers like Google have championed 24/7 CFE. This requires procuring a diverse portfolio of clean energy resources, including solar, wind, geothermal, and energy storage, to ensure that clean power is available to match the data center’s load around the clock. This sends a much stronger market signal for investment in firm, dispatchable clean technologies that are critical for grid reliability.

- This trend is also driving interest in long-term, “always-on” power sources. The pursuit of true 24/7 CFE is a key reason for corporate exploration of advanced nuclear technologies like Small Modular Reactors (SMRs). Although SMRs are still in a pre-commercial phase (TRL 6-8), Microsoft‘s 2023 agreement to explore nuclear energy sourcing demonstrates a strategic move toward securing firm, carbon-free power that can anchor a 24/7 CFE portfolio.

Hyperscaler Self-Procurement SWOT Analysis: A Utility Bypass Model

The self-procurement model represents a rational and effective strategy for individual hyperscalers to manage costs and meet sustainability mandates in a volatile energy market. However, its strengths are inextricably linked to weaknesses and threats that arise from its disruptive impact on the integrated grid system, creating a fragile equilibrium that is vulnerable to policy and infrastructure constraints.

Table: SWOT Analysis for Hyperscaler Self-Procurement Models

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | VPPAs offered long-term cost hedges against market volatility and provided a clear path to 100% annual renewable energy targets for ESG reporting. | Direct cost savings became extreme due to wholesale capacity price spikes (+833% in PJM). Self-procurement is now a critical opex-reduction strategy, not just an ESG initiative. | The financial case for bypassing utility tariffs has been validated and intensified by market conditions, shifting the driver from sustainability to economic necessity. |

| Weaknesses | Dependence on lengthy interconnection queues and limited transmission capacity were recognized as long-term project risks. | These weaknesses became acute bottlenecks. The 5-15 year timeline for transmission build-out is now the primary constraint on data center growth in key markets like Northern Virginia. | The model’s core vulnerability, its reliance on a public grid it does not fully fund, has been exposed as the rate of data center growth outpaces grid expansion. |

| Opportunities | Corporate offtake agreements were seen as a way to provide revenue certainty for new renewable energy projects. | Hyperscaler capital is now seen as essential for developing firm clean power, with buyers like Google pursuing 24/7 CFE portfolios that require storage and geothermal. | The opportunity has matured from simply funding intermittent renewables to catalyzing the development of the next generation of dispatchable clean technologies needed for grid reliability. |

| Threats | The risk of cost-shifting to other ratepayers was a theoretical concern raised by consumer advocates and regulators. | This threat has materialized. Lawmakers in 11 states are considering data center regulations, and Illinois’s governor proposed suspending tax incentives, signaling significant political backlash. | The “social license to operate” is now at risk, as the model’s negative externalities on public infrastructure and non-participating customers become politically untenable. |

2026 Scenario Modeling: Will Grid Access Fees Derail Hyperscaler Bypass Strategies?

The strategic calculus for hyperscaler energy procurement in 2026 hinges on the regulatory response to the cost-shifting dilemma. The most critical factor to watch is the potential implementation of non-bypassable “grid access fees” or similar charges designed to force data centers to internalize the full cost of their grid impact. The outcome of this policy battle will determine whether the self-procurement model continues its exponential growth or faces a significant economic correction.

- If states successfully implement Grid Access Fees, watch for an immediate re-evaluation of data center siting strategies. Hyperscalers may slow development in those jurisdictions or pivot aggressively toward fully integrated, co-located projects like the Google/Intersect Power model, which reduce reliance on the public transmission network. This could also increase interest in powering data centers with on-site resources like the natural gas assets being acquired by firms like Blackstone.

- If these policies fail or are delayed, expect an acceleration of utility bypass, further exacerbating grid fragmentation. This will likely trigger more extreme political responses from consumer advocates and lawmakers, potentially leading to outright development moratoria, as has been debated in several localities, including in Loudoun County, Virginia.

- These could be happening already, as evidenced by the Illinois governor’s proposal to suspend data center tax incentives in February 2026. This move, while not a direct grid fee, is a clear political signal that the era of unconditional public support for data center growth is ending and that the industry’s external costs are becoming a central focus of state policy.

Onsite Power Redundancy Costs Rise With Unit Size

The section explores the future financial viability of bypass strategies in the face of potential grid access fees. The chart provides a crucial cost input for this scenario modeling. The rising cost of onsite redundancy must be weighed against proposed grid fees to determine the most economic path forward.

(Source: SemiAnalysis)

The questions your competitors are already asking

This report covers one angle of how legislative frameworks like Illinois’ HB 5513 enable hyperscalers to bypass utility procurement, creating a parallel energy system. The questions that matter most depend on your work.

- What is the status of Illinois’ POWER Act (HB 5513), and which other states are considering similar legislation to allow data center self-procurement?

- Which hyperscalers are gaining ground against utilities like ComEd by using self-direct procurement programs in Illinois?

- What is the outlook for PJM capacity market prices, and how much risk is being shifted from hyperscalers to captive ratepayers?

- How does the cost and speed of hyperscaler self-procurement compare to traditional utility Integrated Resource Plans (IRPs) for new renewable energy projects?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.