The 2026 Memory Supercycle: How the HBM Supply Crisis Redefines AI Infrastructure

HBM Adoption Risks: How AI Demand Created the 2026 Supply Bottleneck

HBM Adoption Risks: How AI Demand Created the 2026 Supply Bottleneck

The artificial intelligence sector’s explosive growth has created a structural supply crisis, elevating High-Bandwidth Memory (HBM) from a specialized component to the primary bottleneck for AI hardware deployment through 2026. The market has shifted from a supply-driven environment to one defined by extreme demand, where major memory producers are sold out years in advance, giving them unprecedented pricing power and exposing the fragility of the advanced semiconductor supply chain.

- Between 2021 and 2024, the market was characterized by the adoption of HBM 3, with SK Hynix securing a dominant position as the exclusive supplier for NVIDIA’s H 100 GPU. This period established HBM’s technical necessity for AI, but supply could still largely meet demand.

- The period from 2025 to today marks a fundamental inflection point. Demand for HBM 3 E, required for next-generation accelerators like the NVIDIA B 200, has overwhelmed production capacity. SK Hynix and Micron Technology reported their entire 2026 HBM production is sold out, signaling a prolonged memory crisis.

- This imbalance is driven by the escalating memory requirements of AI models. NVIDIA’s Blackwell B 200 GPU uses 192 GB of HBM 3 E, a 140% increase from the H 100’s 80 GB. This rapid growth in memory per chip, multiplied by millions of units, has created a demand tsunami that manufacturing cannot meet.

- The crisis is compounded by execution failures. Samsung Electronics has struggled to meet NVIDIA’s qualification standards for its 12-layer HBM 3 E chips due to yield and performance issues, relegating the world’s largest memory maker to a tertiary position and tightening the bottleneck further.

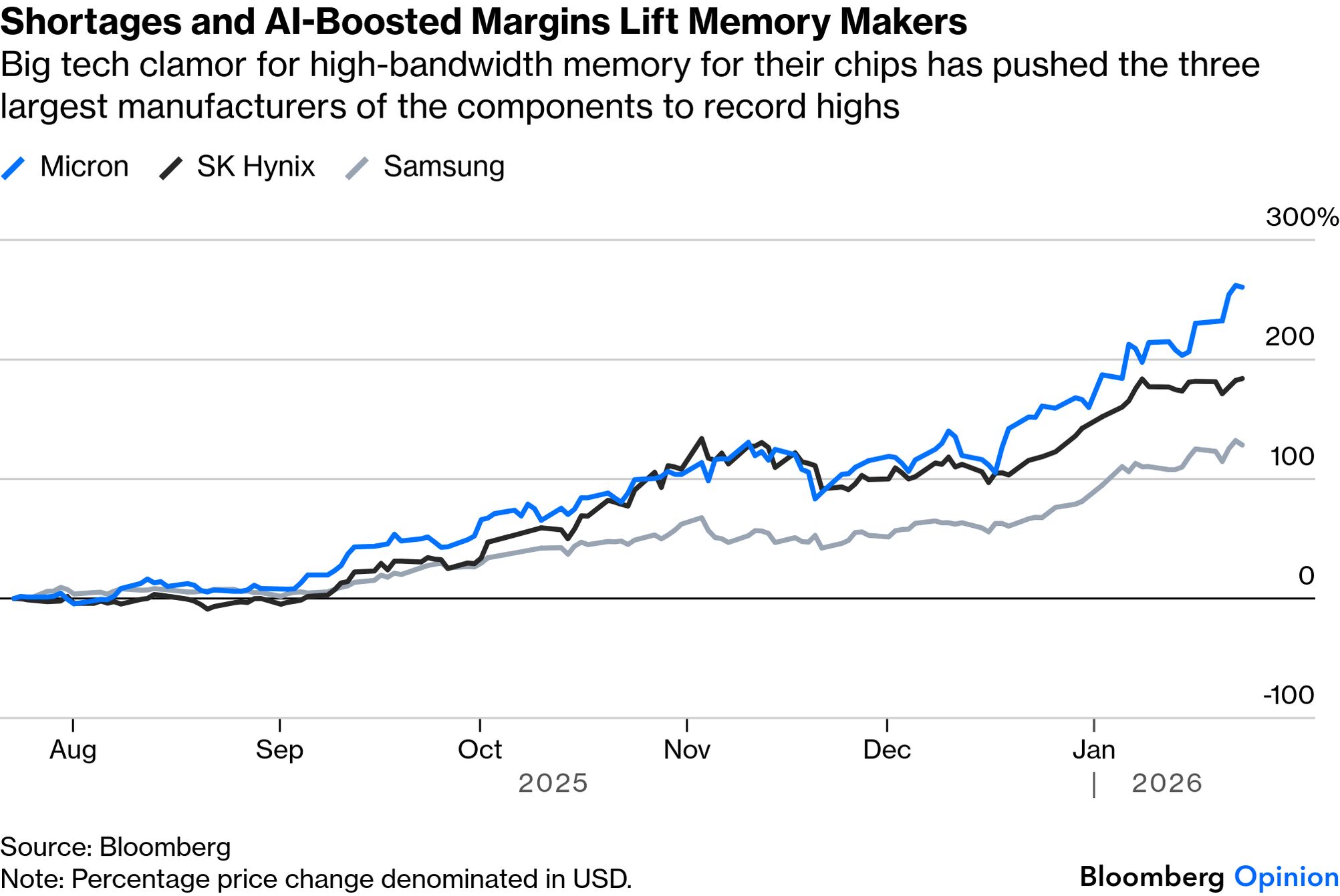

HBM Prices Soar Amid AI-Fueled Shortages

This chart directly illustrates the ‘unprecedented pricing power’ and supply crisis mentioned in the section, showing how extreme AI demand has caused HBM prices to skyrocket into 2026.

(Source: EnkiAI)

The Investment Race: A Multi-Billion Dollar Push to Break the 2026 HBM Choke Point

In response to the structural supply shortage, leading HBM producers have initiated massive capital expenditure programs aimed at expanding fabrication and advanced packaging capacity. These multi-billion-dollar investments underscore the industry’s recognition that the current supply-demand imbalance is not a cyclical trend but a long-term reality, although the long lead times mean new capacity will offer no significant relief before 2026–2027.

- SK Hynix is aggressively investing to defend its market leadership, committing over $30 billion to new capacity. This includes a landmark $15 billion advanced packaging plant in the United States and $14.6 billion for its M 15 X fab in South Korea, both focused on HBM 3 E and future HBM 4 production.

- Micron Technology has raised its 2026 capital expenditure to $20 billion, with a strategic focus on its mega-fabs in Idaho. The company is also investing $7 billion in a new HBM assembly facility in Singapore, demonstrating a global strategy to increase its HBM market share.

- These investments highlight a critical dynamic: HBM production is far more resource-intensive than traditional DRAM. The diversion of wafer capacity to produce lucrative HBM chips is creating an artificial shortage in the commodity memory market, threatening to drive up prices for consumer electronics and automotive components. This entire dynamic is a key part of the broader AI manufacturing constraint in 2026.

Table: Major HBM Capacity and R&D Investments (2025-2026)

| Company | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| SK Hynix | Feb 2026 | Announced a $15 billion investment for an advanced HBM packaging plant in the U.S. to secure its supply chain for key American clients like NVIDIA. | Financial Content |

| Micron Technology | Feb 2026 | Increased its 2026 capital expenditure to $20 billion, targeting capacity expansion at its Idaho mega-fabs for both HBM and traditional DRAM. | Financial Content |

| SK Hynix | Jan 2026 | Announced plans for a $10 billion AI investment arm in the U.S. to fund semiconductor, data center, and related AI infrastructure projects. | KED Global |

| SK Hynix | Dec 2025 | Committed 20 trillion KRW (~$14.6 B USD) for its M 15 X fab in South Korea, which will serve as a primary production hub for HBM 3 E and next-generation HBM 4. | Business Korea |

| Micron Technology | Jun 2025 | Announced a $7 billion investment in a new HBM assembly and test facility in Singapore, with operations scheduled to begin by 2027. | The Globe and Mail |

Partnership Analysis: Strategic Alliances Defining the HBM Market in 2026

In the high-stakes HBM market, strategic partnerships between memory suppliers, foundries, and AI accelerator designers are critical for success. These alliances dictate market share, accelerate technological development, and determine which companies can navigate the severe supply constraints. Early and deep collaboration has become the primary determinant of leadership, separating the winners from the laggards.

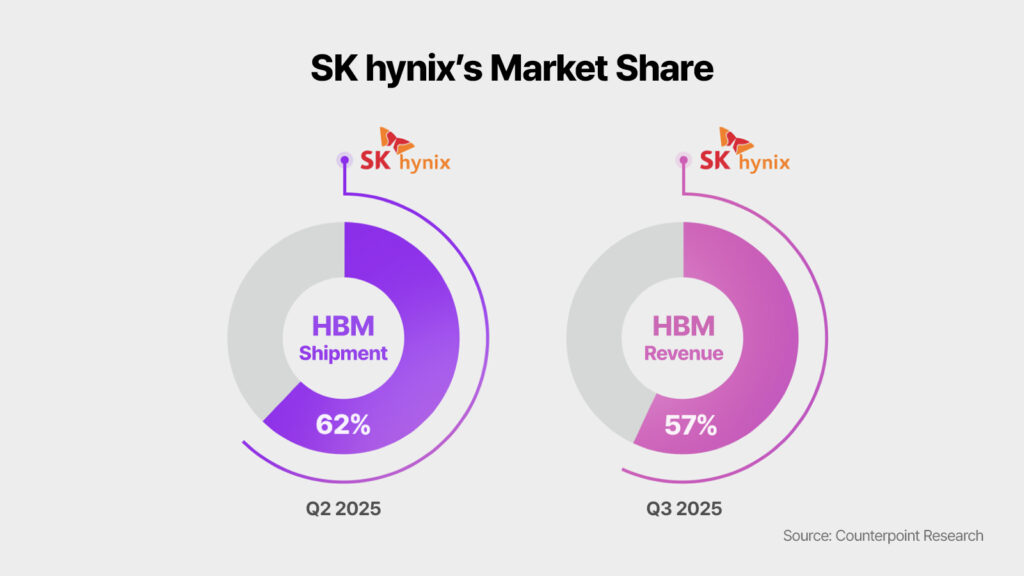

SK Hynix Projected to Dominate 2025 HBM Market

This section states that strategic alliances dictate market share, and this chart quantifies that outcome, showing the market dominance of SK Hynix resulting from its key partnerships.

(Source: SK hynix Newsroom)

- The foundational partnership in the market remains the one between SK Hynix and NVIDIA. SK Hynix’s status as the primary HBM 3 supplier for the H 100 cemented its market dominance, a relationship that continues with HBM 3 E for the B 200 and H 200 platforms.

- Micron Technology’s strategic success is a direct result of its focused partnership with NVIDIA for the H 200 GPU. By skipping the HBM 3 generation and concentrating on a power-efficient HBM 3 E solution, Micron secured a critical design win that established it as a credible second source and captured significant market share.

- Looking ahead to the next generation, SK Hynix has formed a crucial alliance with foundry-leader TSMC to co-develop HBM 4. This partnership aims to tackle the complex integration challenges of HBM 4, including hybrid bonding, giving SK Hynix a head start on the technology that will define the market post-2026.

Table: Key HBM Strategic Partnerships

| Partners | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| SK Hynix & TSMC | Apr 2024 | Announced a partnership to co-develop HBM 4 memory, focusing on performance and integration with TSMC’s advanced logic processes. This positions both to lead the next technological transition. | SK hynix Newsroom |

| Micron Technology & NVIDIA | Feb 2024 | Micron commenced volume production of its HBM 3 E memory, which was selected for NVIDIA’s H 200 Tensor Core GPU, marking Micron’s successful entry into the high-end AI memory market. | Micron Investor Relations |

| SK Hynix & NVIDIA | Mar 2024 | SK Hynix began mass production of its HBM 3 E product, becoming the first supplier to deliver the memory for NVIDIA’s latest GPUs, including the B 200, extending its long-standing partnership. | KED Global |

Geographic Focus: How the HBM Bottleneck is Reshaping Global Semiconductor Strategy

The intense competition and strategic importance of HBM are driving a geographic realignment of the semiconductor supply chain, with activity concentrated in a few key nations. While South Korea remains the epicenter of HBM manufacturing, significant new investments in the United States reflect a strategic push to onshore critical advanced packaging capabilities, driven by government incentives and a desire to de-risk supply chains.

- From 2021 to 2024, HBM production and development were overwhelmingly concentrated in South Korea, home to market leaders SK Hynix and Samsung. This region continues to house the largest HBM fabrication facilities.

- Starting in 2025, a notable shift began with major investment announcements in the United States. SK Hynix’s $15 billion advanced packaging plant in Indiana and Micron’s $20 billion focus on its Idaho fabs represent a direct response to geopolitical risks and incentives from the U.S. CHIPS Act.

- Asia remains central to the broader supply chain. Micron’s $7 billion HBM assembly facility in Singapore highlights the region’s continuing importance in backend manufacturing, while Taiwan’s TSMC remains the indispensable partner for advanced packaging (Co Wo S) and future HBM 4 integration.

Technology Maturity: HBM 3 E at Scale but Facing 2026 Production Limits

HBM 3 E has reached commercial scale and is the established memory standard for leading-edge AI accelerators, but its manufacturing complexity and long production cycles are the core of the 2026 supply bottleneck. The technology has matured from early sampling to mass production, yet suppliers cannot ramp capacity fast enough to meet demand, while the industry is already planning for the even more complex transition to HBM 4.

- In the 2021-2024 period, the industry’s focus was on scaling HBM 3. SK Hynix achieved high-volume manufacturing for NVIDIA’s H 100, while competitors were still in the development phase.

- From 2025 to today, the focus has shifted to HBM 3 E, with both SK Hynix and Micron achieving mass production. The key technical differentiator has become manufacturing yield, where SK Hynix has reported rates near 80%, a significant advantage over Samsung, which has struggled with its 12-layer stack qualification. The power consumption of these new chips is also a major factor, with data centers increasingly focused on liquid cooling and mitigating the AI power crisis.

- The technological frontier is advancing rapidly. Suppliers are moving from 8-layer HBM 3 E stacks to 12-layer and even 16-layer versions, pushing capacities to 36 GB and 48 GB per stack. This progression, while necessary for future AI models, further complicates manufacturing and exacerbates the supply-demand imbalance.

SWOT Analysis: Navigating the High-Stakes HBM Market in 2026

The HBM market is defined by a unique combination of explosive demand and severe manufacturing constraints, creating a high-risk, high-reward environment for its key players. This SWOT analysis breaks down the core strategic factors shaping the industry as it contends with the supply bottleneck leading into 2026.

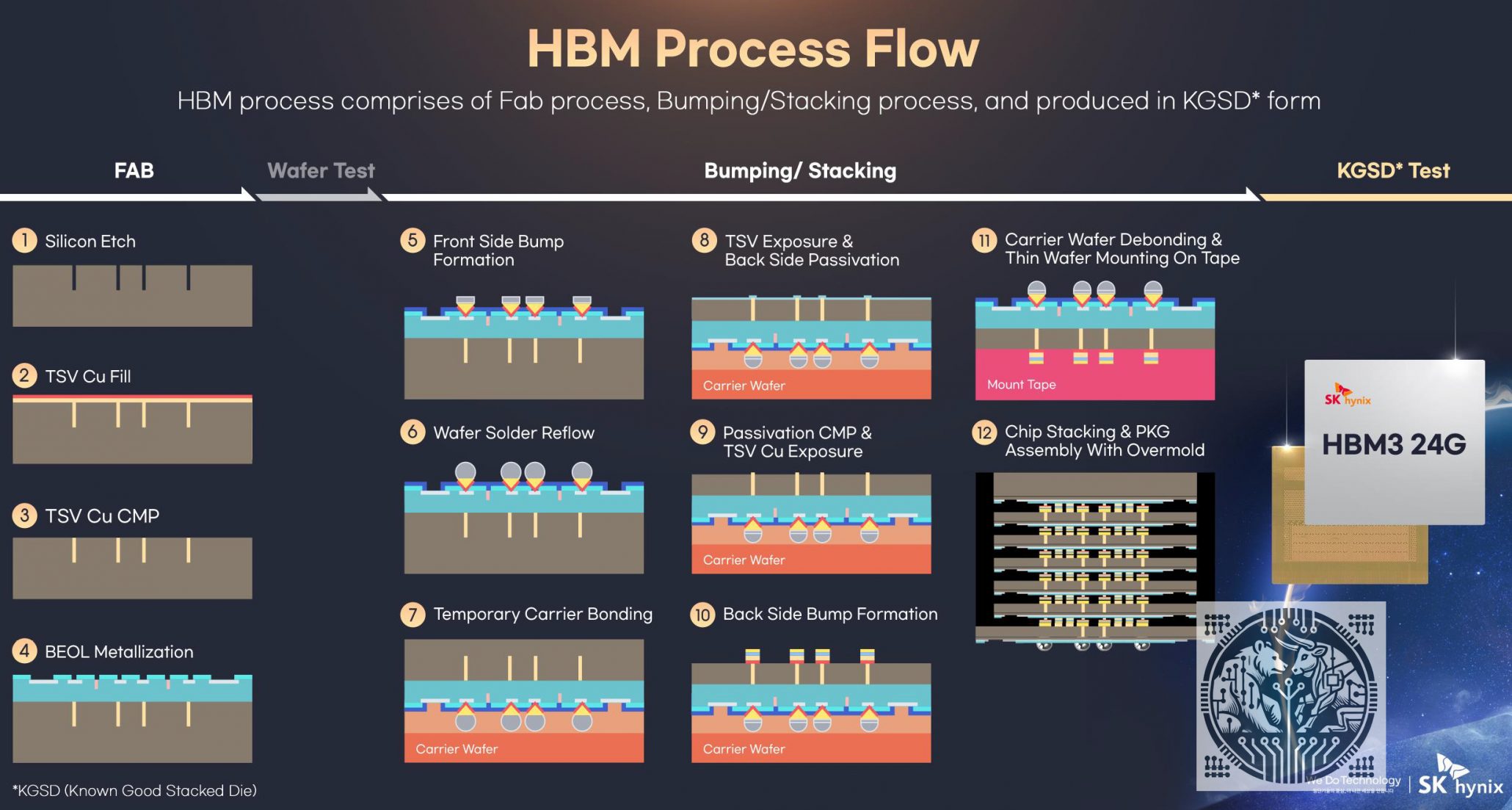

Visualizing HBM’s Manufacturing Complexity

This section’s SWOT summary identifies ‘profound manufacturing complexity’ as a core weakness, and this infographic directly illustrates that complex, multi-stage process.

(Source: Tech Investments)

- The market’s primary strength lies in the oligopolistic structure and extreme pricing power held by successful suppliers.

- Its core weakness is the profound manufacturing complexity and long lead times for new capacity, which make the supply chain rigid and slow to respond to demand surges.

- The main opportunity is the sustained, multi-year growth of the AI market, which has permanently elevated memory from a commodity to a high-margin strategic component.

- A significant threat remains the rapid pace of technological change, where a failure to execute on the next generation (HBM 4) could quickly erode a company’s market leadership.

Table: SWOT Analysis for the HBM Market (2021-2025)

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | High barrier to entry due to technical complexity. Established partnerships with key GPU makers. | Extreme pricing power with HBM prices rising 5-10%. Oligopoly solidified with sold-out capacity through 2026. High yields (near 80%) for leaders like SK Hynix. | The value of memory was validated as a strategic, high-margin asset, not a commodity. First-mover advantage and manufacturing excellence became the key drivers of profitability. |

| Weaknesses | Long production cycles. High sensitivity to yield rates. Dependency on a single customer (NVIDIA) for a large portion of revenue. | Inability to meet demand despite massive investment. Production is constrained by other bottlenecks like TSMC’s Co Wo S packaging. Laggards like Samsung faced public qualification failures. | The market’s structural inability to scale supply in line with demand was confirmed. The bottleneck shifted from just HBM production to the entire advanced packaging ecosystem. |

| Opportunities | Growing demand from AI and HPC applications. Potential to command price premiums over standard DRAM. | AI market projected to drive HBM revenue to over $30 billion by 2026. Cannibalization of DRAM creates price hikes across all memory segments. Government incentives (U.S. CHIPS Act) fund expansion. | The “AI supercycle” was validated as a long-term structural shift. The economic incentive to prioritize HBM over commodity DRAM became an explicit industry strategy. |

| Threats | Risk of a new entrant or competitor leapfrogging in technology. Cyclical nature of the memory market. | Rapid transition to HBM 4 risks making current HBM 3 E investments obsolete. Geopolitical risks cited by SK Hynix. Dependence on NVIDIA creates concentration risk as it seeks to diversify suppliers. | The threat of technological disruption accelerated, with the HBM 4 transition now a primary focus. Geopolitical and supply chain diversification became urgent strategic priorities for both producers and customers. |

Scenario Model: A Two-Tier Market Emerges from the 2026 Bottleneck

The critical uncertainty shaping the HBM market through 2026 is whether it will remain a functional duopoly or if a viable third competitor can emerge to alleviate the supply crisis. The outcome will directly impact pricing, availability, and the pace of AI hardware innovation for the rest of the technology industry.

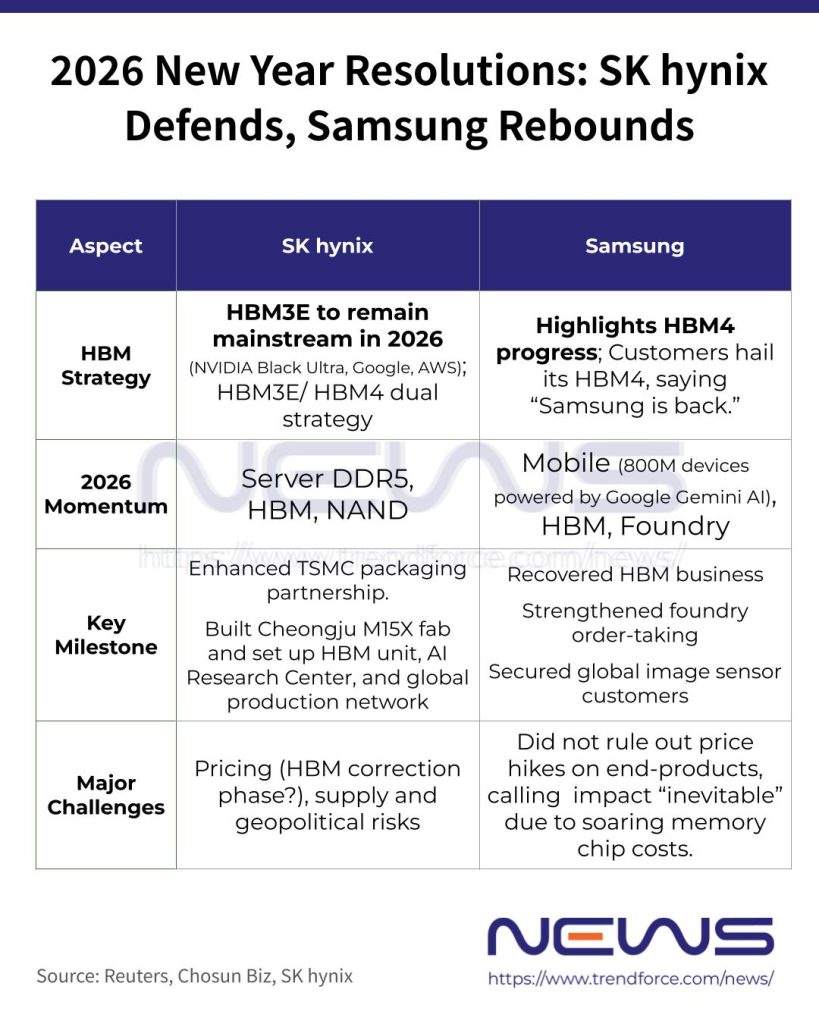

HBM Market Leaders Detail 2026 Strategies

The section proposes a scenario based on the competitive dynamics between HBM leaders, and this chart directly outlines the 2026 strategies of SK hynix and Samsung that will determine the outcome.

(Source: TrendForce)

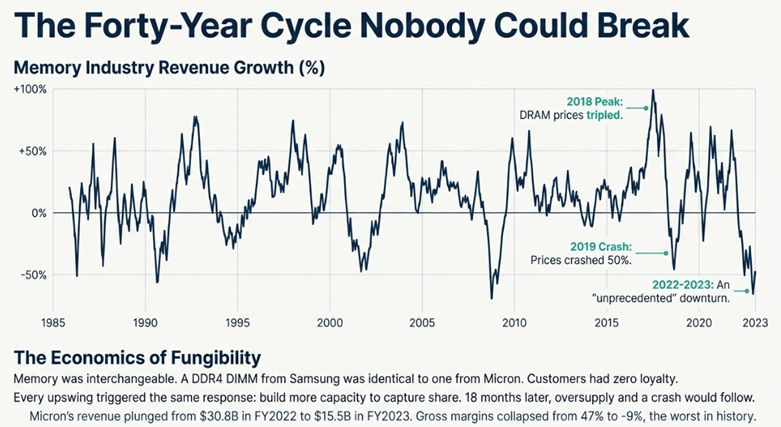

Memory Market’s 40-Year Boom-Bust Cycle

This chart provides critical context for the SWOT analysis, visualizing the historical ‘boom-bust’ commodity cycle that the HBM market is now breaking away from, as noted in the ‘What Changed’ column.

(Source: Nikhs – Substack)

- If Samsung Electronics fails to achieve high-yield, high-volume production of its 12-layer HBM 3 E and future HBM 4 products by mid-2026, then the industry will face a prolonged and more acute supply bottleneck.

- Watch for NVIDIA’s official supplier announcements for its 2026 GPU roadmap and Samsung’s quarterly reports on its foundry and memory division yields. A failure to be named as a primary supplier would confirm its continued struggles.

- In this scenario, SK Hynix and Micron will solidify their control, commanding even higher price premiums. AI companies and hyperscalers will face extended lead times and potentially be forced to delay infrastructure build-outs, impacting the overall growth trajectory of the AI sector and underscoring the severity of the global AI power demands.

Frequently Asked Questions

Why is there a major HBM supply crisis expected to last through 2026?

The crisis is caused by a massive surge in demand from the AI sector. Next-generation AI accelerators, like NVIDIA’s B200 GPU, require significantly more memory (192 GB of HBM3E) than their predecessors. This rapid growth in memory-per-chip, multiplied by millions of units, has created a demand that far exceeds the current global manufacturing capacity, leading to producers being sold out years in advance.

Who are the main companies leading the HBM market?

The HBM market is currently led by SK Hynix, which secured a dominant position through its exclusive supply partnership with NVIDIA for the H100 GPU. Micron Technology has emerged as a strong second supplier after securing a design win with its HBM3E for NVIDIA’s H200 GPU. Samsung Electronics, while a major memory producer, is currently lagging in a tertiary position due to production challenges.

Why is Samsung Electronics struggling to compete with SK Hynix and Micron?

According to the article, Samsung has faced significant challenges in meeting NVIDIA’s qualification standards for its 12-layer HBM3E chips. These struggles are attributed to issues with manufacturing yield and performance, which have prevented Samsung from becoming a primary supplier and have intensified the overall market bottleneck.

What is being done to solve the HBM supply bottleneck?

Major HBM producers are making massive capital investments to expand production. SK Hynix has committed over $30 billion to new advanced packaging and fabrication plants in the U.S. and South Korea. Similarly, Micron is investing $20 billion in its Idaho mega-fabs and $7 billion in a new facility in Singapore. However, due to long lead times, this new capacity is not expected to significantly alleviate the shortage before 2026-2027.

How are strategic partnerships shaping the HBM market for 2026?

Strategic partnerships are critical for success. The SK Hynix and NVIDIA alliance established market leadership and continues with the B200 GPU. Micron’s focused partnership with NVIDIA for the H200 GPU allowed it to capture significant market share. Looking ahead, SK Hynix is partnering with TSMC to co-develop HBM4, aiming to get a head start on the next generation of memory technology that will define the market post-2026.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.